The Best of The Oxford Income Letter: July-December 2025

55 Years and Counting: This Perpetual Dividend Raiser Provides the Most In-Demand Product in America

By Marc Lichtenfeld • Chief Income Strategist • November 2025

It’s not a secret that the demand for electricity to feed artificial intelligence is enormous.

OpenAI, the creator of ChatGPT, recently said it wants to build 250 gigawatts of new computing capacity in the next eight years. That is the equivalent of 20% of all of America’s electricity-generating capacity. If an entire country generated 250 gigawatts, it would rank seventh in the world in electricity generation.

And that’s just the demand from one AI company.

Add in a few more AI operators, crypto, general growth of the economy, and new technology, and the demand for electricity is almost hard to imagine.

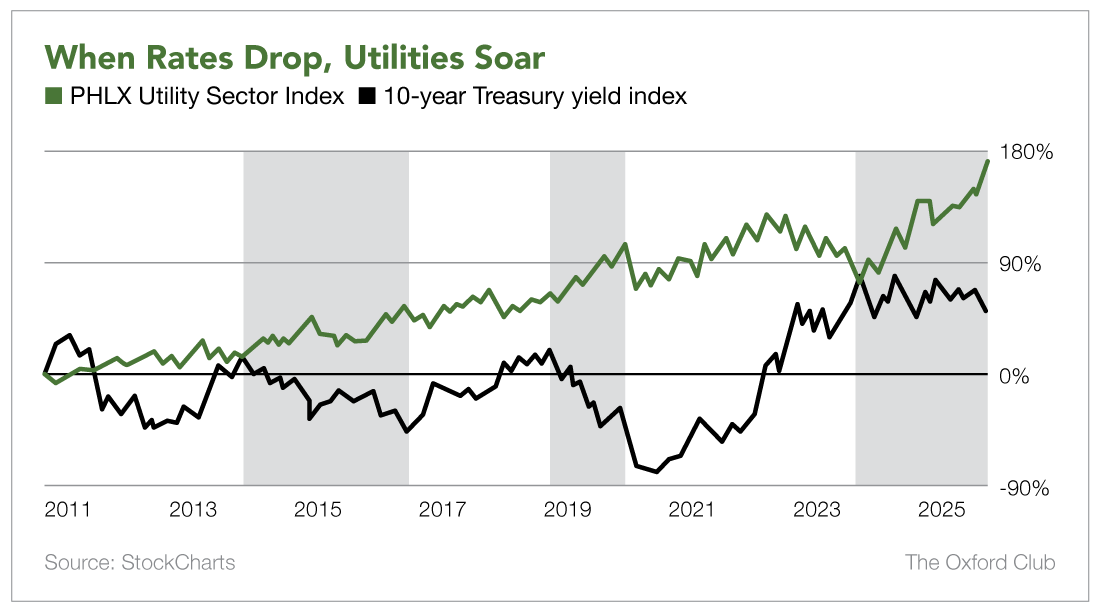

Combine all that demand with falling interest rates, and electric utilities are clearly a place to invest right now. (Utilities tend to borrow lots of money, so lower interest rates are decidedly bullish for the sector.)

Below is a chart of the PHLX Utility Sector Index and the 10-year Treasury yield. Though the timing hasn’t been perfect − especially during the pandemic − you can see the inverse relationship. Typically, when interest rates hit their peak and then begin to fall, utilities really get going, like in 2014, 2018, and 2023.

That’s why now is the time to buy a utility – especially an electric utility. But I’m not settling for just any electricity producer. You know me. I love dividends, and I want us to receive a bigger payout tomorrow than today.

