The Gold Stock Lag: How to Position Yourself for Gains of 1,000% or More as X Marks the Spot

Gold has been on one of the great bull runs in modern history. From under $1,800 an ounce a few years ago, it has surged past $3,000… $4,000… and even $5,000… finally touching above $5,600 before easing back. The gains have been absolutely extraordinary.

But if history is any guide − and having studied over 50 years’ worth of data, I strongly believe it is − the biggest gains from this gold bull market haven’t happened yet.

The reason comes down to a pattern I’ve been tracking for years. I call it the “Gold Stock Lag.” It’s a consistent, repeatable phenomenon, and it has played out during every major gold bull market since the 1970s.

Here’s how it works: When gold goes on a major run, a specific group of stocks called junior gold miners lag behind.

It’s not because anything is wrong with them, and it’s not because they’re missing the rally. It’s simply because Wall Street moves slowly.

Analysts wait for earnings confirmation, fund managers wait for analyst upgrades, and institutional investors wait for each other. Nobody wants to be first.

These stocks sit there, ready to take off, while the obvious gold plays grab all the headlines.

Then, once gold peaks and levels off − and once those first earnings reports arrive and show profit margins nobody has ever seen before − the dam breaks. The institutional money floods in all at once… and these junior miners don’t just catch up to gold. They overshoot it dramatically.

