The Big Beautiful Nation

The 4 Companies Powering the Resurgence of American Defense

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act into law. At 870 pages, it is the largest piece of domestic legislation enacted in a generation.

Most investors read the headlines about trillions of dollars in tax cuts and moved on.

I kept reading.

On Page 290, buried in Section 20002 of Title II, I found something that changes the investment case for American defense: a $29 billion government mandate to build the most powerful naval fleet of all time.

The Trump administration calls it the “Golden Fleet.”

The bill allocates $4.6 billion for a new nuclear-powered attack submarine, $5.4 billion for guided-missile destroyers, $2.1 billion for unmanned surface vessels, and billions more to rebuild America’s broader maritime industrial base.

According to law firm K&L Gates, this initiative will “set in motion the largest revitalization of U.S. shipbuilding since before WWII.”

In 1940, the year before the United States entered the war, America produced 90% of the world’s ships, making it the dominant maritime power on Earth. Yet today, our shipbuilding capacity is estimated to be just 0.5% that of China’s.

The One Big Beautiful Bill just changed that equation, and only a small group of companies have the expertise, the infrastructure, and the existing contracts to answer the call.

In this report, I’m recommending four of them – the companies I believe are best positioned to profit from America’s biggest defense expansion since World War II.

Pick No. 1: Huntington Ingalls Industries (NYSE: HII)

If you want to understand why America’s shipbuilding revival starts here, consider this: Huntington Ingalls Industries is one of only two companies in the U.S. that can build nuclear-powered submarines and the only one capable of designing and building nuclear-powered aircraft carriers.

It essentially has a monopoly. After decades of investment, specialized labor, and classified engineering know-how, its position can’t be replicated quickly or cheaply.

The U.S. Navy currently operates 49 nuclear-powered attack submarines. Its stated goal is 66. Every additional boat the Navy needs has to come from Huntington Ingalls or its single partner in production.

With the Golden Fleet mandate now federal law, the demand pipeline has never been clearer.

CEO Chris Kastner said it all on one of the company’s recent earnings calls: “The U.S. Navy and all of our defense customers need our ships and technologies now more than ever.”

A Business Built for This Moment

In 2025, Huntington Ingalls reported revenue of $12.5 billion, up 8.2% year over year. All three of its divisions – Newport News Shipbuilding, Ingalls Shipbuilding, and Mission Technologies – reached record revenue levels during the year. That kind of broad-based strength is unusual in any industry, but it’s especially notable in defense contracting, where program delays and cost overruns are common.

Newport News Shipbuilding, the division responsible for manufacturing nuclear vessels, grew revenue 9% to $6.5 billion. Shipbuilding throughput increased 14% in 2025, and management has targeted another 15% improvement in 2026.

In 2025, the company delivered one Virginia-class submarine to the Navy, launched another, and began construction of a third. It also delivered the bow section of the first Columbia-class ballistic missile submarine – a critical milestone. According to the Library of Congress, “Since 2013, the Navy has consistently identified the Columbia-class program as the Navy’s top priority program.”

Huntington Ingalls finished 2025 with $53.1 billion in backlog after booking $16.9 billion in new contract awards during the year. That backlog represents roughly four years of revenue, and it was built before the full financial weight of the One Big Beautiful Bill began to flow through the system.

Free cash flow reached $800 million in 2025. Earnings per share grew 10.2% to $15.39. Combined operating income across all three segments rose 25.1% to $717 million, with operating margins expanding from 5.0% to 5.7%.

More recently, first quarter revenue grew more than 13% year over year to $3.1 billion.

Over the past 15 years, Huntington Ingalls has delivered average annual gains of approximately 17%.

Those returns were generated during a period when defense budgets were flat or declining. American shipbuilding policy was, at best, indifferent.

That era is over.

The policy environment has reversed, the funding is now federally mandated, and the biggest order in Huntington Ingalls’ history has not been placed yet.

When the Navy moves to close the gap between its current fleet of submarines and its goal of 66, the scale of that procurement will dwarf anything Huntington Ingalls has ever seen.