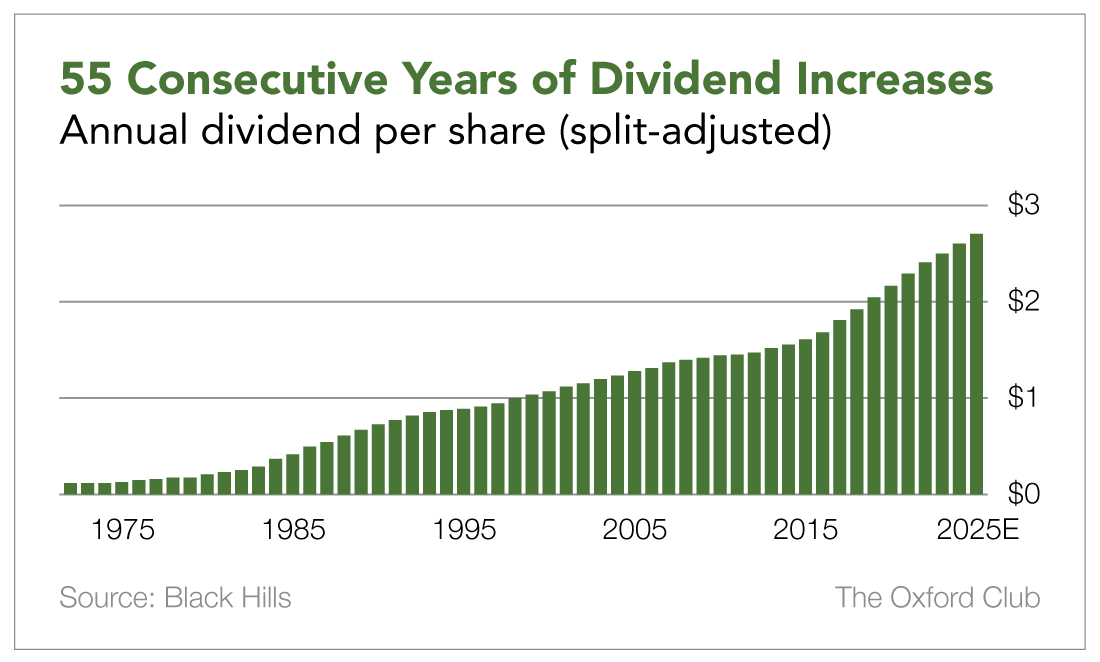

Given that this month’s recommendation has raised its dividend for 55 years in a row, I have a lot of confidence that will be the case.

Black Hills (NYSE: BKH) has hiked its dividend every year since 1971, the same year Charles Manson was convicted, Jim Morrison died, and Disney World opened. It began paying a dividend in 1942, but it’s been around a little longer than that – since 1883.

Black Hills is based in Rapid City, South Dakota, and serves 1.35 million natural gas and electric utility customers in eight states: Arkansas, Colorado, Iowa, Kansas, Montana, Nebraska, South Dakota, and Wyoming.

However, the company is about to get much larger. It announced in August that it is acquiring NorthWestern Energy (Nasdaq: NWE), which will add nearly 800,000 more customers. The combined company will generate roughly 2.9 gigawatts of electricity, operate 38,000 miles of electric lines, and produce power using thermal, hydro, wind, and coal. It will also have 59,000 miles of natural gas pipelines.

It is expected that 61% of the new company’s rate base − that is, its invested assets − will be in electricity and 39% will be in natural gas.

The merger is an all-stock deal. NorthWestern shareholders will receive 0.98 shares of Black Hills for each share of NorthWestern that they own. The transaction is expected to be completed by the end of 2026.

The acquisition of NorthWestern increases Black Hills’ annual earnings growth target to the 5% to 7% range. It should also significantly boost cash flow.

Here’s the amazing thing: That 5% to 7% earnings growth rate does not include any growth from data centers.

The company’s data center clients include Meta Platforms (Nasdaq: META) and Microsoft (Nasdaq: MSFT). Meta will be ramping up its data center operations next year, so earnings and cash flow should be higher than management’s guidance for years to come.

Black Hills will also supply the electricity for a 115-acre data center campus in Cheyenne, Wyoming, that is being developed by Related Digital. It broke ground last month and is expected to go online at the end of 2026. (Wyoming is becoming a hotbed for data centers because of low electricity costs and the amount of available land.)

Black Hills operates under a regulatory framework called the Large Power Contract Service tariff. This means that the company can offer low-cost electricity to data centers, but the data centers must pay for any upgrades so that those costs will not be passed on to consumers.

In addition to protecting residents from rate increases, the tariff also allows Black Hills to generate revenue with less capital invested and develop solutions that address customers’ specific needs.

The stock is cheap compared with its peers. It trades at less than 16 times earnings, versus an industry median of more than 20. Price-to-forward sales is at a 25% discount, and price-to-book is at a nearly 35% discount. Simply trading in line with the industry median earnings multiple would suggest a price of $80 − 13% higher than where the stock is trading now.

The Dividend

Black Hills pays a $0.676 quarterly dividend, which comes out to a 4% yield. With a five-and-a-half-decade run of annual increases, the payout will almost certainly be raised in the first quarter of next year.

