Boost Your Retirement Savings by “Leaps and Bounds”

Let’s be honest…

Who wouldn’t want a lifetime of potential profits?

That’s why David Fessler and I decided to introduce our new Leaps and Bounds Portfolio. We wanted to showcase long-term opportunities – particularly Long-Term Equity Anticipation Securities (LEAPS) – as well as broad sector exchange-traded funds (ETFs) that offer substantial upside with more spread-out risk.

LEAPS are how professional traders love to make money. As a refresher, these are options with more than nine months until expiration.

They behave just like other options. But they have a longer “shelf life.”

Our goal with this special portfolio is to help you reap benefits similar to those you’d see if you owned the stock…

But at the same time, enjoy the potentially life-changing returns of owning options.

I’m talking 100%… 200%… and even 1,000%.

Now, don’t worry. LEAPS are often less risky than traditional options. That’s because they have a long runway and there’s the potential for one major positive catalyst after another. So as shares of the underlying company gain 10%, 20% or more, these LEAPS can skyrocket several times that.

When there’s an attractive opportunity in the market, buying the stock is a no-brainer. But when you want to limit the capital tied up in an investment AND have the opportunity for explosive returns – especially over the next year or so – LEAPS are the way to go.

With that in mind, Dave and I have three opportunities to share with you today. We think these plays can help investors boost their retirement savings by leaps and bounds in the years ahead.

Matthew’s Pick No. 1: Flying High… Once Again

2020 was a devastating year for airlines, cruise ships, restaurants, movie theaters, theme parks and travel stocks.

COVID-19 brought large swaths of the global economy to a grinding halt.

And we saw scores of bankruptcies unfold in these sectors.

A dozen national restaurant chains declared bankruptcy, including California Pizza Kitchen, Chuck E. Cheese, Ruby Tuesday and Sizzler. Admittedly, many of those had been in decline for years. COVID-19 was merely the final nail in the coffin, bringing a quick end to a long, slow death.

It did the same for long-suffering retail chains such as Guitar Center, J.C. Penney, J. Crew, Modell’s Sporting Goods, Neiman Marcus, Pier 1 Imports, True Religion and others.

But that doesn’t include the thousands upon thousands of small businesses that went under due to the pandemic and the quarantine measures.

Airlines have survived. But they were also some of the hardest hit.

With people around the world shuttered away in their homes, viewing the world from afar through screens and mobile devices, major carriers reduced their routes by as much as 90% during the peak of the pandemic.

Australian airline Qantas said COVID-19 cost it billions as its profits collapsed more than 90%. And it didn’t believe international travel would rebound until mid-2021.

Others suffered far worse. Air Italy, Avianca, Compass Airlines, Norwegian Air, Ravn Alaska and dozens more went under.

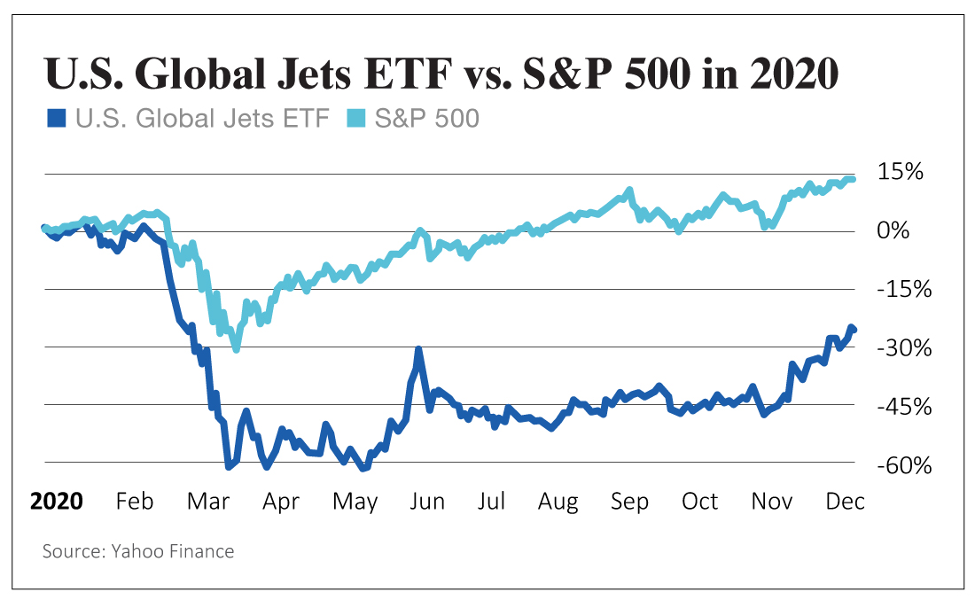

The U.S. Global Jets ETF (NYSE: JETS) tumbled more than 60% and was one of the worst-performing sectors on the S&P 500 in 2020.

