The Next Great Space Company: A Microcap Poised for Astronomical Growth

A digital illustration of satellites orbiting Earth, connected by glowing lines, showcasing a network in space.

Apple may be on the verge of its most disruptive launch since the original iPhone.

It’s the foundation for a new era of connectivity – one that could seriously disrupt the $200 billion wireless carrier industry.

And it’s happening at a moment when the economics of space have fundamentally changed.

Thanks largely to SpaceX, satellite launches are now faster, cheaper, and more scalable than ever before. What was once the domain of governments and defense contractors is rapidly becoming a commercial platform – capable of supporting global consumer services at scale.

At the heart of Apple’s move into this new frontier is a company almost no one on Wall Street is paying attention to.

It’s a roughly $3 billion microcap stock… one that has already embedded its technology into more than a billion iPhones.

Apple has committed up to $1.5 billion to this partner, yet much of the market still hasn’t grasped the magnitude of what’s unfolding.

But history shows that when small suppliers become essential to Apple’s biggest product waves, quadruple-digit gains are not uncommon.

So what is this potential launch I’m predicting and, more importantly, who is the space partner Apple has chosen?

It starts with a feature that’s been quietly hiding in plain sight since 2022…

Apple’s Next Step Toward Mobile Domination

Apple debuted a new feature in its iPhone 14 called Emergency SOS via Satellite, allowing users to send emergency texts when outside cell or Wi-Fi coverage.

Not the most exciting upgrade.

But certainly a meaningful one.

Most iPhone owners will never trigger it. But for those in danger – or beyond the reach of terrestrial networks – it offers a potentially lifesaving connection.

What caught my attention was what happened next.

In 2024, Apple quietly committed up to $1.5 billion to expand its satellite footprint with its chosen “space partner” – Globalstar Inc. (Nasdaq: GSAT).

This move didn’t happen in a vacuum.

SpaceX had already demonstrated, through its Starlink network, that low-Earth-orbit satellites could deliver reliable, real-time connectivity at scale. Apple didn’t need to reinvent that wheel – it simply needed a dedicated, tightly integrated satellite backbone for the iPhone ecosystem.

Of Apple’s $1.5 billion commitment…

-

$1.1 billion is allocated for prepaid satellite services

-

$400 million gives Apple a 20% equity stake in Globalstar.

And Globalstar has committed 85% of its upgraded network capacity to Apple.

When the announcement hit, Globalstar shares jumped more than 30% in a single session.

That reaction made sense.

While Apple hasn’t yet revealed plans to challenge mobile carriers directly, this partnership puts it in prime position to do so. And in a world where SpaceX has already proven the viability of satellite-based connectivity, Apple’s optionality here is enormous.

When – not if – Apple expands its satellite capabilities, Globalstar could be sent straight into orbit.

The Hidden Satellite Backbone Powering iPhones

For years, Globalstar was written off as just another struggling satellite operator – long on vision, short on profitability.

That narrative is now broken.

The company’s latest results don’t just show improvement… they signal a financial inflection point.

