The Ultimate Trump Trades: Three Little-Known Ways to Ride the Small Cap Boom

When America wins, its investors can win big too. Under President Trump, the government is working to bring factories, jobs, and key industries back home. And that is creating a huge new shift in the U.S. economy. Some experts believe as much as $10 trillion could flow into American businesses over the next decade.

While the Trump economy will benefit large companies with government investment and policies friendly to their businesses…

It will also send smaller companies into the stratosphere.

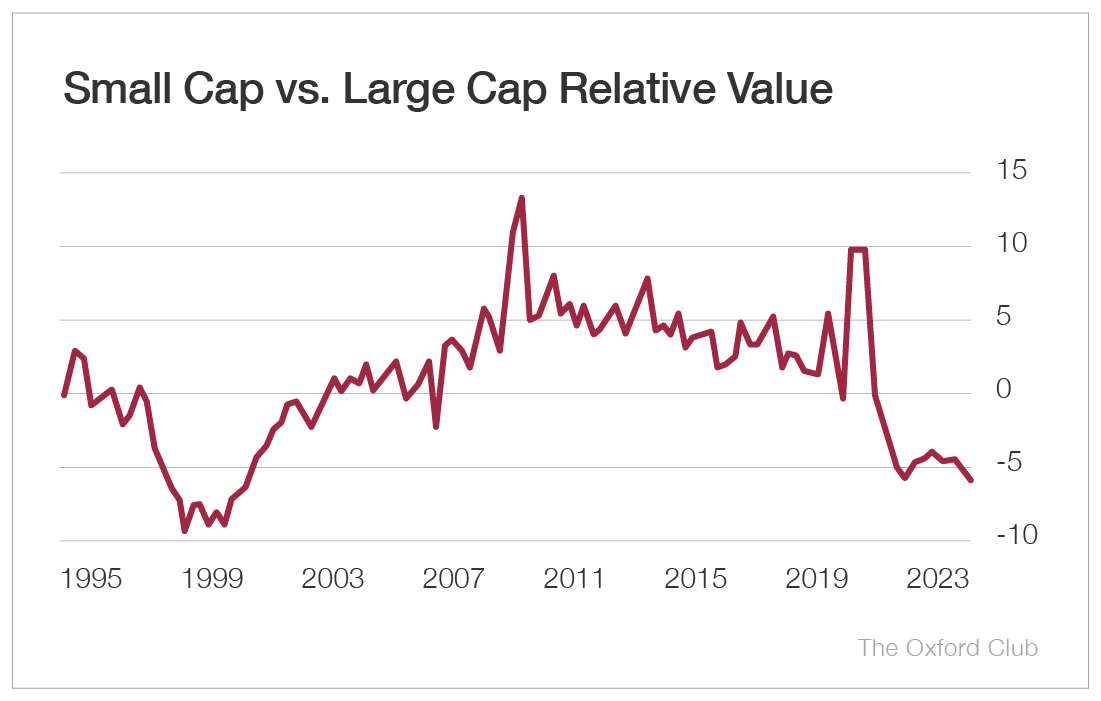

And a unique market anomaly is occurring right now that’s set to make small cap companies even more potent. There’s a historic valuation gap between small cap and large cap companies.

Small cap stocks are trading at historically wide discounts relative to large cap stocks. Previous periods of wide valuation gaps between small and large caps have often preceded extended periods of outperformance for smaller companies.

Middleby surged over 13,800%.

Tractor Supply skyrocketed 50,000%.

And Monster Beverage rose by a staggering 125,000%.

And now we have a second chance to buy into the small cap revolution by investing in innovative, small American companies. Pro-business policy proposals and renewed focus on domestic growth have historically favored smaller, more nimble companies.

It already happened once during his first term. The Trade Desk jumped 2,500%, Digital Turbine soared over 8,000%, and Enphase Energy returned 9,700%.

Make no mistake: The 2020s might be half over, but they still have plenty of time to roar like the 1920s…

In this report, I’ve made the case for three companies that are capable of the same sort of growth. I believe these companies have the potential for outsized long-term gains in the new “Renaissance of America.”

Fast-Moving Profits

Cloud computing is vital to the modern economy. Thousands of companies of all sizes use Amazon Web Services, Google Drive, and Microsoft Azure. Cloud computing represents one of the largest and fastest-growing segments of the global technology market.

And it’s San Francisco-based Fastly (NYSE: FSLY) that makes much of that cloud computing possible. It can claim Amazon, Google, and Microsoft as customers along with 3,092 other companies around the world. And 99% of those customers continue to renew Fastly’s services.

Fastly’s edge cloud network is designed to reduce latency and improve performance for modern applications. It processes trillions of requests across its global network. And it’s fast enough that 90% of its customers can run firewalls around their applications to keep them safe. The company’s technology portfolio is supported by a substantial patent base.