The industry is a wasteland of losses that only the bravest of investors are venturing into.

But the famous adage “Be fearful when others are greedy and greedy when others are fearful” doesn’t apply only to the entire market. It also applies to specific sectors.

With the markets at new highs, there are some days it feels near impossible to find opportunities that are trading at a discount to future growth.

But airlines are one of those opportunities. Investors can buy shares for cheap with the prospect of better days ahead.

We have COVID-19 vaccines from AstraZeneca, Moderna, Pfizer and others. And that means the biggest disrupter in the market for 2021 is the return to normalcy.

So, for me, airlines are some of the must-owns for the year ahead. There’s pent-up consumer demand for travel… and anything besides being stuck at home.

And right now, the most attractive of the beaten-down airline sector is American Airlines (Nasdaq: AAL).

American Airlines and its subsidiary American Eagle typically offer 6,700 flights per day to nearly 350 destinations in 50 countries around the world.

Obviously, COVID-19 grounded most of that. And we can see the impact in its financial results.

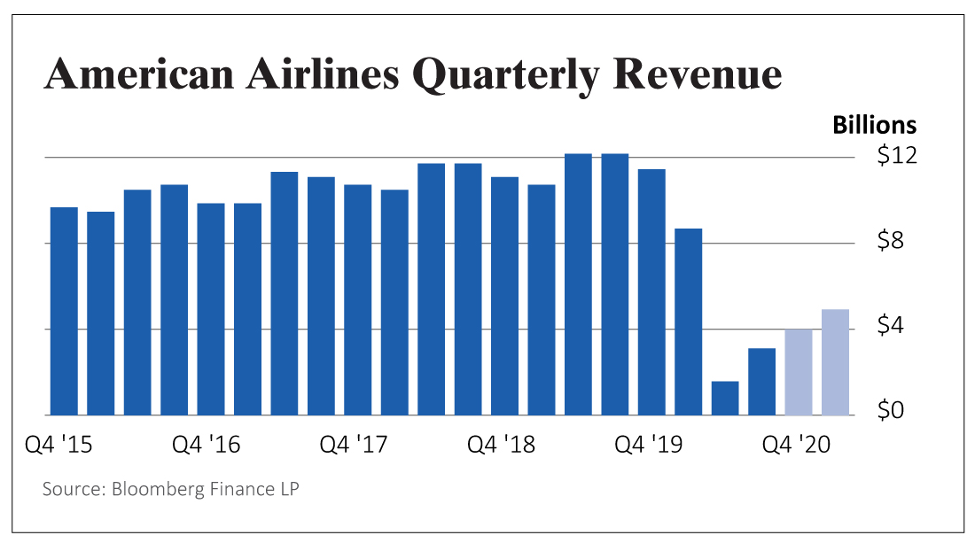

In the second quarter of 2020, American Airlines faced one of the most challenging quarters in its history. Revenue collapsed 86.4% to $1.622 billion as available seat miles plummeted 78.4%.

The airline’s shares were torched in 2020, falling nearly 70% to levels not seen since 2010… in the aftermath of the financial crisis.

But the bottom for its business was hit in April. We’ve since seen – and will continue to see – improvements.

In the third quarter, revenue was down “only” 73% to $3.2 billion. And that was on a year-over-year reduction of 59% in available seat miles.

But it saw improvements in passenger demand in the quarter. And I expect this will accelerate as the vaccines become widely available in the second half of 2021.

When the books are closed on 2020, American Airlines is projected to see that revenue dropped more than 62% to $17.21 billion.

But bluer skies are ahead for 2021. And I love targeting companies that are coming off these types of lows.

For the year ahead, American’s revenue is expected to climb 56.8% to $26.98 billion. Meanwhile, its loss per share will shrink from approximately $20 in 2020 to $5.49.

And that will trigger a rebound in shares.

So I think this is a perfect opportunity for a LEAPS play.

Shares of American are nearly 50% below their 52-week high of $30.78. That was set in February 2020, before the pandemic unfolded. They also trade at a price-to-sales ratio of 0.29, well below its peer average of 0.94. That means they’re trading at an even steeper discount than competitors like Alaska Air, Delta and United.

