Three Tax-Advantaged Investments That Pay Big Income Too

Focusing on dividend-paying investments is one of the great secrets to building wealth.

Unfortunately, Uncle Sam always wants a piece of those dividends…

And add to that the possibility for a lethal combination of runaway inflation and higher taxes on the horizon.

Thankfully, there are certain types of investments that pay big dividends… and help you keep more of them.

I’ve found three high-paying, tax-advantaged types of investments that protect your money from the taxman and fight the destructive effects of inflation.

They are master limited partnerships (MLPs), real estate investment trusts (REITs) and business development companies (BDCs).

While these types of investments are lesser-known and can be a little more complicated, they’re your best shot at avoiding a major retirement crisis.

In this report, I’ll explain how each of these investments work and how each can help you make more… keep more… and make it last.

Let’s start with the investment with the greatest tax advantage: MLPs.

Master Limited Partnerships

An MLP is a company organized as a publicly traded partnership.

MLPs have two types of partners: general partners, who manage the MLP and oversee its operations, and limited partners (you), who are investors in the MLP.

In general, MLPs are considered low-risk, long-term investments that provide a steady income stream.

The risk with MLPs is that since nearly all of the company’s profits are distributed back to shareholders, any decrease in earnings can result in a dividend cut.

However, most MLPs are formed to generate steady cash flows and consistent cash distributions. They earn a stable income based on long-term service contracts.

That’s what makes MLPs a great place to find attractive yields. Quite a few MLPs are currently sporting yields of 8% or more.

About 80% of MLPs are energy companies. Most of them are oil and gas pipeline companies that aren’t affected much by the price of oil or gas. Their businesses rely on the volume of product that flows through their pipelines.

Tax Treatment

MLPs do not have the same tax implications as most other stocks. In most stocks, you are a shareholder. In an MLP, you are considered a partner in the business.

An MLP has a special structure that bypasses corporate taxes because it passes along the majority of profits to unitholders in the form of a distribution.

A bit of lingo: MLPs have units, not shares, and pay distributions, not dividends.

This isn’t just jargon; there are important differences from a tax perspective.

What sets MLPs apart from many other tax-advantaged investments is those distributions…

The distribution most MLPs pay is usually 80% to 90% return of capital. Sometimes it’s 100%.

The return of capital lowers your cost basis.

I’m simplifying things with this example, but if you bought an MLP at $25 per unit and for 10 years received a $1 per unit distribution that was all return of capital, your cost basis would be reduced to $15.

Over those 10 years, you would not pay taxes on those $10 in distributions ($1 x 10 years). However, when you sold, you would pay a capital gain tax on the difference between $15 and the selling price.

If your cost basis eventually went down to zero, the income you received would be taxed from that point forward – usually at the capital gains rate.

MLPs can also be an effective tool for estate planning.

When an MLP investor passes away, the heirs inherit the stock at the market price at the time of death (similar to a regular stock). So the cost basis, which had been lowered, is adjusted to the price at the investor’s death. It’s like resetting the meter.

The reason it can be effective for estate planning is it may allow the original investor to collect years of tax-deferred income. When they pass, no taxes are collected on that income and the heirs start all over again.

Keep in mind that each MLP is different. Each will have its pros and cons, and the distribution may vary from year to year.

Be sure to read the investor relations page of the website of any MLP you are considering investing in to get a thorough understanding of the way the company pays distributions.

Talk to your tax professional before investing in MLPs, because the tax implications can be complex.

Additionally, you’ll receive a K-1 tax form from the company, which is different from the 1099-DIV that you get from regular dividend-paying companies.

The fact that the majority of MLP cash distributions are not taxed at all when unitholders receive them makes MLPs very appealing.

All things considered, MLPs are a worthy consideration for income-oriented and tax-reduction-focused investors.

Real Estate Investment Trusts

If you’re looking for a way to keep Uncle Sam’s greedy hands off some of your income, I urge you to take a serious look at REITs.

This is a very popular investment for income investors looking for high yields and favorable tax treatment.

For just a few dollars per share, you can essentially become an owner in real estate all over the country.

The managers of these trusts are industry experts with years of experience and dozens of staff at their disposal. They’re tracking down the best real estate bargains on the market.

Which makes your decision easy…

You don’t have to manage properties… fix even a single leaky faucet… or chase down checks from flaky tenants.

And here’s the beauty of this situation.

You can purchase a REIT and sit back and collect fat dividend checks – many REITs today are paying 5%, 6%, 7% or higher – that often include favorable tax treatment!

REITs do not pay corporate taxes and instead must pay out 90% of their profits to shareholders in the form of dividends.

In other words, they’re passing along a large portion of their rent checks to YOU!

And with REITs, there’s also huge capital gains potential.

The REIT Choice

There are REITs for nearly everything: those that specialize in apartment buildings, office buildings, shopping centers, hospitals, medical offices, nursing homes, data storage centers and more.