Recommendation: Buy Huntington Ingalls Industries (NYSE: HII) at the market. Set a 25% trailing stop to protect your principal and profits.

Pick No. 2: BWX Technologies (NYSE: BWXT)

Every Virginia-class submarine, every aircraft carrier, and every Columbia-class ballistic missile submarine in the U.S. Navy requires a nuclear reactor. And every one of those reactors is manufactured by a single company: BWX Technologies.

BWX doesn’t have to compete for naval nuclear contracts. It is the only entity licensed to produce them.

That distinction gives it an unparalleled position in the U.S. defense industrial base: a sole-source monopoly over the single most critical component of the Navy’s most capable vessels.

Over its six-decade history, the company has delivered more than 420 reactor cores to the Navy and built 325 steam generators for nuclear power plants. It is the Pentagon’s most trusted nuclear contractor – and now, with the Golden Fleet mandate driving submarine production toward historic levels, it is also one of the most indispensable.

A Record Year… and a Backlog That Keeps Growing

In 2025, BWX Technologies delivered the strongest financial results in its history. Full-year revenue grew 18% to $3.2 billion, and adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) increased 15% to $574 million. Earnings per share jumped 20%, and free cash flow rose 16%.

All of those metrics exceeded the company’s own initial guidance.

BWX ended 2025 with $7.3 billion in total backlog, up 50% year over year. By the end of the first quarter of 2026, that number had expanded to over $8.6 billion.

The growth has been driven by large, multiyear naval propulsion contracts, special materials processing, and commercial nuclear power awards. Q1 revenue and earnings per share rose 26% and 22%, respectively.

The company secured approximately $2.6 billion in contracts under the U.S. Naval Nuclear Propulsion Program in mid-2025 and has already added over $1 billion of it to the backlog.

These are long-duration, recurring revenue streams that reflect the Navy’s absolute dependence on BWX Technologies for its nuclear propulsion needs.

For 2026, the company expects to report non-GAAP earnings per share of $4.60 to $4.75 and adjusted EBITDA of $650 million to $665 million, representing double-digit growth over 2025’s record results.

Beyond the Navy

BWX Technologies is not solely a defense company. It has built a growing commercial nuclear business that provides diversification and additional growth runway.

In 2025, the company closed the acquisition of Kinectrics, expanding its nuclear power plant services and radiopharmaceutical isotope business.

Then, in May 2026, BWX announced the acquisition of Precision Components Group, establishing a domestic footprint in commercial nuclear component manufacturing and further broadening its business beyond defense.

The company is also advancing the BWXT Advanced Nuclear Reactor, or BANR – a truck-portable small modular reactor capable of generating 50 megawatts of power virtually anywhere. The military applications for BANR are obvious, but so are the data center applications: As AI companies race to secure reliable, low-carbon power for their facilities, a deployable reactor that can be set up in weeks rather than years becomes an extraordinary asset.

Over the past 10 years, BWX Technologies has delivered average annual total returns of approximately 20%. In 2025 alone, the stock gained 56% – not because of a product launch or one viral moment, but because the U.S. Navy needs nuclear reactors and there is only one place to get them.

With terrific growth across the board, an $8.6 billion backlog, and a federally mandated naval expansion that requires the company’s products, the setup for BWX Technologies is as clean as it gets.

Recommendation: Buy BWX Technologies (NYSE: BWXT) at the market. Set a 25% trailing stop to protect your principal and profits.

Pick No. 3: RTX (NYSE: RTX)

RTX – formerly known as Raytheon Technologies – is the largest defense and aerospace company in the world by revenue. With $88.6 billion in sales in 2025, it operates at a scale that few can match.

That being said, the investment case here is not just about size. It’s about the specific, high-urgency contracts that are flowing through the company’s defense businesses at an accelerating pace.

RTX’s defense backlog reached $109 billion in the first quarter, with its total backlog shooting up to $271 billion – a 25% increase year over year. That kind of growth reflects an environment in which demand is accelerating faster than any contractor can immediately supply, and RTX is at the front of the line.

