The Perfect Time to Be a Fixed Income Investor:

My Top Three Corporate Bonds for Today’s Market

Thank you for being a loyal Oxford Bond Advantage subscriber. If you visit the portfolio page on our website, you can see that the portfolio is quite large. That’s because when we buy a bond, we expect to hold it until maturity. If we have an opportunity to take a quick gain, we will do so if it makes sense. But most of the time, we’ll hold the bond until it matures.

I am always adding new bonds, so the portfolio grows in size.

Because there are so many bonds that are rated “Buy,” I have selected my top three corporate bonds to help you determine where to put new money to work. They have different risk levels, so be sure to diversify your holdings. Don’t simply chase the highest yielders, as they often carry higher risk.

That being said, there hasn’t been a better time to be in bonds in years. Interest rates are at their highest levels in a long time. Just a few years ago, you had to take on significant risk to generate any kind of income. Today, you can get quality corporate bonds that should generate substantial income and return 8% per year or higher – without taking the risk of investing in stocks.

Remember, no matter what happens with a company – whether its earnings go up or down, whether its margins grow or shrink, or whether analysts love or hate the stock – as long as the company doesn’t go bankrupt, bondholders will get paid in full at maturity. And if we buy the bonds at a discount (as we usually do), we’ll even make a little profit in addition to all of the interest we get paid.

My top three corporate bonds are in three different sectors that should do well. They’re the bonds of a discount retailer, an energy company and a company that invests in other businesses.

Our discount retailer should do well in good times and bad. The energy company should perform very well in the coming commodities supercycle. And our investment company has a long history of providing successful businesses with capital in all kinds of economic cycles.

When investing in bonds, be sure to diversify. As with stocks, you don’t want all of your holdings in just one or two bonds. So leave some capital aside for new bonds that will be coming your way.

But these top three are an excellent place to put new money to work.

The Merchandise Isn’t the Only Thing That’s a Bargain at This Retailer

Kohl’s is one of the largest department stores in the United States with more than 1,100 locations in 49 states. The company offers a wide range of products, including footwear, apparel, household items and beauty products.

Its prices tend to be low, and fortunately for us, so are the prices of its bonds.

That’s why I am recommending the Kohl’s (CUSIP 500255au8) July 17, 2025, 4.25% coupon bonds.

With the bonds trading at a discount to par value, we can now lock in a very secure minimum expected annual return (MEAR) of 8.5%. (I show how the MEAR is calculated below.)

One thing I love about these bonds is the incredible value of the Kohl’s real estate portfolio that underpins them.

Against the total $1.9 billion in long-term debt that Kohl’s currently has, the company’s owned real estate is worth more than $8 billion. For Kohl’s bondholders, that means there is more than $8 of collateral available for every $2 of debt the company has.

That real estate value means we have an incredible amount of security supporting our bonds.

Unquestionably, this real estate value is what attracted multiple different parties trying to acquire Kohl’s in 2022.

It was reported that the company was approached separately by Sycamore Partners, Starboard Value, Franchise Group, Simon Property Group and Brookfield Asset Management – all with offers in excess of $9 billion.

Those $9 billion offers provide us with multiple independent data points again confirming the significant value of the real estate.

