The Ultimate Gold Royalty Stream:

Earn Huge Income From the New Gold Bull Market

We’re seeing a monumental shift in the gold market right now.

The last time this happened, it preceded gold’s biggest bull market in history. During the 1970s, gold went from about $35 an ounce all the way to a high of $878 on January 21, 1980.

That’s a more than 2,400% gain in just 10 years.

Billionaire hedge fund founder Ray Dalio says he sees a “paradigm shift” in the gold market, similar to what happened in the 1970s after President Nixon took the dollar off the gold standard.

Hedge fund manager David Einhorn, founder of Greenlight Capital, also sees gold going “higher, perhaps much higher.”

Now, while bullion, gold ETFs, and mining stocks might do well…

I believe royalty streams are a far better way to profit from this new gold boom.

Royalty streams allow you to diversify your holdings across several mining stakes, so they’re much lower-risk than investing in a miner… and they can generate far bigger gains than simply buying gold.

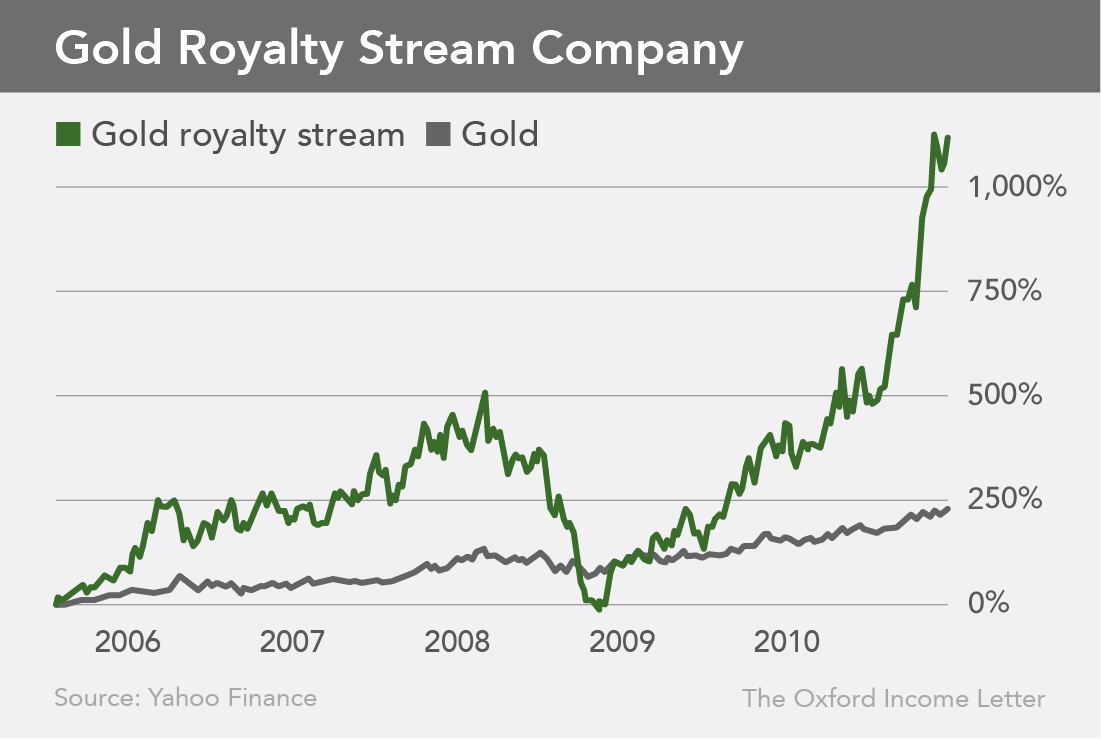

For example, between 2005 and 2010, gold went on a big bull run, gaining 211% in just five years.

Not bad.

But the gold royalty stream company in this report rose 1,108% over the same period!

This royalty stream gained five times as much as gold…

Without options or any type of risky leverage!

In 2025, gold gained nearly $1,700 per ounce − an astounding 64% rise. That was its largest annual increase since 1979.

Yet it still couldn’t manage to outperform our royalty streaming company, which gained over 109%.

I expect another strong year for the yellow metal in 2026… and Wheaton Precious Metals (NYSE: WPM) is the company to add to your portfolio to profit from it.

A River of Gold

Based in Vancouver, Canada, Wheaton Precious Metals isn’t a mining company. It’s a precious metals streaming company.