Two Contracts Worth Watching

In early January 2026, Collins Aerospace, an RTX business unit with more than 70 years of experience as a supplier to the Federal Aviation Administration, was awarded a $438 million contract to support the FAA’s Radar System Replacement program. The program is part of the Department of Transportation’s initiative to modernize the U.S. National Airspace System, with plans to replace up to 612 aging radar systems nationwide by 2028.

Collins will deliver next-generation radar systems that are slated to replace a patchwork of aging technology with a unified, modern platform. As the work scales toward the full 612-system replacement program, RTX is positioned to capture a significant share of what amounts to a nationwide infrastructure overhaul.

At the same time, Raytheon – RTX’s defense systems division – is advancing the U.S. Army Lower Tier Air and Missile Defense Sensor, known as GhostEye. This is the next-generation missile defense radar that will replace the current radar in the Army’s Patriot system.

In August 2025, the Army awarded Raytheon an additional $1.7 billion under the program, bringing the cumulative contract value to $3.8 billion. The Army plans to acquire 94 of these systems over the next several years, so the existing agreements cover only a fraction of the potential revenue for RTX.

In December 2025, RTX also secured a $50 billion umbrella contract from the Department of Defense to supply Patriot missile defense systems, spare parts, services, and sustainment over a 20-year period for U.S. and international customers. That single award is larger than most defense companies’ entire enterprise value.

A Banner Year With More Room to Run

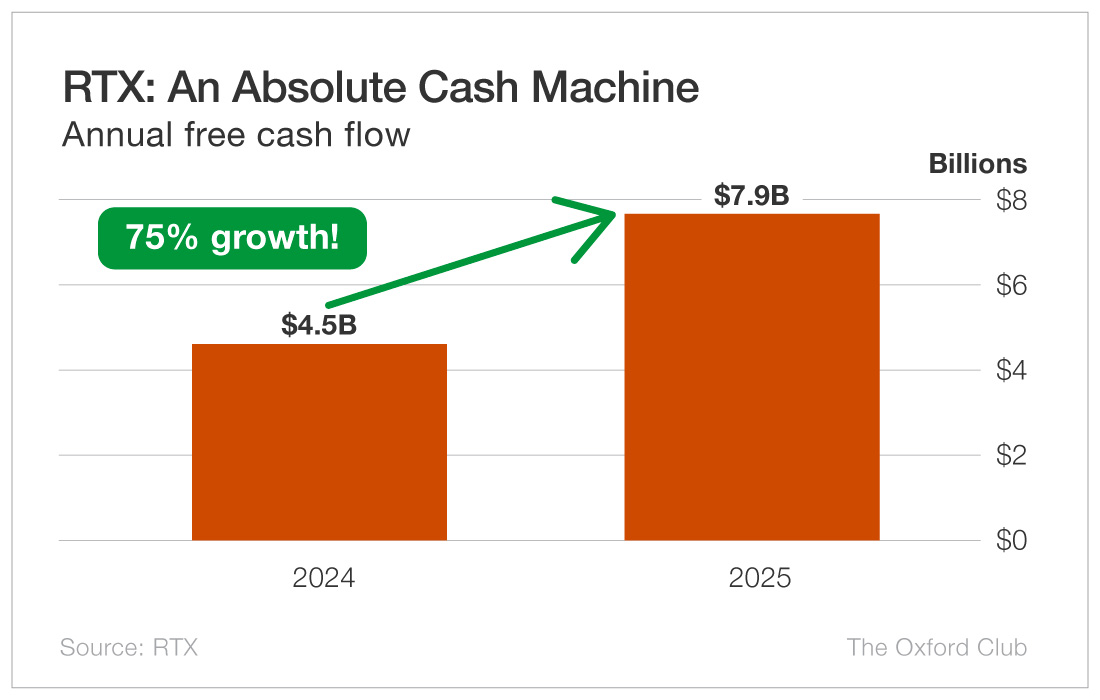

RTX grew full-year 2025 sales 10% to $88.6 billion, with adjusted earnings per share of $6.29, up 10% year over year. Free cash flow was $7.9 billion – $3.4 billion more than in 2024, an increase of about 75%. The company ended the year with a “book-to-bill” ratio of 1.56, meaning it booked $1.56 in new orders for every dollar of revenue recognized. (A figure above 1 is considered strong, as it represents increasing demand.)