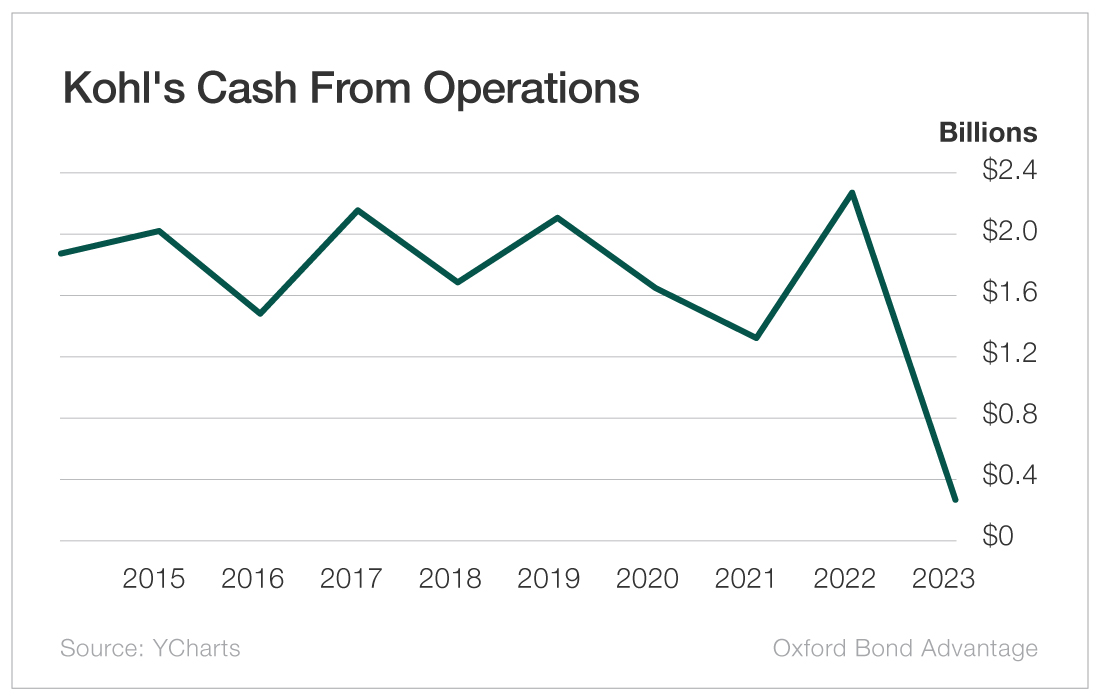

Operationally, last year was not terrific for the Kohl’s business. For a decade, Kohl’s had recorded annual operating cash flow that stayed in a narrow range around $1.8 billion.

In 2022, operating cash flow fell to under $300 million.

I don’t expect future years to look like 2022. The main driver of the 2022 cash flow decline was the company taking extremely aggressive markdowns on clearing out excess inventory.

Having to take those markdowns to clear inventory isn’t good, but it isn’t something that should have to be repeated.

With the excess inventory gone, Kohl’s profit margins should return to a more historical level.

The timing of these inventory write-downs coincides with the arrival of new CEO Tom Kingsbury. Often, when a new CEO arrives, a company has a “kitchen sink” set of financials where everything that can be written off is written off.

This gives the new CEO a fresh start and every chance to succeed.

Kingsbury seems pretty sold on the idea that Kohl’s cash flow is going to bounce back to normal levels. Immediately after the disappointing 2022 numbers were released, he went out and spent $2 million of his own dollars buying shares of Kohl’s.

You can’t get a more bullish indicator than that.

The company just renewed its $1.5 billion credit facility with its bank with a 2028 maturity date. That gives the company plenty of liquidity well past the 2025 maturity date of the bonds we are buying.

I expect Kohl’s business to rebound from this one bad year. But honestly, we don’t really need it to. With the liquidity that the company has, the repayment of our bonds shouldn’t be a problem.

Plus, with the huge amount of value in the company’s real estate acting as collateral, these bonds should be just fine in all possible scenarios.

Action to Take: Buy the Kohl’s (CUSIP 500255au8) July 17, 2025, 4.25% coupon bond. The bond is rated BB by S&P Global Ratings.

At the current trading price of $92, you will lock in a MEAR of 8.5%. You will receive five interest payments of $21.25, minus $9.90 in accrued interest, plus a gain of $80 at maturity from buying at a discount to face value, for a holding period of 27.19 months at a cost of $920 per bond.

5 x 21.25 – 9.90 + 80 / 27.19 / 920 x 12 = 8.5%

(For the sake of simplicity, the equation above is calculated from left to right rather than using standard order of operations.)

A Safe Energy Play in a Booming Industry

There are events that transpire after which everything is forever changed.

For the global natural gas market, such an event happened the moment Russia invaded Ukraine.

From now on, the world of natural gas will never be the same.

With the Russian invasion, a long-known weakness in European energy security immediately came front and center. Europe is desperately dependent on Russia for natural gas.

Prior to the invasion, a staggering 45% of this vital commodity that Europe was using came from Russia.

This meant that on a daily basis, almost half of the European continent was at the mercy of Putin cutting off the heat from their homes and the power to their businesses.

It is a powerful weapon in his hands.

Can you imagine if half of the United States relied on Russia to provide the energy that heats our homes in the winter?

No, I can’t either.

Europe’s reliance on Russia was always an uncomfortable position. With Putin’s invasion of Ukraine, we know that it is a completely unacceptable position.

The leverage that Putin has over our European allies is severe. It needs to be eliminated… permanently.

That is why, in March 2022, President Biden announced an agreement for the United States to massively ramp up the natural gas that it supplies to Europe.