Action to Take: Buy the American Airlines (Nasdaq: AAL) January 20, 2023, $15 calls. Be patient. Go as low as possible. This LEAPS play offers better upside than owning shares.

Matthew’s Pick No. 2: A Bet on a Return to Normalcy

If you’ve been a subscriber to Strategic Trends Investor for some time, you know I’m not one of those die-hard, permanent commodity bulls.

I think crude oil will slowly lose its place to renewables and alternative fuel sources. I’m not one of those analysts who believe crude is a permanent staple.

And remember, oil and natural gas, as well as other commodities like uranium and gold, are where I got my start.

I consider myself a selective energy bull.

And when I’ve made my calls on crude in the past – both bearish and bullish – they’ve largely been right.

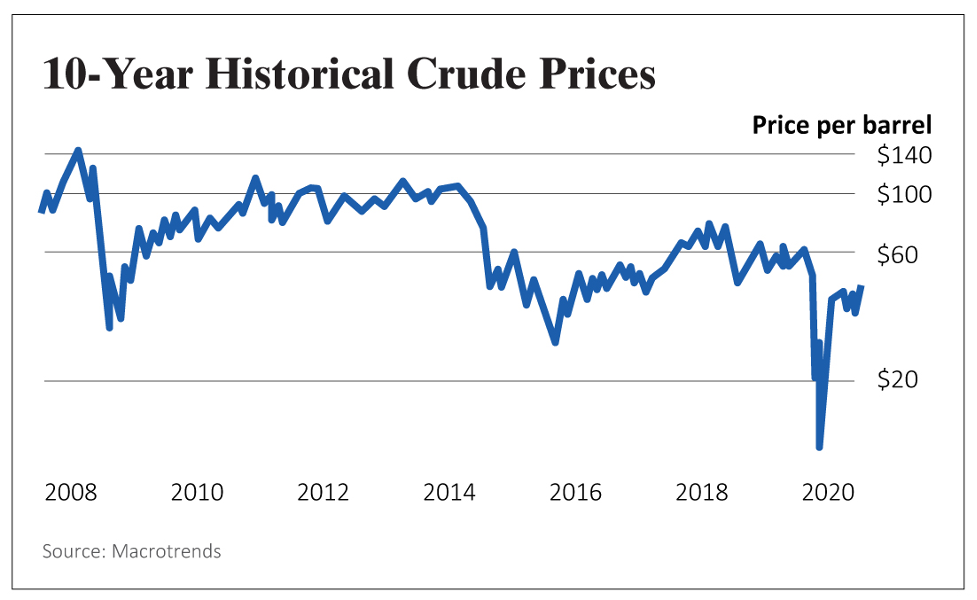

Before the pandemic unfolded, I thought crude was going to fall to $40 in 2020. COVID-19 just accelerated its drop.

But now I see a perfect opportunity for crude to rebound. Just like the rebound I told investors to buy into back in 2016 when crude tumbled to $26 per barrel.

For 2021, I’m predicting that U.S. crude not only will retake the $50 per barrel level – a level not seen since the early days of 2020 – but also will top $60.

Now, I’m not a fool. I don’t think pre-pandemic consumption will return. But I think we’ll now have a multiyear – albeit bumpy – rally in energy.