For 2026, RTX projects adjusted sales of $92.5 billion to $93.5 billion, adjusted EPS of $6.70 to $6.90, and free cash flow of $8.25 billion to $8.75 billion. At their respective midpoints, those figures would equate to growth of 5% to 8%.

That’s the natural byproduct of a $271 billion backlog being converted to revenue.

RTX operates across three major business units: Collins Aerospace, Raytheon, and Pratt & Whitney (engine systems). The breadth of its portfolio means RTX benefits from nearly every major U.S. defense program simultaneously – whether it is air superiority, missile defense, naval systems, or airspace modernization.

With defense budgets rising globally and American policy now committed to rebuilding military capacity, RTX is perhaps the most direct way to capitalize on that investment cycle. It’s not the highest-upside company in this report, but it may be the most durable.

Recommendation: Buy RTX (NYSE: RTX) at the market. Set a 25% trailing stop to protect your principal and profits.

Pick No. 4: Ondas (Nasdaq: ONDS)

The first three companies in this report are established defense firms – blue chips with decades of history, massive backlogs, and contracts measured in the billions.

Ondas is something different.

It is a high-growth autonomous systems company in the early stages of a transformation that could make it one of the most important defense suppliers of the next decade.

Ondas operates through two business units. The first, Ondas Autonomous Systems, or OAS, delivers AI-powered drone and robotic platforms for defense, security, and critical infrastructure. The second, Ondas Networks, provides private wireless communications solutions for industrial customers, including railroads. OAS is the growth engine – and its results in 2025 were extraordinary.

From Startup to Defense Platform

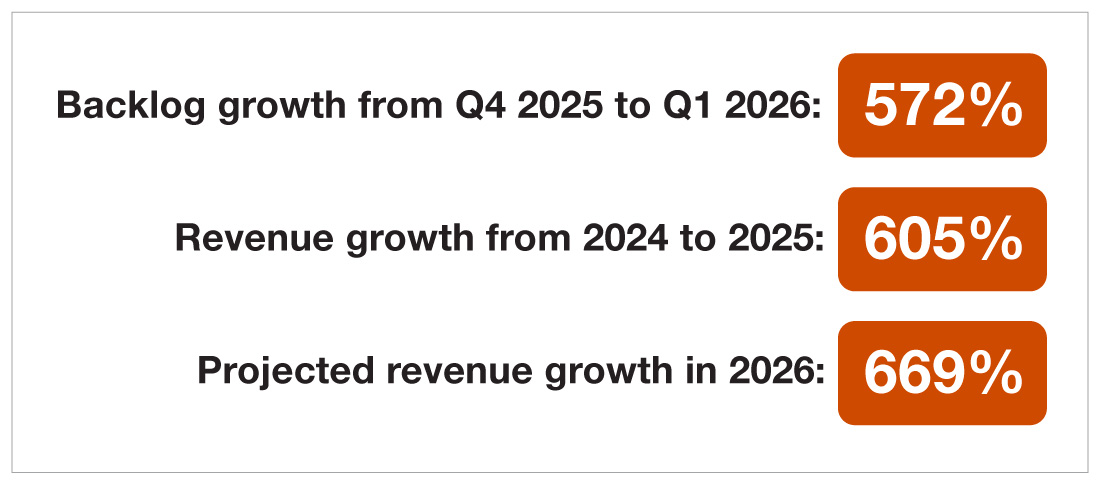

Full-year 2025 revenue for Ondas came in at $50.7 million – a 605% increase year over year.

That is not a typo.

The company grew revenue more than sevenfold in a single year, driven by accelerating demand for its autonomous systems platforms from defense and government customers around the world.