When looking at a utility’s dividend safety, I use operating cash flow rather than free cash flow. Because utilities have such high capital expenditures, operating cash flow is a more accurate representation of their ability and willingness to pay their dividends.

Last year, Black Hills generated $719 million in operating cash flow and paid out just $182 million in dividends for a payout ratio of 25%. In 2025, I expect operating cash flow to be around $800 million and dividends paid to be $195 million for a payout ratio of 24%.

Assuming the NorthWestern Energy acquisition adds to earnings as the company expects, cash flow is likely to increase as well. Additionally, the more than half a century of yearly dividend increases is very important to management. I don’t believe they would’ve entered into this merger if it would’ve jeopardized the dividend.

Positive cash flow growth, a low payout ratio, and an incredible 55-year track record of dividend raises mean this dividend is very safe.

Management expects a payout ratio on earnings (not cash flow) of between 55% and 65%. Based on 2029’s analyst consensus EPS estimate of $5.17, that would come out to a dividend of $3.10 per share in four years, which would bring the yield close to 4.5% on the current entry price.

Remember, management’s guidance does not include some of that data center growth, so there is opportunity for an even faster-rising payout from this Perpetual Dividend Raiser.

Action to Take: Buy Black Hills (NYSE: BKH) for $72 or lower, and add it to the Compound Income Portfolio. If the stock is above $72, wait for it to come back in. The stock should be held in a tax-deferred account if possible. If not, it’s fine to hold it in a taxable account; you’ll just have to pay the taxes on the dividends each year.

[Editor’s Note: Marc recommended Black Hills in the November 2025 issue, but it remains an active “Buy” recommendation as of the time of this writing in January 2026. To view all of the Oxford Income Letter portfolios, click here.]

A New Portfolio… and a Smart Buy in Today’s Market

By Marc Lichtenfeld • Chief Income Strategist • July 2025

As promised, this month we’re launching our Strategic Growth Portfolio. It was great seeing so many of you write in to say how excited you are about this new addition.

Even though our focus will always be steady dividend payers and bonds, it makes sense to add some growth stocks to the mix.

While I love the predictability of dividend stocks, they’re meant to be long-term holds. But markets offer windows of opportunity that we’d be foolish to ignore.

To be clear, we’re not abandoning our core approach. We’re simply adding a third leg to the stool.

First, we’ll keep building on our foundation of dividend growers with solid fundamentals.

Second, we’ll maintain a healthy allocation to bonds, which are finally offering real yields again – the best we’ve seen in a long time.

And third, we’re now adding selective growth plays that can help us compound our wealth faster than traditional income investments.

What kind of growth plays am I talking about? Here’s the perfect example…

Thor Industries (NYSE: THO) is the world’s largest manufacturer of recreational vehicles. Think motor homes, travel trailers, and fifth wheels. If you’ve seen an Airstream, Jayco, or Keystone RV, you’ve seen Thor’s work.

It’s a cyclical business. When times are good, people buy RVs for weekend getaways and retirement adventures. But when concerns about the economy arise, RV sales dry up fast as people postpone big-ticket purchases.

Right now, we’re in one of those down cycles. High interest rates and economic uncertainty have hammered RV demand, and most investors are running the other way. This is the time to buy − not when everything is going gangbusters, every analyst rates the stock a “Buy,” and investors are flocking to it like a hipster to an overpriced flannel store.

Here’s what the skeptics are missing…

Thor’s third quarter results beat expectations on both lines. Net sales jumped 3.3% year over year to $2.9 billion, and gross profit margins expanded from 15.1% to 15.3%. The company’s North American Towable RV segment posted a stunning 200-basis-point improvement in gross profit margin.

That’s impressive given the challenging market conditions − and it’s not just luck. It’s smart management executing a proven playbook in tough times.

Thor generated $257.7 million in cash from operations in the most recent quarter. Over the first three quarters of fiscal 2025 (from August 2024 to April 2025), it improved its cash flow by over $100 million compared with the previous year. This tells us Thor is getting more efficient at turning sales into cash.

The company sits on roughly $1.5 billion in liquidity. That includes about $508 million in cash and the ability to tap into nearly $1 billion worth of credit if necessary. It has also reduced its total debt by $139 million.

This is exactly what we want to see during a downturn. Smart companies use these periods to strengthen their balance sheets and position for the next upcycle.

While the RV industry faces headwinds, Thor isn’t standing still. It’s investing heavily in the future of recreational vehicles.