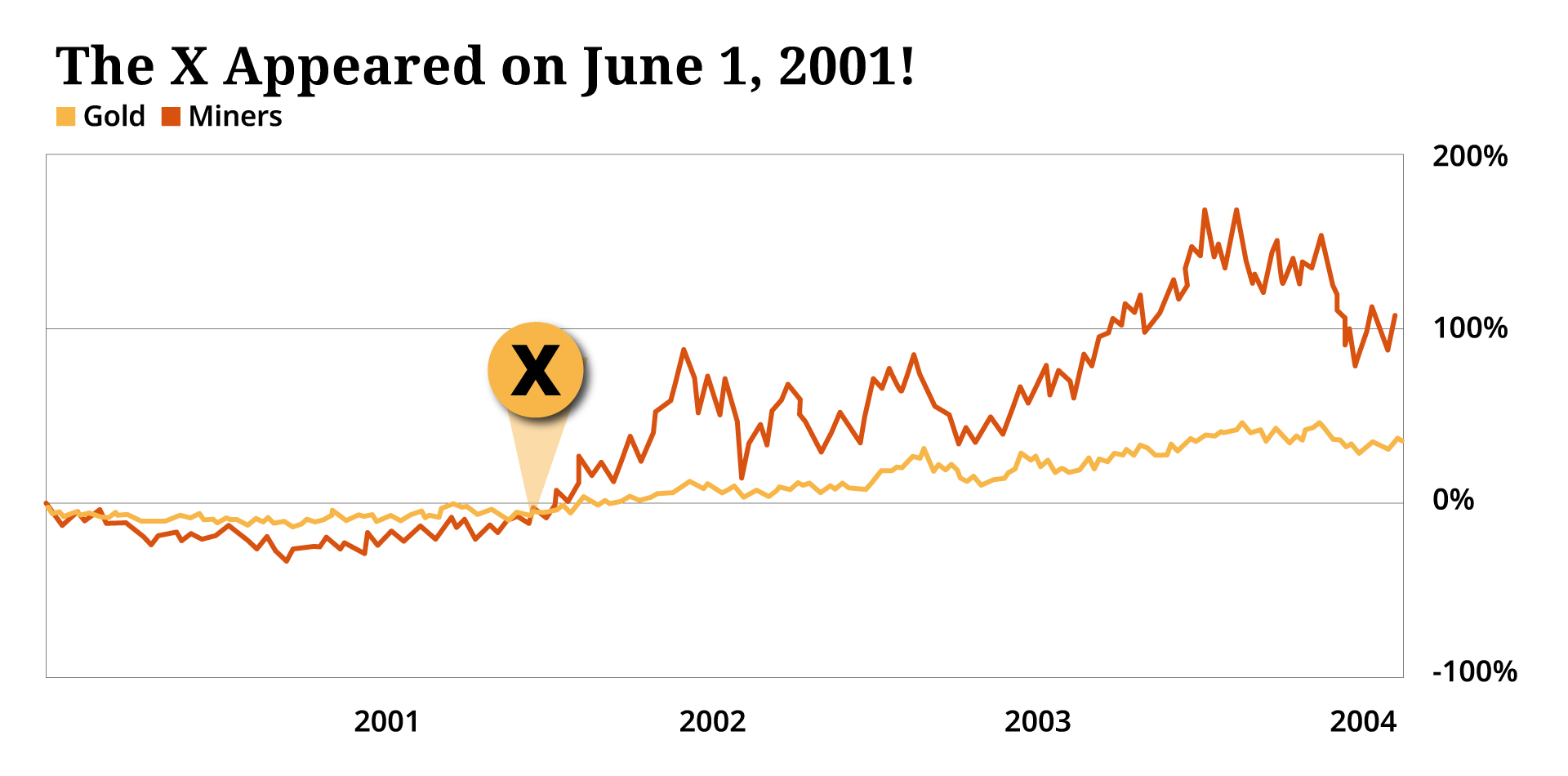

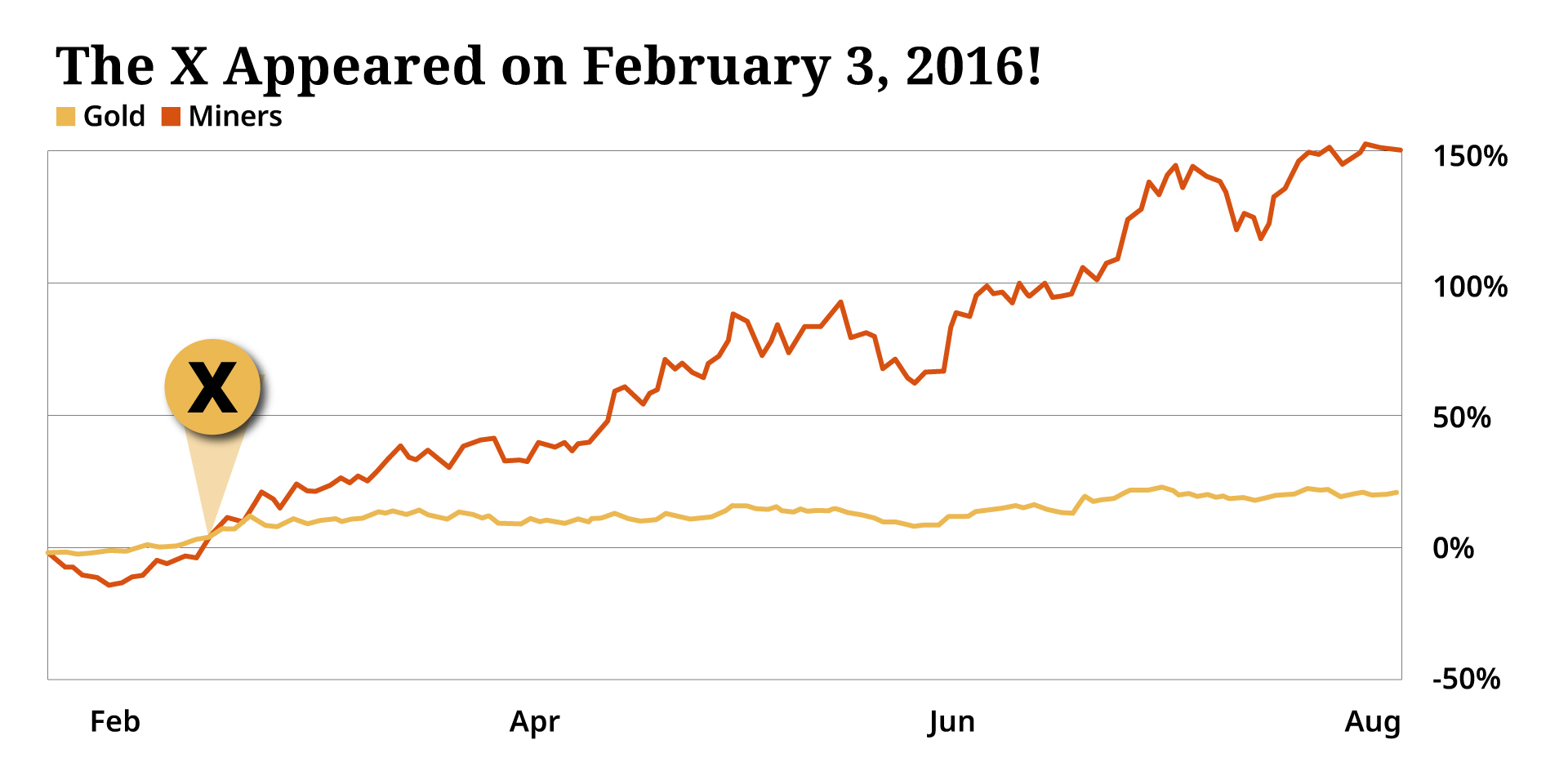

The effect is so dramatic, in fact, that it creates a clear “X” on the chart at the exact moment when these stocks accelerate past gold.

Here are a couple of examples of the crossover point…

As they say, “X” really does mark the spot.

The reason for the overshoot is simple math.

When gold rises from, say, $2,000 to $5,600, a junior miner with production costs of $1,400 per ounce sees its per-ounce profit explode from $600 to $4,200. That’s a 600% increase in profits from a 180% move in gold.

The math works in miners’ favor in a way it simply doesn’t for the metal itself.

This pattern has repeated through five decades, propelling individual stocks like Keegan Resources, B2Gold, Aurelian Resources, Seabridge Gold, and Cartaway Resources to gains of 1,012%… 1,640%… more than 5,000%… 11,375%… and even as much as 26,040%.

But right now, we are sitting at the most compelling version of this setup I have ever seen.

The current gap between gold prices and junior miner performance is arguably the widest it’s been at this point in the cycle in 50 years.

Gold is up roughly 129% from its base; junior miners are up just 83%. That’s an enormous 46-point gap − nearly twice as wide as in previous cycles.

Think of this effect like a slingshot. The farther you pull it back, the harder it launches… and right now, the slingshot is pulled back farther than at any point in half a century.

Crucially, there’s one more catalyst that makes the timing especially urgent: Within the next few weeks, these junior miners will release their first-ever earnings reports with gold above $5,000.

That will be the confirmation Wall Street has been waiting for.

When analysts see those profit numbers − figures unlike anything they’ve seen before − the explosion will begin.

In this report, I’ve identified five junior gold miners that I believe are perfectly positioned to ride this wave.

Each one is trading at a significant discount, and each one has the balance sheet, the production profile, and the catalysts to potentially deliver 1,000% gains or more in the coming years.

The window is open right now. Let me show you how to play it.

Gold Stock Lag Pick #1: Americas Gold and Silver (NYSE: USAS)