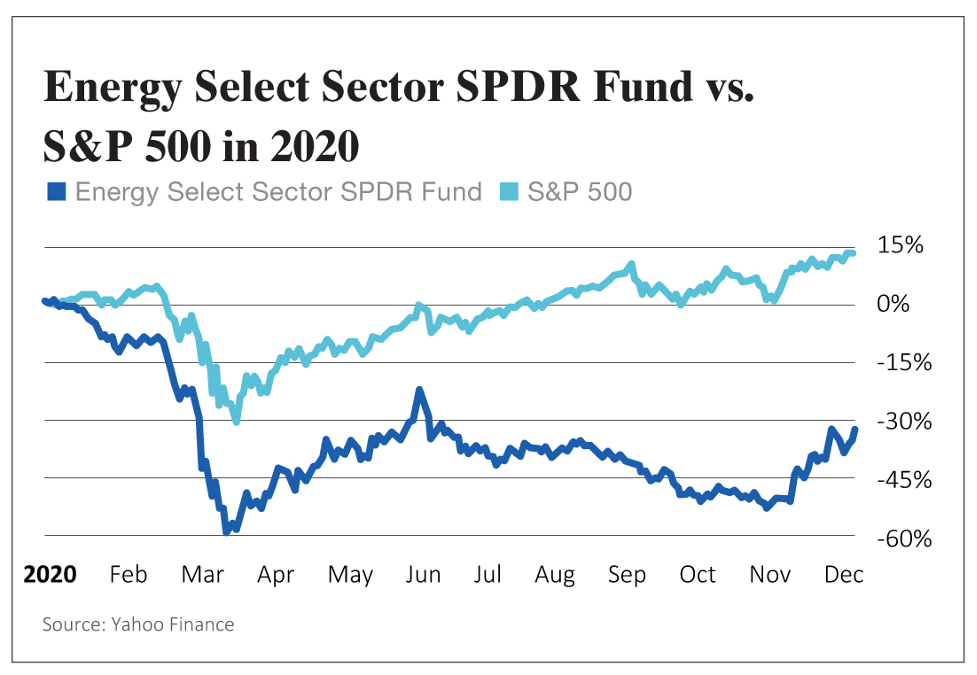

Due to the pandemic and the halt of the global economy, energy was the worst performer in 2020 by a considerable margin.

The Energy Select Sector SPDR Fund (NYSE: XLE) lost more than half its value this past year. And it’s still down more than 30%.

A lot of investors are terrified by energy stocks right now. But they don’t see that these are trading at a steep discount to their future growth.

And my personal favorite opportunity in this sector is Exxon Mobil (NYSE: XOM).

For those of you who aren’t familiar with the company, it explores and produces oil and natural gas in the U.S., Canada, Europe, Africa, Asia and pretty much any region of the world imaginable. Its proved reserves are more than 22.4 billion barrels of oil equivalent, and it has nearly 24,000 wells in operation worldwide.

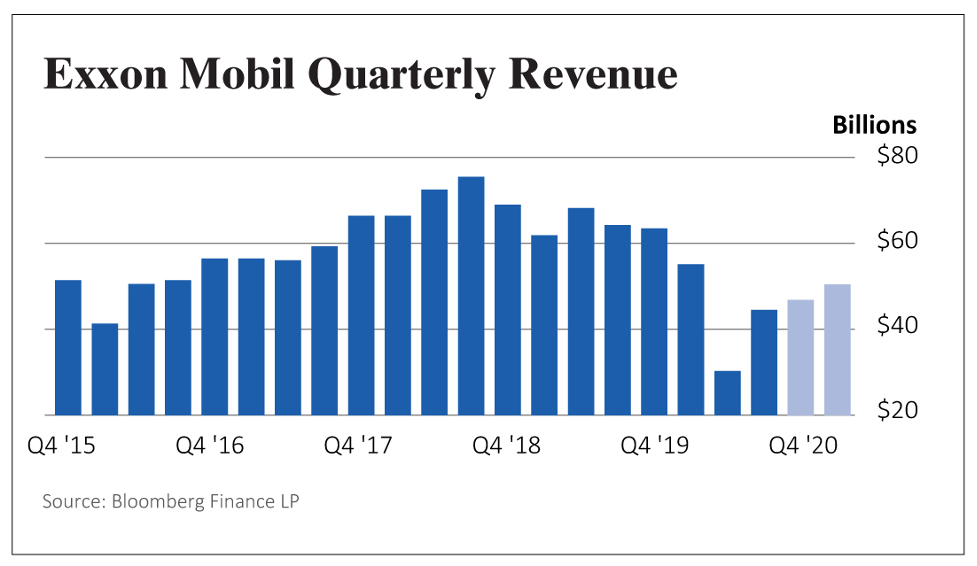

As the price of crude tumbled in 2020, so did this oil major’s shares.

Shares of Exxon shed more than 40% of their value in 2020. And they’re still trading at levels not seen since 2004.

Now, at the height of the pandemic, the company’s business was decimated.

In the second quarter, Exxon reported a loss of $1.1 billion as

But it’s since seen a dramatic rebound.

In the third quarter, Exxon’s loss shrank to $680 million as revenue came in at $46.2 billion. By no stretch of the imagination is that a rosy picture. But it was a major improvement from the second quarter, and the oil major’s business will continue to get better with each step closer to normalcy.

When all is said and done, Exxon is projected to report a 31.9% decline in revenue for 2020 to $180.51 billion. And the company is expected to report a loss per share of $0.42.

But with more than $180 billion in annual revenue, this company is far from going belly-up.

And for the year ahead, Wall Street is projecting revenue to increase 20.8% to $218.08 billion with earnings returning to a profit of $1.38 per share.

Exxon has survived recessions, oil shocks, and pretty much every financial and natural disaster that’s come along. The pandemic won’t end its reign. And that’s why I think this is another fantastic, undervalued opportunity where a LEAPS play can pay off big!