The company’s network is the best of all worlds. It’s fast, it’s safe, it’s easy to use, and it allows customers to save money compared with the costs of the competition.

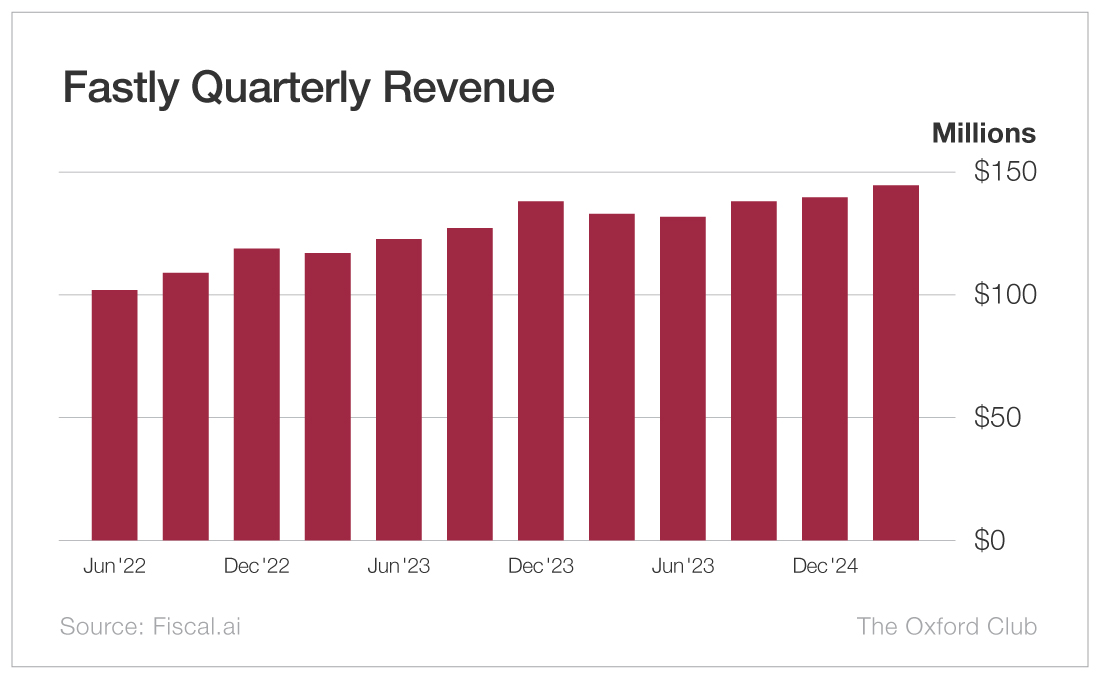

Despite all of that, the company has just a $3 billion market cap and trades for a microscopic price. But Fastly is putting up some serious numbers on its bottom line and, with its elite clientele, you can bet it won’t remain a bargain for long.

Fastly has generated more than half a billion dollars in annual revenue in recent years. And recent quarterly results have shown continued year-over-year revenue growth.

Fastly’s revenue growth has been on a tear for the past several years. Revenue has trended higher over multiple years as demand for edge computing expands.

The company maintains a solid liquidity position relative to its size. That’s a refreshing sight in an industry where so many companies, particularly smaller ones, are absolutely drowning in debt.

Combine the patents, the network, and the A+ client list Fastly has already put together with the explosive growth it’s been seeing, and you have a winner. At current levels, the stock remains modestly valued relative to its technology footprint.

Action to Take: Buy Fastly Inc. (NYSE: FSLY) at market.

In Good, Steady (Robotic) Hands

Medicine is one of the biggest market opportunities for robotics. And overworked doctors and nurses need all the help they can get.

The potential of this market propelled one of my best picks, Intuitive Surgical (Nasdaq: ISRG), to the moon. When I recommended it in 2004, it surged 309% over the next two years. It became the fourth-best-performing stock of the last 20 years, rising by 200-fold in all.

Intuitive’s groundbreaking DaVinci surgical robots allowed surgeons to perform more complex surgeries with less risk. Even the best surgeon’s hand might slip, or an older surgeon may not have as steady hands as he or she used to.

But surgical robots like DaVinci solve both problems, giving surgeons a precise tool and allowing older professionals with decades of experience to continue to perform operations.

And I believe Procept BioRobotics Corp. (Nasdaq: PRCT) is the next Intuitive Surgical. The company’s new surgical robot, the AquaBeam, is an image-guided robot meant to use minimally invasive surgery called Aquablation to treat BPH, the benign enlargement of the prostate.