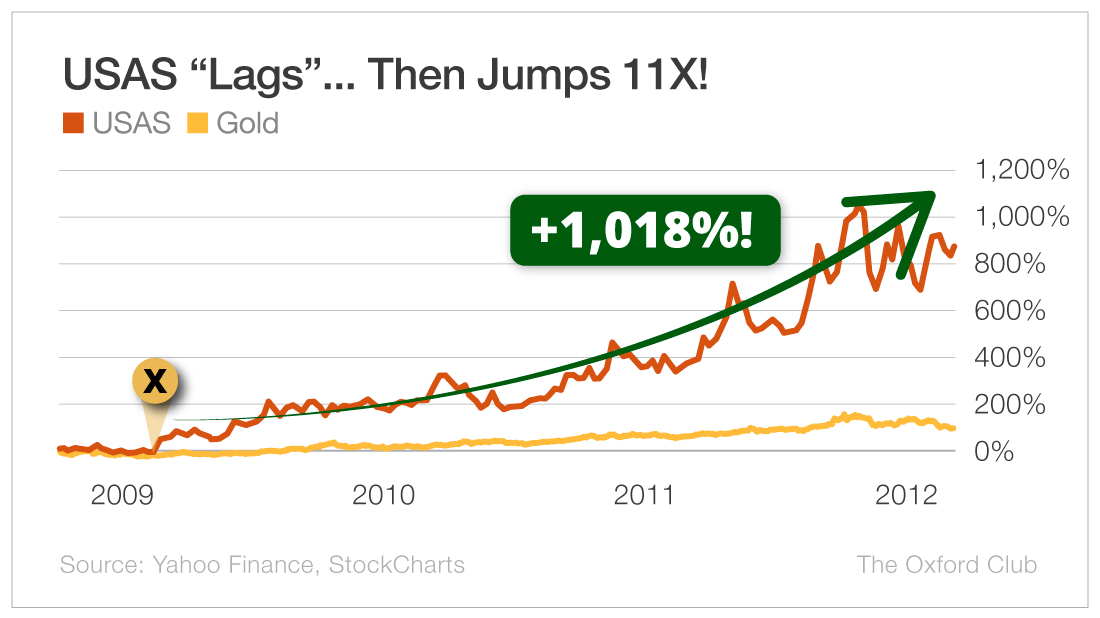

Americas Gold and Silver is my top pick for this cycle for a reason: It has already seen substantial gains from the Gold Stock Lag pattern once before.

In 2009, the stock followed the Gold Stock Lag almost perfectly.

It lagged behind the metal during gold’s rise… and then launched after the crossover point (the “X”), delivering gains of more than 1,000% over the following two years.

That pattern is now setting up again, and the conditions today are arguably more favorable than they were in 2009.

The gap between gold prices and junior miners’ performance is wider today than it was at the equivalent stage of the 2009 cycle. If Americas Gold and Silver follows the same playbook − and the math strongly suggests it will − the gains from here could rival (or even exceed) what we saw in 2009.

The Price (and the Timing) Is Right

Timing matters with the Gold Stock Lag, and right now, the clock is ticking on a specific catalyst: earnings.

The company is scheduled to issue its next earnings release during the second or third week in May. This will be the first time it reports its financials with gold trading above $5,000 an ounce. That’s not a minor detail.

At current gold prices, its per-ounce profit margins are dramatically wider than anything the company − or Wall Street − has seen before. When those numbers hit, the repricing should begin immediately. Institutions that have been waiting for “confirmation” won’t have any excuse left to sit on the sidelines.

The window to get in ahead of that moment is closing fast.

With a share price of approximately $6 and a market cap of $1.5 billion, the stock sits in a sweet spot that’s rare to find in mining. It’s large enough to have proven operations, audited financials, and real institutional coverage, but small enough to have potential that a $50 stock simply can’t match.

For a household name like Meta Platforms (Nasdaq: META) or Tesla (Nasdaq: TSLA) to return 10X from here, it would have to grow to a market cap of around $15 trillion, or roughly half of U.S. GDP. That’s not happening − at least not anytime soon.

But a small cap stock like this one can catch the full force of a Gold Stock Lag breakout, rocket up by 10X, and still have plenty of room to run.

One of the most telling signs that this stock is coiled and ready to pop is its recent price action − or lack thereof. Since mid-March, Americas Gold and Silver has been consolidating, mostly trading in a tight range around $6 without breaking out in either direction.

When volatility tightens like this, prices stay cheap. It’s the ideal entry condition, because you’re getting in at a discount to where the stock should be trading, and you’re positioned to catch the full force of the move when the spring finally releases.

Every stock in this report represents a compelling opportunity, but Americas Gold and Silver earns the top spot because it has done this before − under conditions nearly identical to today’s.

When you combine the imminent earnings catalyst, the compressed entry price, and one of the widest gold-to-miners gaps in 50 years… you have a setup I wouldn’t want to miss.