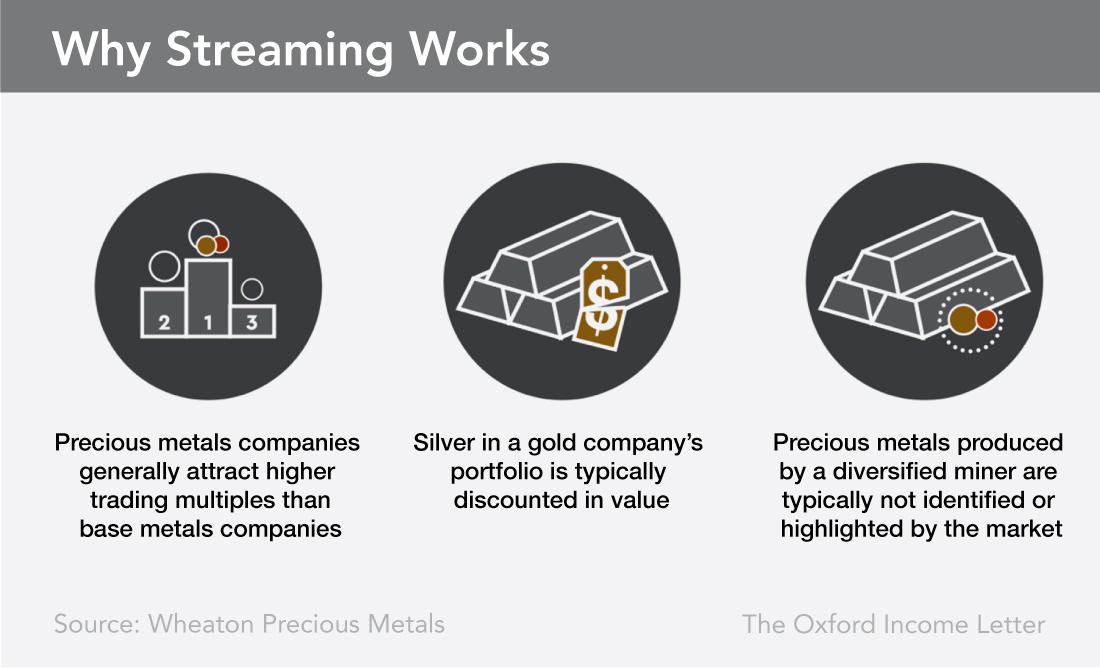

See, most mining operations are focused on one or two metals – gold, silver, copper, cobalt, etc. However, those minerals are rarely alone in the ground. Different metals are often found lumped together. For example, gold is usually found with silver, lead, zinc, and copper.

A gold mining company makes most of its money by selling the gold it digs up, but then it’s left with all the silver, lead, zinc, and copper that it spent time and money to extract along with the gold.

That’s where Wheaton comes in. Streamers like Wheaton give capital to miners upfront, and in exchange, they receive the extra metals those miners have no use for. They then sell those metals on the market and pocket the cash just as a miner would.

For example, if a company is mining for copper, it may get some gold that it won’t have much use for. The streaming company will buy that gold (guaranteeing that the copper miner can make some profit on it) and then sell it for a higher price at market.

In addition to locking in guaranteed profits, the miners are insulated from potential downturns in the market prices of those minerals and no longer have to worry about offloading the minerals they aren’t targeting in their mines.

Wheaton buys gold, silver, nickel, cobalt, and other minerals directly from miners at contractually agreed-upon, below-market prices. That means it has very predictable costs and high profit margins, and it’s able to profit from mining operations while taking on none of the risk.

As with oil and gas extraction, mining is a risky business. You may open a mine only to learn its reserves are much lower than previously thought − never mind the overhead of mining equipment, staff, taxes, and environmental regulations that miners have to deal with.

On the other hand, Wheaton simply moves the minerals, collects a profit, and then gives the money back to its shareholders through a dividend check.

It’s essentially a mineral royalties company, just as Texas Pacific Land (NYSE: TPL) collects oil and gas royalties tied to its land holdings. But what sets Wheaton apart is that it’s incredibly well diversified − both in the geographical distribution of the mines it works with and in the types of minerals it buys and sells.