Symptoms of BPH can seriously impact an individual’s quality of life. They range from difficulty urinating and kidney damage to bladder stones and urinary infections. Symptoms of the condition are present in 1 in 4 men aged 55 or older and half of men 75 or older. By age 80, 20% to 30% of men require treatment for the condition.

And surgery used to be the only solution, though it could lead to incontinence, erectile dysfunction, and sexual dysfunction. Enter Aquablation, which received FDA approval in December 2017…

It uses nothing more than a robotically assisted waterjet, and it’s heat-free. It also leads to much better outcomes. Only 1% of men treated with Aquablation had incontinence issues as a side effect… 0% developed erectile dysfunction… and only 11% had any lingering sexual dysfunction.

A treatment option that successful, with few side effects, is a winner for any biotech company. And Procept is no different. The company has been building momentum quickly and is about to take off.

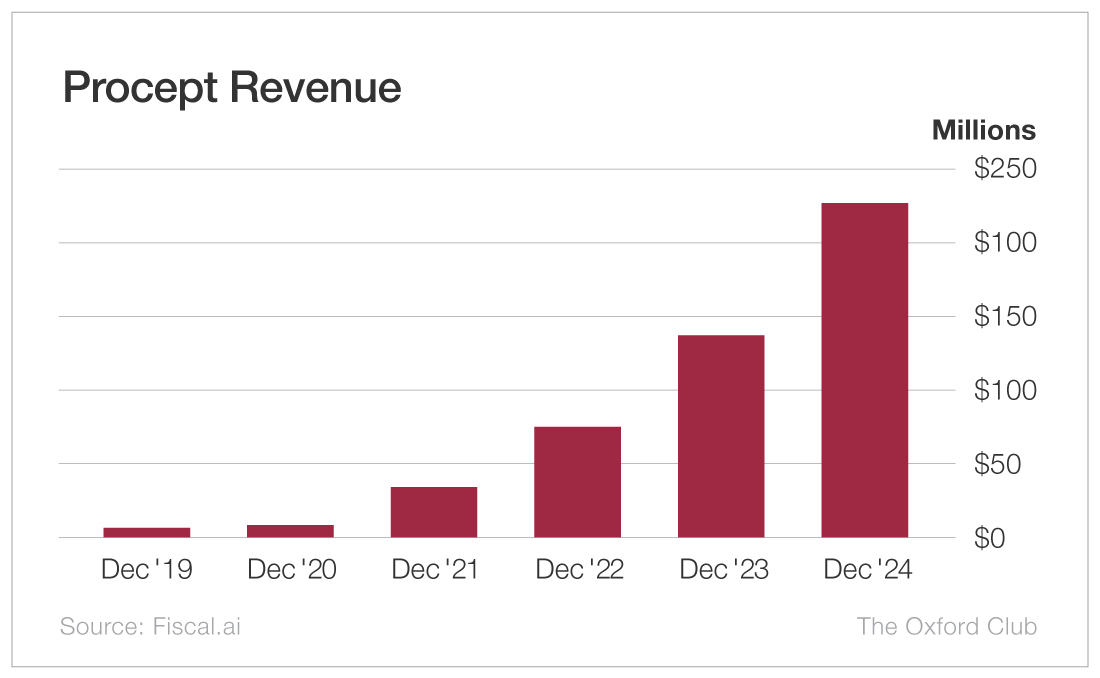

In the past five years, its revenue has surged at a CAGR of 55%. That rapid growth has continued, with Procept reporting Q1 2025 revenue of $69.2 million, followed by $79.2 million in the second quarter (up 48% year over year) and $83.3 million in the third quarter (up 43% year over year). For full year 2025, Procept generated $308.1 million in revenue, an increase of 37% compared with 2024.

The company maintains a strong balance sheet with ample cash reserves and healthy gross margins, supporting continued growth and adoption of its robotic platform.

Action to Take: Buy Procept BioRobotics Corp. (Nasdaq: PRCT) at market. Use a 25% trailing stop to protect your principal and your profits.

A King’s Ransom

One of the main planks in the Trump platform is to expand America’s capacity to drill and extract our vast oil reserves. So we can be sure the oil and gas industry will reap the biggest benefit from this administration’s agenda.

But finding out exactly where to drill can be a conundrum. The process of exploration, that is, finding new well locations, can be expensive, can be time-consuming, and can result in a loss if no suitable location is found.

That’s where royalties companies like Dorchester Minerals LP (Nasdaq: DMLP) come in. These companies own land where they know oil and gas is sitting beneath the surface. They charge extraction companies royalties (a percentage of the value of all oil and gas produced by the extractor from that land) for the right to drill.

And Dorchester Minerals is set to make a mint as oil and gas producers take advantage of Trump’s pro-energy policies to fulfill the commander in chief’s promise to “drill, baby, drill.”