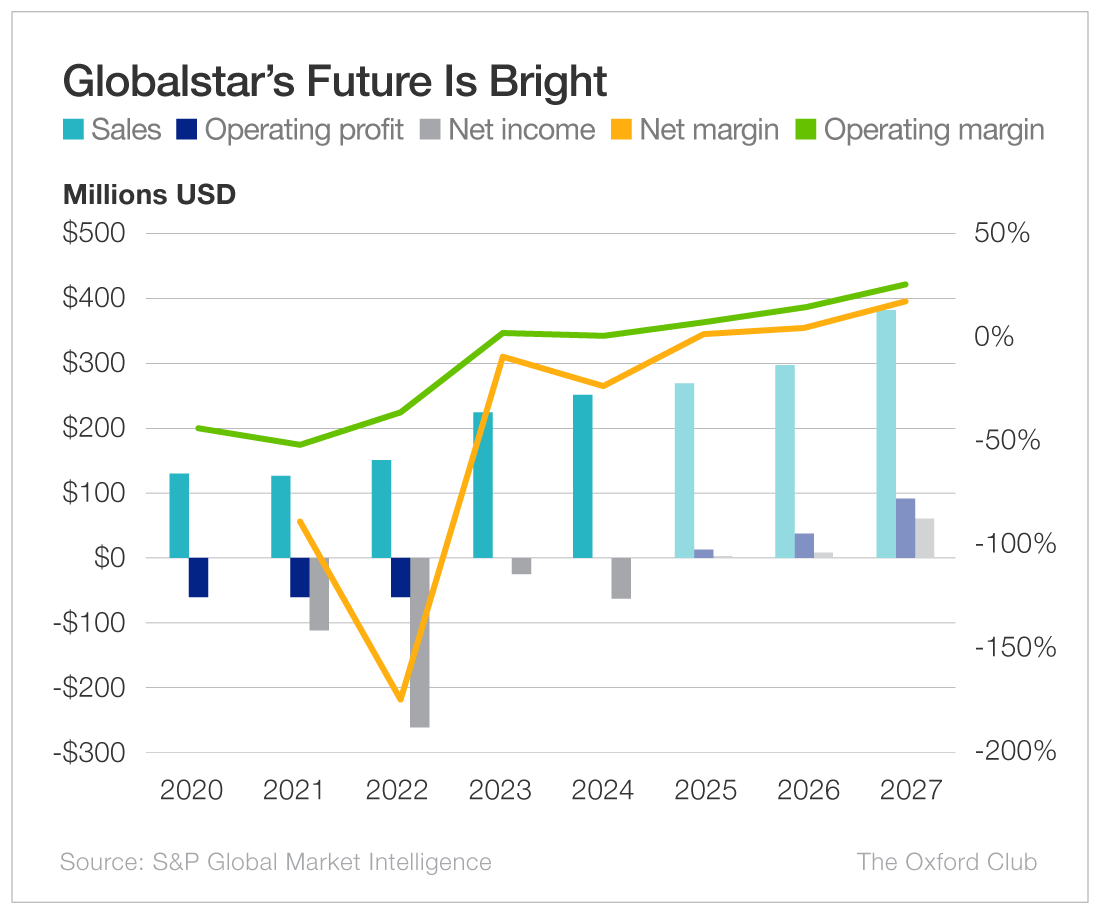

In the second quarter of 2025, revenue climbed 11% year over year to $67.1 million. But the headline number isn’t the full story…

Globalstar flipped from a net loss to a $19.2 million profit, delivering earnings per share of $0.13.

Adjusted EBITDA surged to $35.8 million, translating to a 53% margin – rivaling far larger players in the satellite communications space. Adjusted free cash flow for the first half of 2025 came in at $77.9 million, up sharply from $51.9 million a year earlier.

The company now holds $308 million in cash and controls $1.91 billion in total assets.

Just as important, Apple’s prepaid capital has removed much of the financing risk typically associated with satellite operators – a risk SpaceX itself spent years overcoming through scale and launch efficiency.

With Apple footing much of the expansion bill, Globalstar now has the stability to fully capitalize on growth initiatives. In the microcap world, that combination – profitability, free cash flow, and locked-in revenue – is exceptionally rare.

4 for 4: How Globalstar Meets Every Microcap Benchmark

When I recommend a microcap, I’m not looking for a flashy story. I’m looking for four traits that separate real opportunities from the penny-stock graveyard: sustained sales growth, rising earnings, undervaluation, and strong institutional commitment.

- Sustained Sales Growth

Globalstar isn’t a speculative concept. Its satellite technology already powers a core feature inside Apple’s iPhone lineup – a development made economically viable by the launch-cost revolution led by SpaceX.

Beyond Apple, the company serves commercial, government, and defense clients worldwide. Its new strategic agreement with the U.S. Army opens the door to the $40 billion defense communications market.

The result is multiple consecutive quarters of rising sales – the first and most important sign of a microcap on the verge of a breakout.

- Rising Earnings Power

Most microcaps burn cash. Globalstar is generating it.

The company has demonstrated it can cover operating costs, fund expansion, and reinvest in growth – without the constant shareholder dilution that plagues smaller companies.

- Deep Undervaluation

Despite Apple’s investment, its satellite constellation, and years of contracted revenue, Globalstar trades near a $3 billion market cap.

That figure dramatically understates its intrinsic value – especially in an industry where SpaceX has shown that scalable satellite networks can command enormous strategic premiums.

- Powerful Insider and Institutional Backing

Apple’s roughly 20% ownership stake is more than a vendor relationship. It’s strategic alignment between a $3 trillion technology leader and a small company positioned at the center of its next connectivity push.

That kind of backing is rare – and often a precursor to outsize returns.

Put it all together, and Globalstar isn’t just a “check the box” story – it’s a microcap that hits every one of the proven criteria for turning small companies into big winners. With its technology already in millions of devices, a defense market foothold, and an expansion plan fully funded, it’s in the sweet spot where microcaps make their biggest moves.

A Growth Launchpad for Apple’s Satellite Network

So what’s next for Apple’s quiet satellite partner?

In short… Liftoff.

Globalstar is undertaking the most significant expansion in its history. The centerpiece is a constellation refresh – 17 next-generation satellites, built by MDA Space Ltd., with options for nine more.

These satellites are scheduled to begin launching in Q4 2025, benefiting from an industry now optimized for rapid deployment – a standard largely set by SpaceX.

At the same time, Globalstar is expanding its global ground infrastructure, adding new gateway stations and upgrading existing ones to improve coverage, reduce latency, and increase throughput.

Management expects 2025 revenue to more than double once the new satellites and upgraded systems are fully online – a forecast supported by locked-in demand from Apple and growing interest from enterprise and government customers.

Globalstar isn’t just growing.

It’s scaling – with a fully funded network, a dominant anchor client, and a space economy that SpaceX has already proven can expand far faster than Wall Street expects.

Recommendation: Buy Globalstar (Nasdaq: GSAT) at market.