Stream Some Profits Into Your Portfolio

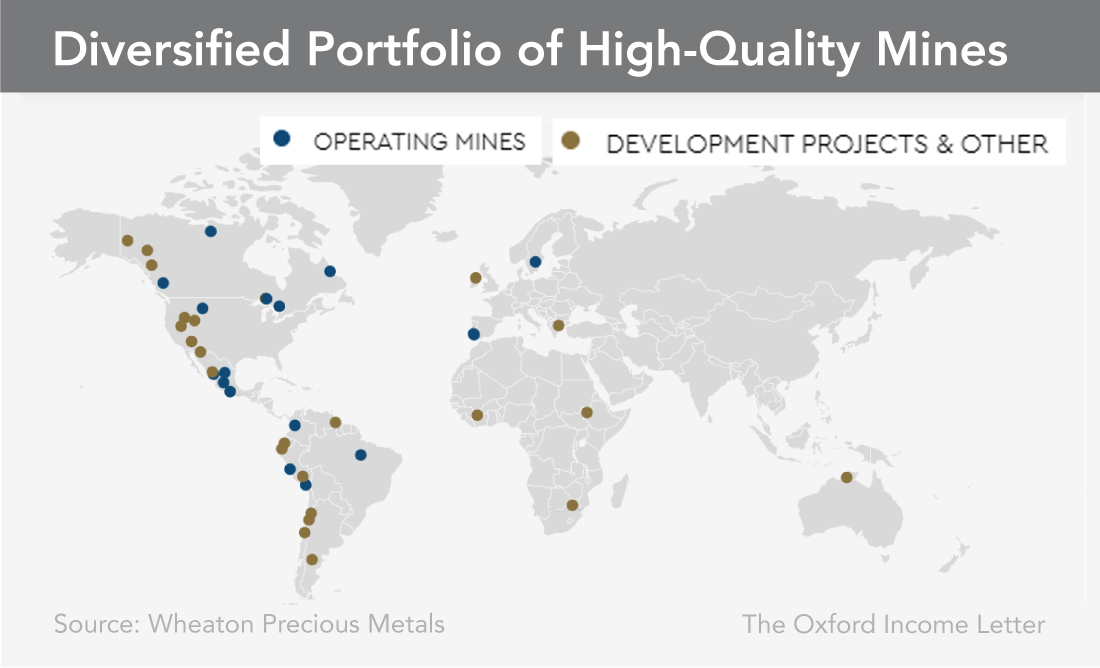

Wheaton is one of the largest precious metals streaming companies in the world. It has streaming agreements with 23 operating mines and 25 development projects across the Americas, Europe, Africa, and Australia.

Those mines produce gold, silver, cobalt, palladium, and platinum as byproducts of the minerals they’re actually mining for… and Wheaton buys them all and sells them.

The company has been in business for over 20 years, yet it remains just as nimble and entrepreneurial as it was in its first year. Despite the entry of more than 20 new competitors into the streaming business, Wheaton continues to be a leader and maintains 40% of the market share.

It generated over $1 billion in operating cash flows in 2024, a new annual record… and then nearly doubled that record by bringing in over $1.9 billion in 2025.

During times of global turbulence, gold is seen as a store of value and a comfort metal of choice. As a result, the company has benefited from high gold prices and strong central bank purchases over the past few years.

Although high gold prices bring challenges in finding new streaming partners due to the impact on valuations, Wheaton has skillfully added high-quality streams over the past few years. Its Montage-Koné transaction in 2024 was the largest precious metals streaming transaction by one company in close to a decade, and the $4.3 billion deal it signed regarding Peru’s Antamina mine in February 2026 was the largest precious metals streaming transaction of all time.

Wheaton also expects to collect “immediate production and cash flow” from its November 2025 agreement on the Hemlo mine in Ontario. As of the end of 2025, it is sitting on $1.2 billion in cash, meaning it’s well positioned to add to its portfolio.

The company’s revenue mix in 2025 was focused on gold and silver, but it included a few other metals as well. Of Wheaton’s record $2.3 billion in revenue, 62% came from gold, 36% came from silver, 1% came from palladium, and 1% came from cobalt.

Geographically, revenues are even more diversified. They’re split primarily among Brazil, Mexico, Peru, and Canada. The rest come from Europe, the U.S., Colombia, and Ecuador.

The company has partnered with some heavy hitters in the mining industry, like Newmont (NYSE: NEM), B2Gold (NYSE: BTG), and Barrick Mining (NYSE: B). It has had gold, silver, and even cobalt streams from those mines.

The cobalt produced as a byproduct of nickel mining in the Voisey’s Bay Mine in Canada is particularly interesting. Cobalt is one of the most vital minerals for producing electric vehicle (EV) batteries. Most of the world’s supply comes out of the Congo, but it’s a scarce resource that will go up in value as the EV market booms in the coming years.

That being said, gold and silver are the meat and potatoes of Wheaton’s business.

Wheaton’s average cost per gold equivalent ounce was $597 in the fourth quarter, up 34% year over year. That resulted in a cash operating margin of $3,941 per gold equivalent ounce sold, an increase of 76% from the previous year. The company also brought in a strong $746 million in operating cash flow during the quarter, representing terrific year-over-year growth of over 134%.

Most impressively, Wheaton set new records for revenue, net earnings, adjusted net earnings, and operating cash flow in both the fourth quarter of 2025 and the full year.