In 2022, Thor unveiled two fully electric RV concepts: the Vision Vehicle and the eStream trailer. These aren’t just electric motors slapped onto old designs − we’re talking steer-by-wire technology, remote hitching and unhitching, remote parking, and self-stabilizing systems.

The Thor 2024 Test Vehicle takes these innovations even further. It’s a Class A hybrid motor home built on an EV chassis with advanced driver assistance systems.

This isn’t just about going electric. Thor is moving RVs toward semi-autonomous operation. That’s a massive competitive advantage as the industry evolves.

There are also several factors that should boost RV demand in the coming months.

Oil prices remain near three-year lows, and lower oil prices make RV travel more attractive. When gas is cheap, families think differently about going on road trips versus flying. Recent inflation declines help household budgets too.

Additionally, as economic uncertainty clears, consumer confidence should return. That typically leads to stronger retail sales.

The company expects a challenging fourth quarter, but there’s light at the end of the tunnel. Thor’s management has proved it can weather tough periods and emerge stronger. The company’s operating model is designed to ramp up and down efficiently, so when demand improves, Thor will be ready.

Earnings are expected to explode as the cycle turns. Despite Wall Street’s bearish outlook (only four out of 16 analysts covering the stock rate it a “Buy”), earnings are forecast to grow 244% between now and 2029. If the stock maintains its price-to-earnings ratio of 22, that implies a stock price of $291 in four years − up from less than $93 currently.

The stock trades at cheap levels despite the company’s market-leading position and strong balance sheet. At just over one times book value and 0.5 times sales, this creates a huge opportunity for patient investors who are willing to look past near-term noise. Thor also pays a 2.2% dividend yield, giving investors income while they wait for growth.

History shows that the best time to buy cyclical stocks is when things don’t look great. Thor’s recent results suggest the worst may be behind it.

The RV industry will recover. When it does, Thor will be positioned to gain market share and deliver outsize returns. That makes it a smart initial addition to our Strategic Growth Portfolio.

Action to Take: Buy Thor Industries (NYSE: THO) at the market, and add it to the Strategic Growth Portfolio. Set a 25% trailing stop. Hold the stock in a tax-deferred account if possible.

[Editor’s Note: Marc recommended Thor Industries in the July 2025 issue. As of the time of this writing in January 2026, the stock is up approximately 26%, but it remains an active “Buy” recommendation. To view all of the Oxford Income Letter portfolios, click here.]

Beyond Borders: The Power of Diversification

By Marc Lichtenfeld • Chief Income Strategist • December 2025

One of the things I’m most grateful for in my life is the opportunities I’ve had to travel outside the United States. Spending time in foreign countries, learning about various cultures and histories, and making friends with people from very different backgrounds have expanded my thinking and opened my eyes to many things, including how good we have it here.

But I’m guilty of the same transgression that nearly all Americans are: I don’t have enough exposure to international assets. I probably have more than most, but still not enough to be truly diversified.