Action to Take: Buy the Exxon Mobil (NYSE: XOM) January 21, 2022, $45 calls. Be patient. Go as low as possible. This LEAPS play offers better upside than owning shares.

Dave’s Pick: A Delicious Opportunity

When searching for new investment ideas, I never used to pay much attention to the food industry. At least not until a few years ago.

Meat is big business. Globally, it’s a $2 trillion industry.

The world’s largest meat purveyor is JBS SA. It operates globally and has more than $50 billion in annual revenue.

Here in the U.S., we produce about 100 billion pounds of meat every year. And that’s growing at a rate of 2% to 3% annually.

That’s a big problem. You see, raising animals for food uses disproportionately far more land than growing plants.

Today, there are 19.7 million square miles of agricultural land in use globally. A full 77% of that is used to house and feed livestock.

But only 17% of our calories and 33% of our protein come from animals. Plant-based foods supply the rest.

By 2050, Earth’s population will hit 10 billion. That’s going to require 70% more arable land for food production.

This is clearly unsustainable. So what can be done?

In 2019, a company named Beyond Meat (Nasdaq: BYND) announced it had a sustainable solution to the problem. Its first product was a plant-based burger.

I’ve had plant-based burgers before, and they didn’t taste at all like meat. But Beyond Meat claimed its burger tasted, smelled and looked just like real beef.

That piqued my curiosity. I had to try one.

And I was pleasantly surprised. I could not tell the difference between it and a real beef burger. I smelled a big disruption coming to the meat industry.

Beyond Meat is leading that disruption.

Its plant-based products now include meatballs, sausages, crumbles, burgers and bratwurst.

In the second quarter of 2020, retail buying and freezer stuffing meant excellent results. However, the third quarter saw COVID-19 keep customers at home.

The company experienced a big drop in food service customer orders. But Beyond Meat president and CEO Ethan Brown is undeterred. In a recent press conference, he said, “We have not, however, blinked in our focus on the expanding long-term opportunity before us.”

Even in the midst of a pandemic, the company is seeing increased purchase frequency, buyer rates and repeat-buying rates. It invested in a new plant in Pennsylvania to increase production.

It believes that it can deliver long-term gains for its shareholders. So let’s time our investment for a post-pandemic leap in profits.

To do that, we are going to purchase a Long-Term Equity Anticipation Security option contract. Known as LEAPS for short, they are simply options contracts that have expiration dates of nine months or more.

Other than that, LEAPS are just like shorter-dated options contracts. They give buyers the ability, but not the obligation, to buy the underlying company’s shares.

I like to use LEAPS on companies that I’m extremely bullish on. They can provide outsized returns if your hunch is correct.

And the best part is, you tie up only a fraction of the money needed to buy the stock outright.

When picking an expiration date, I like to go as far out in time as possible. That gives us the most time to maximize our gains. In the case of Beyond Meat, that’s January 20, 2023.

I like to pick a strike price that’s anywhere from 10% to 20% higher than the current stock price. Beyond Meat shares are selling for around $138 as of this writing.

If we go 20% higher, we arrive at a strike price of $165. And the bid-ask spread (the cost of the contract) is between $41.35 and $43.55.

I always recommend using a limit order when buying any option and especially LEAPS. They trade much less frequently than short-dated options do, and a limit order will get you the best price.

Action to Take: Buy the Beyond Meat (Nasdaq: BYND) January 20, 2023, $165 calls. Please use a limit order and try not to pay more than $45 per contract.

Secure Your Retirement

We’ve all just survived a year none of us ever could have imagined.

But cue the uplifting music…

We now have not one but multiple vaccine candidates.

The stock market, buoyed by booming tech and the thriving stay-at-home economy, has soared to new all-time highs.

Unemployment is receding from its double-digit heights.

And despite the surge in new cases of COVID-19, there’s cautious optimism in the air.

The greatest disruption – and opportunity – that lies ahead is normalcy.

Or at least some semblance of it.

And this will lead to one of the largest economic rebounds in years!

That’s why Dave and I are excited about the long-term prospects for these three companies. And we believe these could help investors secure their retirements by leaps and bounds.

To me, it’s a no-brainer… These three companies are at the forefront of a return to normalcy.

So take a stake in these companies and set yourself up to profit as they return to their pre-pandemic glory days.

Here’s to high returns,

Matthew and Dave

P.S. To access the full Leaps and Bounds Portfolio, click here.