It returns some of that money to shareholders in the form of a quarterly dividend. Wheaton announced on March 12, 2026, that it had raised the dividend from $0.165 to $0.195 per share, which equates to a 0.56% yield and 18% growth from 2025’s payout. The company has raised the dividend nearly every year for the past decade, and its payout ratio based on free cash flow is just under 53%. (I generally recommend reinvesting the dividends to take advantage of compounding, but do whatever is best for your financial situation.)

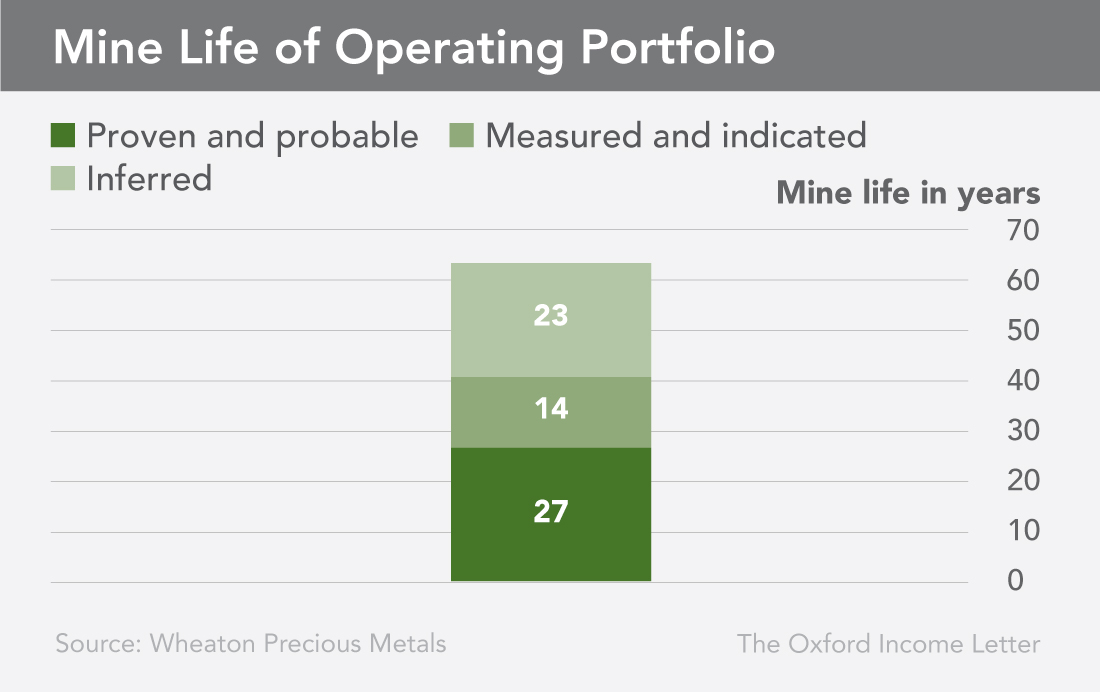

Wheaton should continue paying − and raising − those royalty dividends for the foreseeable future. Annual production is projected to increase 50% by 2030, and the company’s streaming partners have over 60 years of reserve and resource mine life remaining, between “proven and probable,” “measured and indicated,” and “inferred” resources.

If you buy Wheaton today, you’ll collect royalties for years to come on a river of gold and silver that miners of other metals are eager to sell. In the short term, the gold bull market should cause Wheaton’s share price to surge.

Profiting From the New Gold Bull Market

The stage is set for the gold bull run to continue deep into 2026. The bullion boom of the 1970s could repeat itself.

Gold is an effective long-term inflation hedge, and with inflation still elevated − and with interest rates likely to be lowered this year − protecting that buying power is still on everyone’s mind.

We should also see increased demand for gold from China, whose reserves surpassed $200 billion and then $300 billion in value in 2025. Additionally, central banks around the world are buying more gold as they seek to manage currency and geopolitical risks. In fact, 2024 was the third consecutive year that central banks bought more than 1,000 metric tons of gold. While that figure dipped slightly to 863 metric tons in 2025, it was still at the upper end of the expected range and well above the historical average, suggesting that there’s still plenty of demand to push prices higher.

Lastly, with persistent threats of tariffs, tensions with China, and the always-tenuous situations in Russia and especially the Middle East, the geopolitical climate remains uncertain.

When there’s trouble, people flock to gold… and Wheaton is the best way to profit from it.

During the last gold bull market from 2005 to 2010, it shot up 1,108%. That’s five times gold’s 211% return… all without options or risky leverage.

If you’re looking to diversify your royalty streams after picking up some oil and gas royalties, Wheaton is the way to do it.

Recommendation: Buy Wheaton Precious Metals (NYSE: WPM) at market.