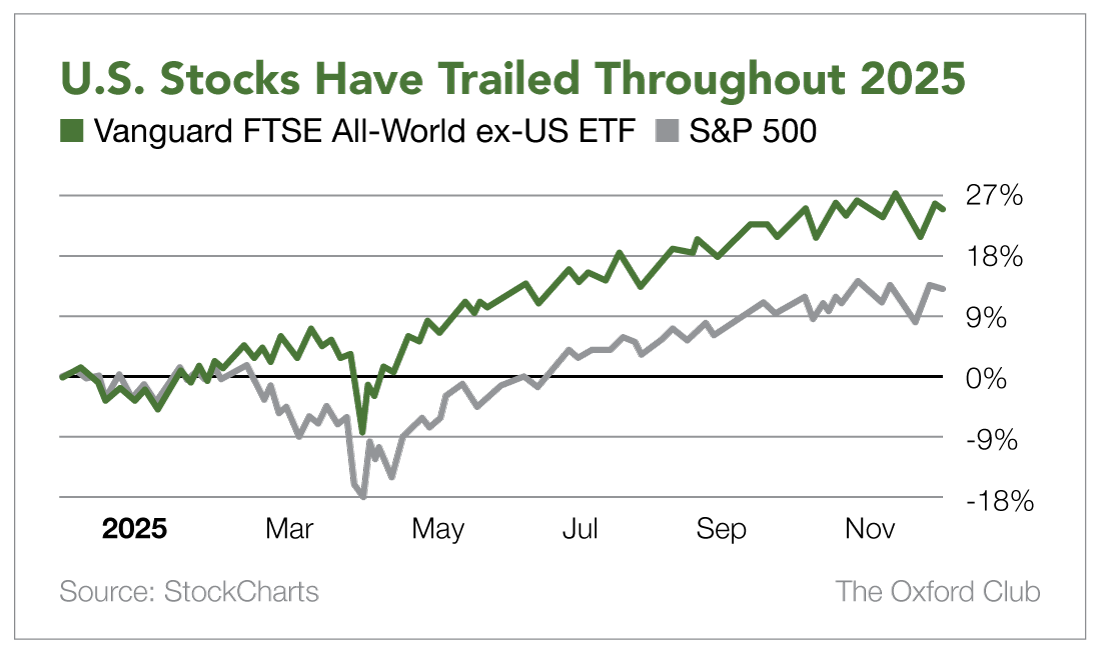

While the United States represents about 4.2% of the world’s population, it makes up roughly 26% of the world’s GDP – a huge percentage. But that still means 3 out of every 4 dollars’ worth of goods and services are produced somewhere else. If you’re not invested outside the U.S., you’re missing out.

Plus, sometimes U.S. stocks lag the rest of the world. As of early December, stocks outside the U.S. have doubled the performance of the S&P 500 over the past 12 months.

Diversification means you should own different sectors and asset classes because something will always be outperforming. The same is true when it comes to geography. Anyone who doesn’t have enough (or any) international stocks has missed some serious gains this year.

But you don’t have to get your international exposure exclusively from stocks.

There are ETFs that focus on specific regions. For example, you could invest in an Asia-focused ETF.

If you want to drill down to individual countries, you can do that too. For every ETF that invests in a well-known tech hub like Taiwan, there’s another one that invests in a much smaller market like Finland. However, I don’t recommend buying individual country ETFs, as many international markets are not very liquid.

Foreign bonds are not easy to come by. There aren’t many listed in the U.S., and I would only buy the bonds of safe, large foreign companies. I’m always looking for them, and I will recommend one in the Fixed Income Portfolio if I can find one that I’m comfortable with.

There are foreign bond funds, but I’m not a fan of most bond funds, because funds typically don’t have maturity dates. The whole purpose of investing in bonds, aside from the income, is knowing exactly how much your investment will be worth on a specific date (the maturity date). Since there is no maturity date on a fund, you’ll never know what it will be worth at some point in the future. And if interest rates rise, bond funds usually decline in value.

Another option is investing in foreign currencies to diversify away from the U.S. dollar.

The dollar has lost roughly 10% of its value this year. If you’re concerned about a further drop, you can invest in ETFs that own either a basket of currencies or individual currencies such as the euro, yen, and Canadian dollar.

Very soon you will be able to own foreign currency via Battle Bank. The online bank is expected to open its virtual doors in the first quarter of 2026. You can open FDIC-insured CDs or deposit accounts in 20 currencies, including all of the major ones, like the euro, the yen, and the Chinese yuan, and even smaller currencies like the New Zealand dollar and Indian rupee. (To learn more about Battle Bank and get on its waitlist with no commitment whatsoever, visit https://oxford.club/battlebank.)

There’s also international real estate. That takes a bigger commitment than buying a few shares of stock or an ETF, but it’s an excellent way to diversify outside the U.S. and own an asset that you can actually use and enjoy. Plus, you may be able to rent it out and generate income when you’re not there.

Since I was a teenager, I’ve dreamed of owning a home in a tropical paradise. I live in Florida and am currently enjoying a beautiful 70-degree day in December, but that’s not what I mean. I want something with a different look and culture.

I may be getting closer. Last month, I was scouting properties in Costa Rica. It’s one of my favorite countries that I’ve visited, and the dollar goes further there than it does here at home.

There are lots of amazing places − especially in Latin America and Europe − where real estate is cheaper than in the U.S, the cost of living is lower, and there is potential for significant capital gains. Some countries also have residency programs if you buy real estate.

The one caveat is I wouldn’t buy overseas unless you have a trusted person or organization to help you with the process. That could be a local lawyer, a realtor who has been referred by someone you trust, or a company like our partner Real Estate Trend Alert (RETA).

Led by the Club’s Real Estate Strategist Ronan McMahon, RETA finds property deals for expats and guides them through the process. RETA has helped me tremendously with my search in Costa Rica. (By the way, all Oxford Club Members are entitled to a free RETA subscription. To claim yours, go to https://oxford.club/joinRETA.)