Recommendation: Buy Americas Gold and Silver (NYSE: USAS) at the market. Set a 25% trailing stop to protect your principal and profits.

Gold Stock Lag Pick #2: Galiano Gold (NYSE: GAU)

If Americas Gold and Silver is my pick based on proven history, Galiano Gold is my pick based on a setup that looks almost absurdly mispriced.

This is a company that’s producing real gold, generating real cash, and carrying zero debt. Yet it’s trading at less than half the valuation of a typical gold miner.

The disconnect between what the business is actually doing and what the market is paying for it is one of the most striking I’ve encountered in this sector.

A Producing Mine With Growing Output

Galiano controls 90% of the Asanko Gold Mine in Ghana, which is actively ramping toward 200,000 ounces per year.

This isn’t an exploration company hoping to find something in the ground. The gold is already being mined, processed, and sold.

That distinction matters enormously at this stage of the Gold Stock Lag cycle. When Wall Street starts paying attention to junior miners − and the incoming earnings reports will force that attention − companies with real, auditable production will spike first and fastest.

Galiano is exactly that kind of company.

It carries over $100 million in cash and zero debt. In the gold mining sector, that combination is genuinely rare. Most junior miners have taken on significant leverage to fund their operations, which means a portion of every dollar of upside from higher gold prices gets absorbed by interest payments and paying off debt.

That’s not the case with Galiano.

With no debt weighing it down, every time the price of gold moves up, the extra cash flows directly to the bottom line. At current gold prices, that bottom line looks dramatically different than it did even 18 months ago.

Priced Like Gold Is at $1,800

This is the heart of the opportunity: By standard valuation metrics − price-to-earnings, enterprise value-to-production, price-to-cash flow, and others − Galiano trades at less than half what a typical gold miner of its profile commands.

That discount doesn’t reflect any fundamental problem with the business. The mine is operating, production is growing, and the balance sheet is clean.

The discount exists because the market is still using outdated assumptions about gold prices. It’s pricing Galiano as if gold has barely moved from its 2022 lows.

Once the market catches up to that reality, the stock’s rise could be swift and dramatic.

The Gold Stock Lag has historically produced its biggest percentage gains in stocks where the disconnect between price and value is most extreme. Galiano fits that profile precisely. The mine is producing. The cash is in the bank. The price of gold has moved. But the stock hasn’t − yet.

That’s not a reason to stay away. That’s the opportunity.

Recommendation: Buy Galiano Gold (NYSE: GAU) at the market. Set a 25% trailing stop to protect your principal and profits.

Gold Stock Lag Pick #3: Fortuna Mining (NYSE: FSM)

Fortuna Mining is perhaps the most mature company on this list.

It operates three mines in Côte d’Ivoire, Argentina, and Peru, producing more than 300,000 gold-equivalent ounces annually.

That geographic and operational diversification provides a kind of resilience that single-mine operators simply don’t have. If one region faces regulatory delays or operational hiccups, the others keep delivering.

That diversification also means Fortuna has multiple pathways to growth. The company isn’t dependent on a single deposit or a single jurisdiction for its future production expansion.

The numbers here are hard to ignore. Fortuna holds approximately $400 million in cash and total liquidity of close to $700 million. In an industry where balance sheet stress is common, that’s exceptional.

That financial firepower gives Fortuna something most of its peers can’t claim: the ability to fund its own expansion without diluting shareholders or taking on debt.

When a junior miner needs capital to grow and turns to equity markets to issue new shares, existing shareholders pay for it through dilution. Fortuna doesn’t face that constraint.

An Ambitious and Well-Funded Growth Plan

I mentioned before that Fortuna is already producing 300,000 ounces a year. However, it’s targeting 500,000 ounces of annual production, or a 65% uptick from today’s output. Critically, that expansion can be funded from existing cash and cash flow without the need for external financing.

The combination of current scale, balance sheet strength, and a well-funded path to much higher production is exactly what institutional investors look for when they start deploying capital into a sector.

Right now, they’re getting all of that from Fortuna − and at a meaningful discount.