We are going to make it so Europe doesn’t need Putin’s energy.

Biden committed an additional 15 billion cubic tons of liquefied natural gas (LNG) to be delivered to Europe through the remainder of 2022, plus another 50 billion cubic tons annually by 2030.

When the war ends, Europe will happily not have to go back to being reliant on Russia for this commodity.

This is a permanent change in market dynamics and very, very good news for American natural gas producers.

Increasing LNG exports to Europe means there is going to be a lot more demand for their product coming.

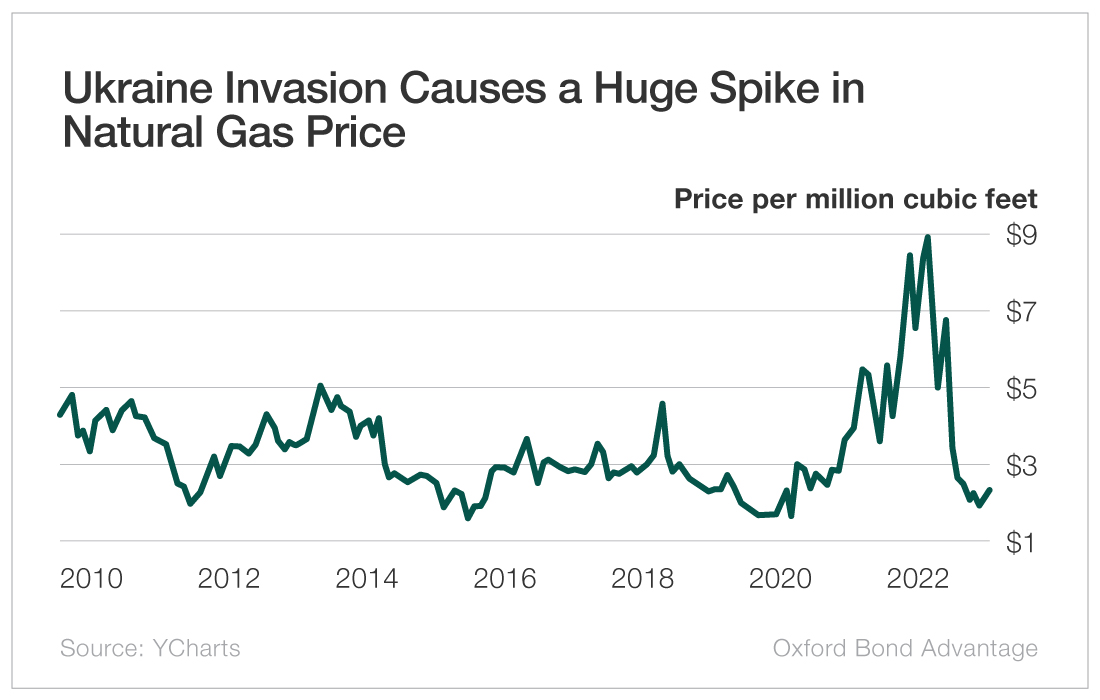

It was good news on top of a year that was full of good news for the LNG industry. In 2022, American natural gas prices soared, hitting a high of $9.85 in August 2022, their highest level in 13 years.

Prior to the invasion, in early 2021, natural gas prices in the United States were about $2.50 per million cubic feet.

In 2022, increasing demand from Europe caused prices to soar and natural gas suppliers were willing to sell all they could.

Fast-forward to today, and we see that all the additional natural gas that came onto the market has caused prices to subside back to about $2.30 currently.

As a result, interest in natural gas suppliers (and their bond offerings) has subsided.

That’s great news for us!

This makes the Southwestern Energy (CUSIP 845467al3) January 23, 2025, 5.7% coupon bonds an excellent “Buy” right now.

Here’s why…

LNG prices have essentially dropped back to more “normal” levels – much closer to their long-term average. That’s a problem for many natural gas providers… but not Southwestern Energy.

Southwestern can still make a nice profit at current natural gas prices!

In the first quarter of 2023, Southwestern generated $1.9 billion in net income and reported first quarter earnings of $0.31 per share. Net cash provided by operating activities was $1.1 billion!

During the quarter – using mostly cash on hand – the company fully redeemed its outstanding 7.75% senior notes due in 2027.

The company is currently rated one notch below investment grade by all three credit agencies.