The OAS portfolio includes several specialized defense products:

- Optimus System: the first FAA-certified drone platform for fully automated aerial security and data collection

- Iron Drone Raider: an autonomous counter-drone system that intercepts and neutralizes hostile drones without human input

- Roboteam: combat-proven tactical ground robots used by military and special operations forces worldwide

- Sentrycs: counter-drone technology that neutralizes threats digitally, without jamming or physical force.

Together, these platforms constitute what Ondas calls a “system of systems” – an integrated suite that can detect, track, identify, and neutralize aerial and ground threats across a defended perimeter. That kind of interoperability is exactly what defense customers are demanding, and Ondas is one of the few companies that can deliver it from a single supplier.

The Balance Sheet and the Growth Runway

What makes Ondas unusual among high-growth defense companies is the strength of its balance sheet. As of March 31, 2026, the company held nearly $1.5 billion in cash and short-term investments. That war chest was built through a combination of a $1 billion capital raise in January 2026 and ongoing proceeds from equity offerings.

Management has deployed that capital aggressively. In 2026, Ondas has already completed five acquisitions with an aggregate value of $557 million.

Those include the $175 million acquisition of Mistral, a U.S. defense contractor with established ties to military programs and government contract vehicles. The deal gives Ondas access to more than $1 billion in existing Department of Defense contract vehicles, and it positions the company as a prime contractor rather than a subcontractor.

The results have been immediate. The company ended 2025 with a backlog of approximately $68 million. By the end of the first quarter, that backlog had grown 572% to $457 million.

New contract wins during April 2026 alone included the first phase of a $140 million strategic military engineering program, a $50 million border demining initiative in Israel, and counter-drone security operations for the 2026 FIFA World Cup.

Management has raised full-year 2026 revenue guidance to at least $390 million, a nearly eightfold increase from 2025’s $50.7 million. Revenue for the first quarter of 2026 came in at over $50 million, far surpassing guidance of $38 million to $40 million – and nearly matching the company’s total revenue across all of 2025.

The Risk and the Opportunity

It’s worth noting that Ondas is still unprofitable on a GAAP basis, and there’s always a chance that it could struggle to integrate its recent acquisitions.

As always, position size accordingly.

But consider the underlying setup: a company with $1.5 billion in cash, a $457 million backlog, $390 million in projected 2026 revenue, and a suite of autonomous defense platforms that addresses the fastest-growing segment of global military spending.

Price targets from Wall Street analysts hover around $20 per share, while the stock has recently been trading near $9.

Drone warfare and counter-drone defense have become central to modern military operations, and Ondas is set up to capture a meaningful share of that demand. It offers intriguing upside for investors who are willing to accept the risk profile of an early-stage, high-growth defense company.

Recommendation: Buy Ondas (Nasdaq: ONDS) at the market. Set a 25% trailing stop to protect your principal and profits.

The Bottom Line

While most of the coverage of the 870-page One Big Beautiful Bill has focused on the tax provisions, the defense mandates buried in Title II have received almost no attention outside the contracting community.

Therein lies the opportunity.

The $29 billion Golden Fleet initiative is not an executive priority that can be reversed by the next administration. It is federal law. There are very few companies capable of fulfilling its requirements, and those that are in the best position to do so are the ones covered in this report.

Huntington Ingalls is the only builder of nuclear aircraft carriers in the country and one of two builders of nuclear submarines – with a $54 billion backlog and the biggest contract in its history still to come.

BWX Technologies holds a monopoly on the nuclear propulsion components that every one of those vessels requires, and it boasts an $8.6 billion backlog and 77% year-over-year backlog growth.

RTX operates the broadest defense and aerospace portfolio in the world, with a $271 billion backlog and $7.9 billion in annual free cash flow.

Lastly, Ondas is building the autonomous systems infrastructure of the next-generation military, with a balance sheet, backlog, and revenue trajectory that most investors have not yet discovered.

Together, these four companies span the full breadth of America’s defense rebuild – from the ships and reactors in the water to the radar systems in the sky to the autonomous drones on the front lines.