Fortuna’s stock has not kept pace with the movement in gold prices, despite the fact that the company’s profitability has improved dramatically. With gold above $5,000 and production costs largely fixed, the margin expansion over the past year has been extraordinary… but the stock price still reflects a much more modest gold environment. That gap tends to close abruptly.

The catalysts are aligning: an incoming earnings report that will showcase historic margins, a funded expansion plan, and institutional investors who will soon have no choice but to acknowledge what the underlying business is actually generating.

Recommendation: Buy Fortuna Mining (NYSE: FSM) at the market. Set a 25% trailing stop to protect your principal and profits.

Gold Stock Lag Pick #4: McEwen (NYSE: MUX)

Every stock on this list benefits from the Gold Stock Lag, but as you’ll see, there’s even more to the story with McEwen.

The company currently produces approximately 60,000 gold-equivalent ounces per year. That’s respectable for a junior miner.

Management has laid out a detailed plan to reach 250,000 to 300,000 gold-equivalent ounces annually by 2030. That would represent roughly a fivefold increase in production over the next four years.

At current gold prices, production growth of that magnitude implies a level of earnings growth that most sectors simply cannot match. When junior miner production quadruples or quintuples, the profit math I described in the introduction becomes truly explosive.

But that’s not what sets McEwen apart from the rest of the companies in this report.

The Copper Giant Nobody Is Talking About

Buried in the company’s asset portfolio is a 46% stake in Argentina’s Los Azules, one of the largest undeveloped copper projects in the world. The independent valuation of Los Azules is north of $2.9 billion.

McEwen’s total market capitalization is a fraction of that figure. The market is pricing the company as a small gold miner and essentially ignoring the copper stake entirely − even as increased copper demand driven by electrification, data centers, and infrastructure spending makes large copper deposits increasingly valuable.

Investors who buy McEwen today are effectively getting the gold production story at a discount… and the potential upside from the copper stockpile for free.

That kind of setup − where a significant asset is simply not being priced in − tends to resolve sharply when attention finally arrives.

The Gold Stock Lag alone is a reason to own McEwen. The pattern fits: meaningful production, an undervalued stock, and the imminent release of the first earnings report with gold above $5,000.

But the copper asset adds a second independent catalyst.

As the major gold miners go shopping for junior acquisition targets to replenish their declining reserves, McEwen’s combination of gold production and a massive copper project makes it an unusually attractive package. Buyout speculation alone could move this stock substantially.

The market is pricing McEwen like a small, unremarkable gold miner. The assets tell a very different story.

Recommendation: Buy McEwen (NYSE: MUX) at the market. Set a 25% trailing stop to protect your principal and profits.

Gold Stock Lag Pick #5: TRX Gold (NYSE: TRX)

TRX Gold is the most speculative pick in this report. It’s a single-mine operator at an earlier stage of its development than the other four companies listed.

That said, the upside case is as compelling as anything I’ve seen in junior gold mining, which is why it earns a place on this list.

You see, one of the things that sets TRX apart from more speculative junior miners is that it is already profitable.

The company’s single operating mine, the Buckreef Gold Project in Tanzania, posted 61% profit margins, record revenue, and record production in the second quarter of fiscal 2026, which ended in February.

Current production sits between 25,000 and 30,000 ounces of gold per year. That’s a solid base for a company of this size… but the real story is where that number is going.

TRX is in the middle of a major mine expansion, with an initial target of 62,000 ounces annually and the potential for significantly higher production beyond that. At current gold prices, doubling production from an already 61%-margin operation produces a level of earnings growth that is hard to find anywhere in the market.