Regardless of how you go about it, make sure your investments are not focused only on the USA. It’s a great big world, and there are plenty of opportunities for gains and income that shouldn’t be missed.

Disclosure: The Oxford Club has a financial relationship with both Battle Bank and RETA. I am also an investor in Battle Bank and will be moving my accounts there when it opens.

How to Earn 6% to 7% in the Fed’s New Rate-Cut Era

By Anthony Summers • Director of Trading • October 2025

The Federal Reserve has turned the corner.

A quarter-point cut may not sound dramatic, but it marks a real shift. For bonds, it means the ceiling on rates has likely been set. After two years of elevated yields, the path ahead points lower. Investors now have a window to lock in attractive income before those yields start to slip.

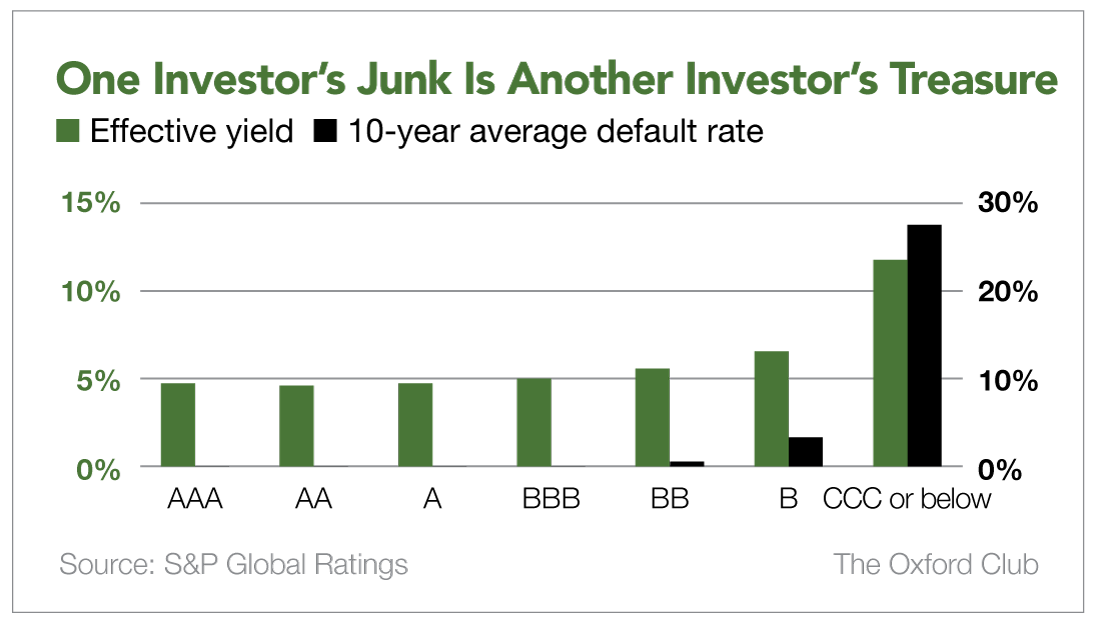

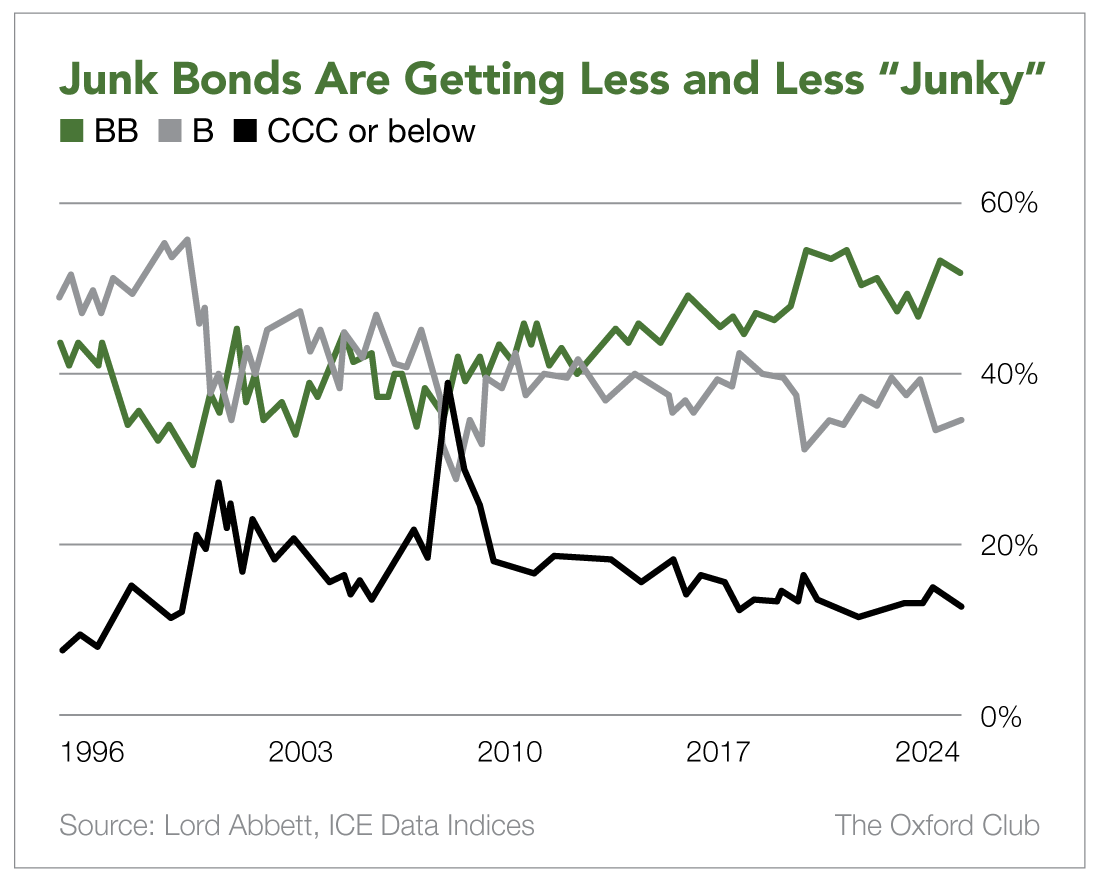

Earlier in this issue, Marc rightly pointed out the uneven performance of high-yield (or “junk”) bonds, writing that they’ve shined in some easing cycles and flopped in others. But for investors who can handle a bit more uncertainty, some of the best opportunities today sit in the safer tiers of the high-yield market, where credit risk is far more muted than the label suggests. (As I often say, not all junk is equally junky.)

Bonds rated BB, the highest rung of high-yield, now yield about 5.5%. B rated bonds pay more − closer to 6.6%. Bonds rated CCC and below yield almost 12%, but at a scary 27% average annual default rate.

In contrast, BB rated issuers have a default rate of just 0.2%. Even B rated companies default only 1.8% of the time. That’s far from catastrophic.

This is the part most investors miss: While the “junk” label is applied broadly, the reality isn’t so stark. In fact, in terms of risk, BB bonds and many B rated bonds are much closer to investment-grade than to the dicey world of CCCs.