A Market Ready for Improvement

Because of the “selling spree” in 2022, natural gas inventory levels have shrunk. The amount of natural gas in storage is currently sitting 35% below where it was at the tail end of 2022.

Storage level is the main data point that traders watch.

The spring season is traditionally weak for natural gas pricing, as demand falls off after winter heating demand ends and before summer air conditioning demand picks up.

If we get a hot summer, which will further draw down inventory levels, natural gas prices could go much higher before next winter starts.

These low inventory levels are bullish for natural gas prices in the short term. And with this bond maturing in 2025, the short term is all we have to be concerned with.

Southwestern Energy was founded in 1929. This company has survived and thrived through nearly 100 years of ups and downs in the industry. The current management team has decades of experience.

I think the odds are pretty good that Southwestern will make it through the next several years.

Action to Take: Buy the Southwestern Energy (CUSIP 845467al3) January 23, 2025, 5.7% coupon bond. It is rated BB+ by S&P Global Ratings.

At the current trading price of $100, you will lock in a MEAR of 5.7%. You will receive four interest payments of $28.50, minus $21.38 in accrued interest, breaking even at maturity because we’re buying it at face value, for a holding period of 19.5 months at a cost of $1,000 per bond.

4 x 28.50 – 21.38 / 19.5 / 1,000 x 12 = 5.7%

(For the sake of simplicity, the equation above is calculated from left to right rather than using standard order of operations.)

Lending Its Way to Prosperity

Based in New York City, Prospect Capital is a business development company (BDC) that focuses on investing in small and medium-sized private companies.

BDCs are publicly traded investment companies that provide debt and equity capital to privately owned enterprises.

Some BDCs specialize in and focus on certain sectors, such as biotech, technology and retail. Prospect Capital is a generalist, entertaining opportunities wherever they lie, but the company’s particular expertise is in the energy and industrial sectors.

Prospect’s typical client is what’s called a middle-market business… businesses that are too big to borrow money from traditional banks but too small to tap into the public markets and issue bonds.

Prospect’s goal is to increase its capital, minimize risk and avoid chasing yield with investments deemed too risky or with poor risk-return profiles.

Prospect’s stringent risk-averse policies are one of the many things I like about the Prospect Capital (CUSIP 74348tat9) March 1, 2025, 6.375% coupon bonds.

Founded in 2004, Prospect Capital is the largest multiline BDC with $8.6 billion in capital. Prospect has one of the largest teams – more than 100 analysts – in the industry, which allows the company to target larger, more credit-worthy middle-market companies.

Because of the company’s intensive screening process, Prospect lends to less than 2% of the loan applications it reviews. The majority of the company’s loans focus on senior and secured lending.

Prospect has a diverse portfolio of 127 investments across 37 industries with 81% of the portfolio collateralized with first lien, secured or underlying assets.

For a lender, first lien means first priority. If a loan turns sour and the borrower declares bankruptcy, the first lien lender gets paid back first from the liquidation of the underlying collateral.

A first lien lender with ample collateral is taking very little risk. It’s hard to lose money if you have assessed the value of the underlying collateral reasonably well.

That’s why Prospect has the least risky loan portfolio of anyone in the sector.