That’s why REITs can be volatile. Just like other industry sectors in the economy and the stock market, the real estate market has its booms and busts.

If real estate values fall, so will the net asset values of the properties a REIT owns. Additionally, a weak economy can lead to a greater number of vacancies – reducing profits and, as a result, the dividend.

A change in interest rates may make borrowing money more difficult for the REIT, lowering its growth rate or making it tougher for its tenants to pay the rent.

Of course, the opposite is true. For instance, in 2021, we saw a boom in the residential real estate market.

As a result, the MSCI US REIT Index was up 43.06% in 2021. And many sector-focused REITs appreciated considerably more than this all-encompassing index.

Looking at the big picture… I expect REITs to be a great place to invest in the coming years.

As inflation heats up and interest rates rise… REIT dividends will go even higher.

Tax Treatment

REITs offer some special tax treatment that makes them unique.

First, the bad news about REIT dividends…

Most REIT dividends are taxed at your ordinary income tax rate, which is going to be higher than the qualified dividend tax rate.

For example, if you own stock of a regular corporation, like Microsoft (Nasdaq: MSFT), and get paid a dividend, that dividend is taxed at the qualified dividend tax rate of 0% for lower income earners to 15% for most investors, or up to 20% for high earners.

But the good news is that REIT dividends provide other tax advantages that reduce your taxable income.

Some REIT dividends, or a portion of the dividends, may be qualified dividends. A qualified dividend is subject to capital gains tax rates that are lower than the income tax rates applied to ordinary dividends.

Plus, a portion of the income you receive may be considered return of capital, which would be tax-deferred and would lower your cost basis.

And some REITs have a unique tax advantage that comes into play…

Some REIT dividends also qualify for a Section 199A deduction. In those cases, investors can deduct up to 20% of their REIT dividends from their taxable income.

With all the potential advantages of REITs – qualified dividends, Section 199A deductions and the juicy yields – you’ll often end up with more money in your pocket investing in them than you would investing in a typical dividend-paying stock.

(And don’t forget the significant capital gains potential!)

Plus, the returns from just about any REIT are going to be more than the puny returns from a bank savings account or mutual fund money market account.

If you wanted to try to find the most favorable REITs from a tax perspective, websites focused on REITs typically provide information on past dividend payments and the portion that qualified for special tax treatment. Once you’ve invested, your brokerage firm will send you a 1099-DIV at the beginning of the year, indicating how the previous year’s dividends should be treated.

Business Development Companies

America’s richest citizens have tapped this strategy for years to build their fortunes.

It allowed billionaire and venture capitalist Peter Thiel to grow a $500,000 grubstake into $1.7 billion in just six years…

Thiel was able to create that fortune using a method that was – until recently – off-limits to regular investors.

Thiel invested in private equity – shares of companies that are not listed on a public exchange.

For years, only institutional investors, pension funds, large banks, hedge funds, and the seriously rich and powerful were allowed to invest in these private companies (due to the Securities and Exchange Commission’s “accredited investor” requirement).

That’s how Thiel became the first outside investor in Meta Platforms (Nasdaq: META) – then called Facebook.

Most individual investors are still excluded from participating directly in these private equity offerings.

But thanks to BDCs, there’s a way for you to get in the game… collect huge dividends… and receive tax advantages.

What’s the Strategy?

BDCs are publicly traded investment companies that provide debt and equity capital to small, privately owned enterprises.

BDCs are not like most stocks trading on the New York Stock Exchange (NYSE) or Nasdaq. In addition to their investments in private equity, they also actively invest in stocks, fixed income, turnarounds, restructurings and real estate.

Some BDCs specialize in certain sectors, such as biotech, technology or retail. Others are generalists, entertaining opportunities wherever they lie.

This multipronged approach provides investors with plump annual dividend yields and terrific capital gains potential.

We all know how wealthy you could have become if you had invested in Microsoft and Apple (Nasdaq: AAPL) when the companies had their initial public offerings. Imagine how rich you would have been if you had invested even before they went public.

When early-stage companies are private and raising money, they can still sell shares, just not to the public in the markets. They sell them to BDCs and other accredited investors in privately arranged transactions.

Those equity positions can become very lucrative as a company matures, and particularly if it goes public.

Sometimes BDCs lend money to a startup (or even more mature companies) instead of taking an equity position. For early-stage companies with little revenue, getting a loan from a bank is nearly impossible… so they go to BDCs.

A BDC may lend money to a startup at, let’s say, 13% annual interest, even though the standard bank business loan might be at 8%. Since the startup can’t get a bank loan, it has to pay the higher interest rate since the risk is larger. The BDC then passes most of that (at least 90%) higher income along to shareholders.

The Role of BDCs in Your Portfolio

BDCs diversify your portfolio in several ways. As a form of private equity, BDCs provide the diversification of an alternative investment – one that doesn’t necessarily move in harmony with the overall stock market.