The chart above makes the case clear. BB bonds offer a 10% larger yield than BBB bonds (5.5% vs. 5.0%) with only marginally higher risk. That’s why so many professional bond managers treat them as a sweet spot between safety and income.

It’s also worth noting that the composition of the high-yield market has improved. More than half of all junk bonds are now rated BB, thanks to upgrades and new issuance. Meanwhile, the riskiest slice, CCC and below, is as small as it’s been in decades.

In other words, the overall market is higher-quality than the scary “junk” nickname implies.

It also helps that the fundamentals of high-yield issuers are stronger today than in past cycles.

Since the pandemic spike, leverage ratios have fallen back toward long-term averages, meaning companies are carrying less debt relative to their earnings. At the same time, interest coverage ratios remain healthy. Many issuers are producing four to five times the cash flow needed to service their interest obligations.

That’s a wide margin of safety – and a key reason the default risk in BB and B bonds has stayed so low despite tighter policy and higher borrowing costs.

The Fed’s easing tilt makes this moment even more attractive. Falling rates give companies additional breathing room by lowering refinancing costs and allowing them to extend credit cycles. That’s a tailwind for firms that already had solid balance sheets but were feeling the pinch from elevated yields over the past two years.

In this environment, BB and select B rated bonds look especially compelling. Their yields compete with long-term stock market returns, but with far less volatility. With the Fed easing, the risk-reward balance tilts even further in investors’ favor.

With the yield curve in flux and the Fed aiming for a soft landing, this corner of the bond market deserves a fresh look. As always, not every bond is created equal.