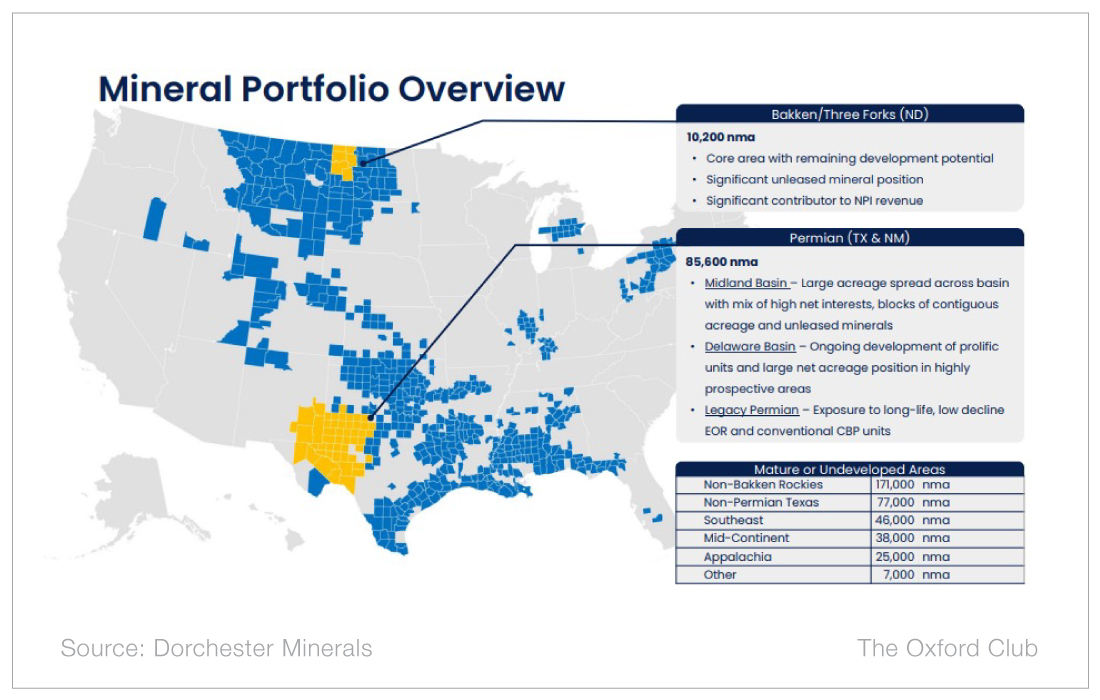

It holds land in 594 counties and parishes across 28 states, including two of America’s most productive oil and natural gas regions, the Permian Basin and the Bakken Formation.

Dorchester is essentially the oil industry’s landlord. Energy extractors pay it rent for the use of the land it owns, and Dorchester passes a large portion of that rent on to investors in the form of a hefty dividend. More on that in a moment.

As you might imagine, being the landlord to an industry that represents one of the largest and most economically significant industries in the U.S. And Dorchester’s balance sheet bears that out…

The company has exceptionally high gross margins, reflecting its royalty-based business model, a strong balance sheet, and a market capitalization that remains modest relative to its asset base. It generates $152 million annually without operating so much as a single oil well.

Over the past five years, revenue has risen at a CAGR of 10.3%. And that was under an administration dead set on hamstringing the oil and gas industry. Recent quarterly results have reflected higher royalty revenue driven by increased production and pricing.

But here’s where we get to the really good part.

Dorchester pays a variable dividend that has historically resulted in an above-average yield. And the company has grown its dividend per share by 9.9% over the last three years.

When you own shares in an LP, or limited partnership, you become a partner in its business. That gives you a right to guaranteed profit from its revenues. Dorchester pays that out through its fat dividend. This is why our strategy with this one will be a little different…

I expect Dorchester will see some solid share price growth over the next four years. But if you reinvest your dividends throughout Trump’s second term, you could be looking at a serious passive income machine. And with its share price going at bargain rates, Dorchester could provide an attractive income stream over time, particularly if dividends are reinvested.

Action to Take: Buy Dorchester Minerals LP (Nasdaq: DMLP) at market.

The Roaring 2020s…

These three companies may be small, but they have skilled leaders, growing sales, and solid business models. Because of their size, they have plenty of room to grow into much larger businesses as money and jobs move back to the United States.

This is a second chance to join a true small cap revolution.

A movement powered by Trump’s pro‑business agenda, a wave of investment returning to America, and a historic discount in small caps. In the past, investors who recognized moments like this early saw major gains.

The 2020s may be half over…

But there is still time for this decade to “roar” for investors who focus on the right small caps instead of chasing crowded mega‑caps.

And I believe that these three “Ultimate Trump Trades” are the best way to take advantage of the American Renaissance in small stocks.