Through their other businesses in real estate, lending, bonds and alternative investments, they provide exposure to many vibrant segments of the economy. That’s not something you can get from most stocks.

In addition, because many BDC portfolios are stuffed with high-interest loans, profitable fixed-income investments and steady management fees, you can also look at the shares as a kind of high-yielding investment…

One that’s capable of expanding its dividend distributions and providing tax advantages along the way.

However, all BDCs are not the same…

Keep in mind, BDCs that specialize in equity investments may have more inconsistent dividends, as their payout could depend on when they are able to sell their positions.

If a BDC sells $10 million worth of stock in one quarter and only $2 million worth in another, depending on the company’s dividend policy, the dividend may fluctuate.

However, a BDC that makes a lot of equity investments may have more upside potential or some very strong yields during good years.

BDCs that specialize in making loans to companies may have more reliable dividends, as they can pretty much project what their income stream will be from loan payments (assuming the default rate isn’t higher than expected).

So in that case, you may have less upside but more consistency when it comes to income.

Many BDCs pay a healthy yield, but as with any investment, the higher the yield (or potential reward), the higher the risk.

So if you’re considering investing in a BDC with a high yield, do your homework on the company, see how consistent the dividend has been and try to determine whether it will be sustainable.

If a BDC has a long and consistent track record, you should have a bit more confidence that it can continue paying the dividend.

Tax Treatment

As with a REIT’s dividend, a BDC’s dividend is treated differently by the IRS.

Because of the way they are structured and regulated, BDCs aren’t considered taxable entities.

In exchange for this favorable tax treatment, a BDC must distribute at least 90% of its profits to shareholders. Most pass an even higher percentage of the profits on.

Generally, you’ll be taxed on the kind of income the BDC received…

- If it earns interest on a loan, you probably will be taxed on that portion as ordinary income.

- If it sells a company for a capital gain, you will be taxed on that portion at the capital gain rate.

When you are investing in a BDC, look at its payment history and method of payment and choose a BDC depending on what should be most tax-advantageous for your circumstances.

The BDC reports income to investors as dividends on a 1099 form (rather than a K-1, which is used by REITs).

Once you’re a shareholder, you should receive a statement from the BDC every year with the payment breakdown, so you’ll have all the information you need when filing your taxes.

Because BDCs can generate high income (I’m seeing many double-digit yields currently), have large capital gains and have tax-preferred treatment… they are attractive choices for almost anyone who can tolerate higher risk.

I generally suggest buying BDCs in tax-advantaged accounts, like IRAs, where the aggressive income-producing tactics can benefit from compounding.

It’s Time to Tax-Manage Your Portfolio

You can’t reach financial independence as quickly if you’re surrendering too much of your annual returns to the taxman.

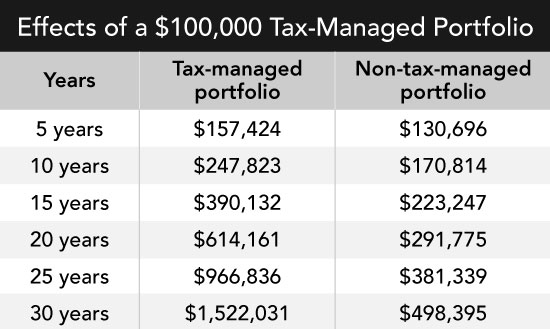

Let’s say one investor owns a $100,000 tax-managed portfolio. Another invests the same amount but is surrendering a total of 4% more each year in taxes.

Even if both portfolios have 10% gross annual returns, the results over time become dramatically different.

The investor who keeps their taxes to a minimum ends up with a portfolio worth more than three times as much… and that’s without generating gross returns that are any better!

Clearly, if you’re not doing everything possible to minimize your taxes – whether it’s using MLPs, REITs, BDCs or another tax-reducing investment strategy – you’re at a serious disadvantage.

Big Income and Important Tax Advantages

MLPs, REITs and BDCs can be excellent ways to add yield to your income portfolio and provide tax advantages.

Many of these investments generate a ton of cash and must pass that cash along to shareholders and unitholders. That’s why they are able to pay investors more than most other income-generating investments.

MLPs, REITs and BDCs, by the laws of their corporate structures, must return profits to shareholders.

Keep in mind that such investments can be volatile, as they are usually concentrated in one (often cyclical) sector and have more complex tax ramifications for shareholders.

But if you don’t mind doing a little homework and talking to your tax professional (or handling it yourself with tax software), these investments can be an excellent way to boost the amount of income you receive every year…

And thanks to their tax-favorable distribution methods, they help you keep more of that income!

With mounting inflation and higher taxes looking inevitable… these types of investments are crucial to ensure your income and grow your wealth.

(Again – and I can’t stress this enough – talk to your tax professional about any questions you may have. Each of these investments provides unique benefits and risks. It’s up to you to decide which work best for you.)