For those willing to look past the “junk” label, there’s value hiding in plain sight − and right now, it’s hiding in bonds most investors continue to overlook.

Marc’s Mailbag

Q: I mainly invest in dividend-paying stocks and own almost all the Oxford Income Letter stocks.

But the effect AI may have on these stocks concerns me since that is a frequent topic these days.

I assume you’re thinking about this also. I wonder if you might share your thoughts specifically regarding the Oxford Income Letter stocks and AI with your readers. Thank you. – Connie M., July 2025

A: Interesting question, Connie. I assume you’re talking about the effect AI could have on the various companies’ businesses.

I don’t have the space to write about each company one by one, but I believe AI will boost productivity significantly over time.

Drug companies should see shorter development times. The same goes for technology companies. Financial institutions should be able to make better decisions. Eventually, AI will improve just about every sector on the planet.

I’m bullish on the use of AI. It will certainly be disruptive, and some jobs will be affected, but overall, I expect it to be as much of a game changer as the internet.

It’s almost hard to remember life before the internet. I suspect that in the not-too-distant future, we’ll say the same about AI.

As was the case with the internet, we likely can’t even imagine how AI will affect our lives as it continues to develop.

Q: In the dividend portfolios, how much do you recommend for each security in the portfolio as a starting balance before adding another recommended dividend security? – Michael M., August 2025

A: Great question, Michael.

The Oxford Club recommends investing no more than 4% of your portfolio in any one position. That means if you are going to invest $100,000 total, you’d invest only $4,000 maximum per position. Now, that doesn’t necessarily mean all of the money has to be deployed at once. Perhaps you have $50,000 to invest now and you plan on adding more funds in the future. You could start with $2,000 or less per position, then add more to each position (or into new stocks) monthly, quarterly, or as funds become available. Just remember the 4% rule. That way, if a position goes against you, it won’t hand you a devastating loss.

Q: I am a lifetime member and in The Chairman’s Circle. I am fully invested in both Alex’s and Marc’s long-term portfolios (all of them). I have been since 2018. In these portfolios, there is not a lot of turnover. So given that I have held most of these positions for eight years, an average return would be 80% for each position. I know you cannot get specific, but it is easier to use an example. Berkshire Hathaway is up 136% since I got in, and I am sure there are positions that are more than that and less than that. At what point as the years go on do you say it is time to take those profits and put the money to use in new upcoming stocks? − Paul, November 2025

A: Great question, Paul.

In the Oxford Income Letter portfolios, I don’t determine when to take profits based on how much a stock is up. For long-term portfolios, we want to let our winners run. That’s what will really move the needle.

We have five open positions that are up more than 100%. The two largest winners are AbbVie (NYSE: ABBV) and RTX (NYSE: RTX), which are up 482% and 877%, respectively. Imagine if we had sold when both were “only” up 100% or even 200%. We would have missed out on huge gains.

There are two reasons I’ll recommend selling a position:

- The fundamentals have changed. If business is weakening, the dividend is stagnant, or the company can no longer afford the dividend, I’ll sell.

- The stock hits our stop price. I recommend 25% trailing stops on some positions, and I add hard stops to other positions when I’m not willing to risk giving up any more of our hard-won profits. Either way, if a stock closes below the stop price, we’ll exit and put the money in our pocket.

The above rules are not the case for short-term trading, which requires more of a “hit it and quit it” strategy. But for expected long-term holdings, if it ain’t broke, don’t fix it. Let your winners run.

Q: In a bull market, as stocks are moving higher and the value of the dollar is moving lower, can we end up in a position where the gain in the portfolio is being outstripped by the loss in the dollar’s buying power? Should we be investing in real asset companies, be it in real estate, farm equipment, military hardware, etc.? − Marc K., September 2025

A: Good question, Marc. I don’t expect the dollar to fall so much that it negates the gains − particularly the long-term gains − of the market. Nor do I expect inflation to rise so high that it offsets the market’s total return over the years.

That being said, I am in favor of owning companies like the ones you described. That’s one of the reasons we own fertilizer company Nutrien (NYSE: NTR), defense contractor RTX (NYSE: RTX), and real estate companies like CareTrust REIT (NYSE: CTRE).

I tend not to worry too much about currency fluctuation. While the U.S. dollar is down about 11% year to date, it’s only a percentage point or two away from where it was 10 years ago.

The value of the dollar can certainly swing, but to try to manage a portfolio based on where we expect the dollar to go is market timing, and we don’t engage in market timing.