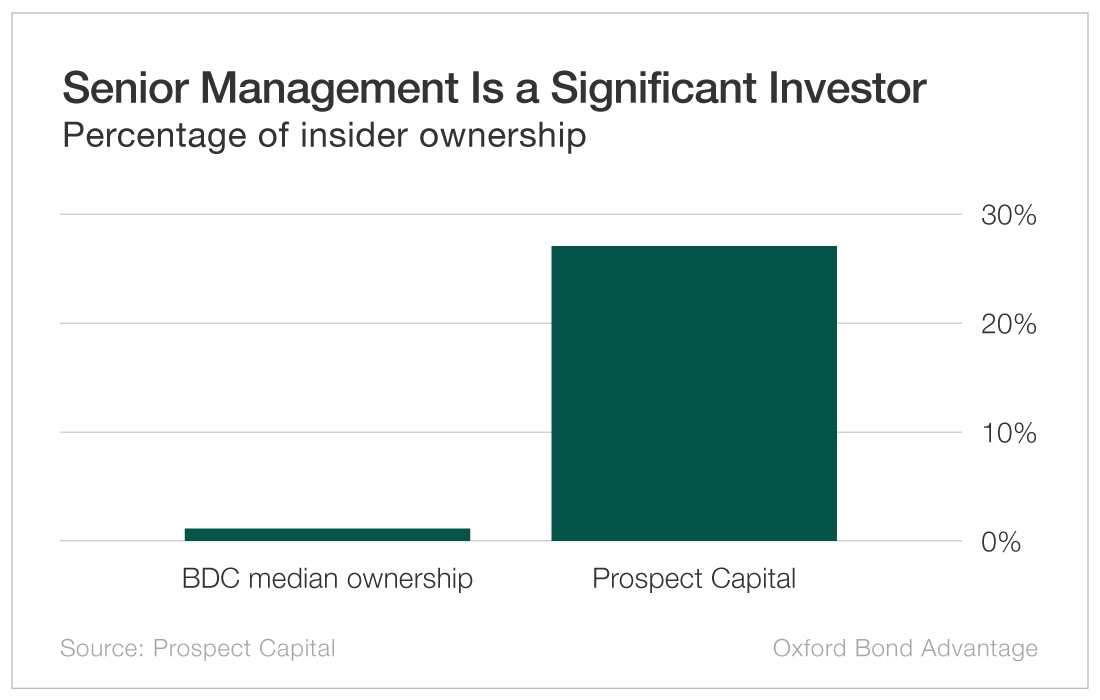

Management is experienced with more than 30 years of industry expertise. The management team has shown its commitment to and faith in the company with significant stock purchases.

Mr. Reliable

What drives performance for bonds is reliability. The best bonds to own are those tied to businesses that crank out a steady stream of cash flow year after year.

That’s why, as a bond investor, I love Prospect Capital. They don’t come any steadier than this. By every measure, these Prospect bonds have delivered for us since I recommended them in April 2019.

Relative to its BDC peer group, Prospect’s management team has built an extremely low-risk loan portfolio. Prospect’s standards are so stringent that nonaccrual (no longer being paid) loans are an incredibly low 0.2%.

Those first lien and secured positions are the protection the company has in a worst-case scenario, like if the economy turned south and borrowers started to struggle. Thankfully, it is a protection that the company will likely never need.

Currently, Prospect’s loans are performing extraordinarily well. I highly doubt this company will have any financial difficulty before our bonds mature in March 2025.

As I mentioned earlier, Prospect’s loan portfolio has only two-tenths of 1% deemed nonaccrual.

That’s near-perfect performance for Prospect’s loan portfolio…

Pretty incredible given the rise in interest rates we’ve seen. There has been no deterioration in Prospect’s loan performance in the past year.

When I recommended these bonds, I did so because I knew that this management team is one of the best in the industry.

I also recommended these bonds because I know that Prospect’s loan portfolio is built specifically around lending money to noncyclical businesses. Noncyclical investments represent 78% of the portfolio.

This means it avoids lending to businesses in industries like mining, automotive, hotels and construction.

Even in a recession, the noncyclicality of Prospect’s borrowers will allow this loan portfolio to hold up well.

This is a solidly profitable firm with an investment-grade credit rating from Standard & Poor’s.

Action to Take: Buy the Prospect Capital (CUSIP 74348tat9) March 1, 2025, 6.375% coupon bond. The bond is rated BBB- by S&P Global Ratings.

At the current trading price of $99, you will lock in a MEAR of 8.9%. You will receive five interest payments of $31.875, minus $15.94 in accrued interest, plus a $10 gain from buying at a slight discount to face value, for a holding period of 21 months at a cost of $990 per bond.

5 x 31.875 – 15.94 + 10 / 21 / 990 x 12 = 8.9%

(For the sake of simplicity, the equation above is calculated from left to right rather than using standard order of operations.)

These three bonds are great options to add to your bond portfolio. Again, any of the bonds rated “Buy” can be bought, but these three are conservative and offer great MEARs.

Congratulations on being a bond investor during the best time to be one in years.

Double Down on These Recs With an Upgrade!

I just narrowed down all of our bond recommendations to the three that I believe have a TON of upside right now…

I expect we’ll see MANY more huge opportunities – available at MASSIVE discounts – in the weeks and months ahead…

And I don’t want you to miss a single one.

More importantly, I want to make sure I’m here to help you maximize your profit potential on every opportunity in our portfolio right now!

So I’m giving you the chance to upgrade your Oxford Bond Advantage subscription for one of the lowest prices we’ve ever offered.

We’re talking about locking in guaranteed, lifetime access to my best research and top bond recommendations… for THOUSANDS less than you’d normally pay!

Simply click HERE to upgrade your subscription today.