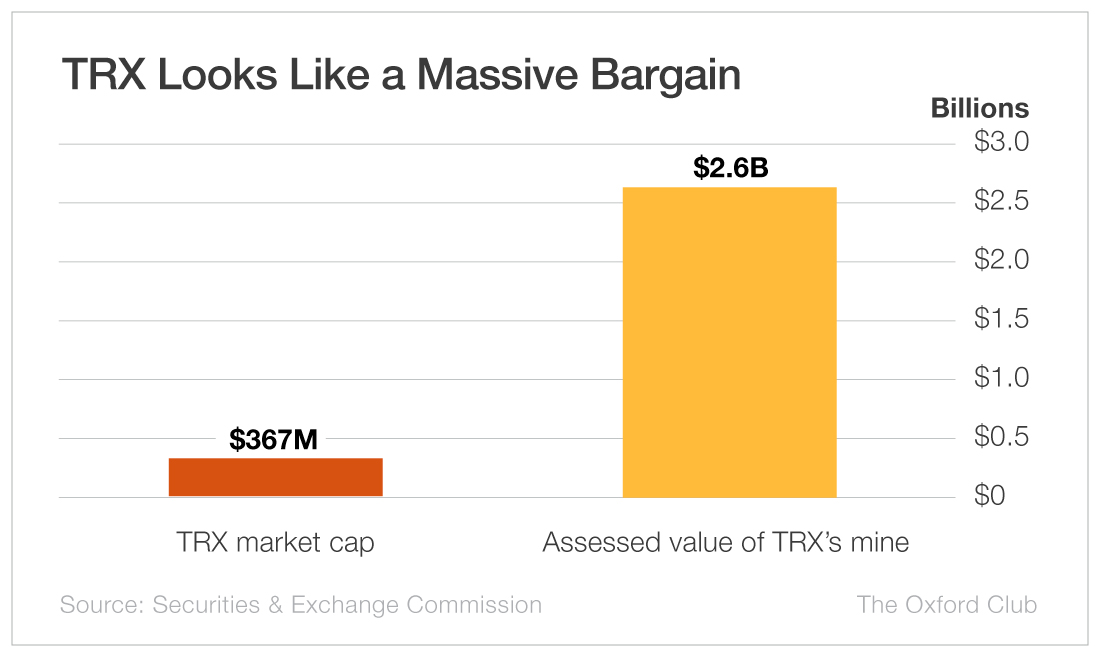

An independent engineering study has valued TRX’s total potential operation at up to $2.6 billion at current gold prices.

The company’s current market capitalization is approximately $367 million.

That’s less than 15% of the independently assessed value of the assets. Even when we account for the execution risk of a mine expansion − and that risk is real − the gap between market price and appraised value is extraordinary. You don’t encounter disconnects of this magnitude very often in any sector.

Why the Upside Could Be Exceptional

The Gold Stock Lag creates a rising tide that lifts all the junior miners on this list. But for a company like TRX with rapid production growth and hugely undervalued assets, the potential upside is staggering.

The expansion is ongoing, the margins are exceptional, and the assets are proven. Yet the market is barely paying attention.

A small position in TRX is, in my view, worth the additional risk. If the expansion unfolds as planned and the Gold Stock Lag triggers as I expect, this could be the biggest winner in the group.

Given the company’s size, I recommend sizing any position in TRX accordingly. Investors who are wary of the elevated volatility might consider a smaller allocation.

Recommendation: Buy TRX Gold (NYSE: TRX) at the market. Set a 25% trailing stop to protect your principal and profits.

Remember, while I expect these stocks to be big winners, junior gold miners are speculative and can be volatile. Position size accordingly for all five, and don’t invest more than you can afford to lose.

The Window Is Open Now

Fifty years’ worth of market history is telling us the same thing it has told investors in every major gold bull market since the Nixon era: The biggest gains don’t come from gold itself. They come from the select group of junior miners that lag behind during gold’s rise… and then explode after the crossover.

The current setup is the most compelling version of this pattern I have ever seen.

The gap between gold prices and junior miner performance is among the widest in half a century. The catalyst − earnings reports showing unprecedented profit margins − is arriving within weeks, and the underlying math translates into gains that most investors aren’t yet pricing in.

The Gold Stock Lag has played out across five decades − through different presidents, different crises, and different economic environments. The pattern has never failed to produce extraordinary winners for those who were positioned ahead of the crossover.

With the all-important earnings reports just weeks and even days away, that crossover is approaching. The time to act is now… before “X” marks the spot.