The 29% Account: Accessing America’s Secret Trust Fund

For most people, saving money means putting it in a bank.

That’s what we’re taught. Deposit your cash. Earn a little bit of interest. Keep it safe.

The problem is that safety doesn’t build wealth. It barely preserves it. And in many years, it doesn’t even do that.

While the big banks offer savers mere fractions of a percentage point, they’re making fortunes for themselves by parking billions of dollars elsewhere. Not in checking accounts. Not in CDs. And not in products they advertise to the public.

The idea behind the “29% Account” comes from that simple truth.

It isn’t an account in the traditional sense. There’s no branch office. No application. No interest rate scrolling across a screen.

It’s about owning the right kind of asset − one that produces cash, requires very little upkeep, and benefits from long-term economic activity instead of short-term predictions.

The “29% Account” − the asset that has returned an average of 29% per year since 2000, making it one of the very best performers in the entire market − is Texas Pacific Land (NYSE: TPL).

How a Forgotten Land Grant Turned Into a Cash Machine

To understand the opportunity here, you need to understand what this company actually owns.

Texas Pacific Land traces its roots back to 1888, when it was formed to manage 3.5 million acres of land after the bankruptcy of the Texas and Pacific Railway. For decades, it was a passive land trust that collected royalty income and passed it along to investors (including a young Warren Buffett).

Around the 1970s, the trust’s performance began to decline due to decreased oil production from conventional wells, and it began to sell off acreage to generate cash. Soon, it looked more like a sleepy income vehicle than a growth story.

However, that changed around 2010 with the rise of two technologies that would transform the industry: horizontal drilling and hydraulic fracturing. In 2021, the trust − buoyed by rapid production and revenue growth − was converted to a corporation. Less than four years later, TPL joined the S&P 500, reflecting both its size and its durability.

That inclusion didn’t change the business. It simply acknowledged what had already been built.

Today, TPL is one of the largest landowners in Texas, controlling approximately 873,000 surface acres and roughly 207,000 net royalty acres, almost entirely concentrated in the Permian Basin. This is not fringe territory. The Permian is the most productive oil basin in the United States and one of the lowest-cost energy regions in the world.

Crucially, TPL is not an oil producer. It does not drill wells. It does not pay for rigs. It does not fund exploration budgets.

Instead, it owns the land and the perpetual royalty interests beneath it. When operators drill and produce oil and gas, TPL receives a share of the revenue − without paying a dime in operating or capital expenses.

That distinction shows up clearly in the numbers.

An Elite Performer With Room to Grow

Over the first three quarters of 2025, TPL generated $586.6 million in total revenue, up 12.8% year over year, despite oil and gas prices sliding for most of the year.

Even more striking were the margins. Adjusted EBITDA margins reached approximately 87%, and net income margins were about 61%. Those are not energy company margins. They are royalty margins.

Oil and gas royalty revenue alone totaled $315 million through the first three quarters, supported by record royalty production of about 33,600 barrels of oil equivalent per day. Because TPL does not pay to drill or operate wells, that production translated directly into free cash flow.

This structure is why management consistently emphasizes resilience. As CEO Tyler Glover put it during the company’s third quarter 2025 earnings release, TPL’s model is “designed to succeed throughout the commodity cycle without the need for hedging,” preserving upside when conditions improve.

TPL is also continuing to pursue growth by acquiring adjacent royalty and surface assets. In 2024 and 2025, the company spent more than $900 million − all in cash − acquiring high-quality acreage, further strengthening its position.

If oil and gas royalties were the whole story, TPL would already be a rare opportunity. But within the past decade, the company added a second, fast-growing business.

Modern drilling consumes enormous amounts of water and produces even more wastewater. That water must be sourced, transported, treated, and disposed of.

TPL owns the land, infrastructure corridors, and pore space that make those services possible.

In 2024, the company’s Water Services and Operations segment generated $265 million in revenue and $139 million in net income, both records. Water sales volumes increased more than 30% year over year, while produced water royalties grew 24%.

By the third quarter of 2025, water-related revenues had reached new highs again, with $80.8 million from the Water Services segment in the quarter and $44.6 million from water sales alone.

This matters because water revenue is tied to activity, not prices. As long as drilling continues, water will still be required − and TPL will still get paid.

But here’s the key part of TPL’s growth story: All of the company’s oil, gas, and water assets are about to become even more valuable.

Right now, the United States is in the middle of an AI data center construction boom. There are 3,000 data centers under construction or planned across the country, each requiring 100 to 300 acres of land and consuming enough electricity to power 150,000 homes running 24/7. Operating costs for a single large-scale facility can exceed $1 billion per year.

The primary roadblock to AI’s growth isn’t technology. It’s finding regions with three critical resources: available land, cheap and reliable energy, and abundant water for cooling. (Each data center uses between 1 million and 5 million gallons of water daily − the equivalent of draining and refilling five Olympic-sized swimming pools every 24 hours.)

TPL’s nearly 900,000 acres sit in one of the cheapest energy regions in America. More importantly, it owns water rights to massive underground aquifers across the region.

In other words, the success or failure of AI hinges on three things… and TPL has a stranglehold on all three.

Tech giants like Microsoft, Google, Amazon, and Meta are all evaluating sites in the Permian region, and TPL’s unique position − controlling land, energy access, and water rights in a single package − puts it at the center of their planning.

Wall Street analysts have already started connecting the dots. A report from Business Insider noted that “investors [are betting that TPL’s] land will be key for data center buildouts.” Another called the company a “Permian Basin powerhouse with an AI edge.”

If even a fraction of America’s data center development ends up on TPL’s land, it could add hundreds of millions in annual revenue in the future.

That’s why I believe the next 25 years could rival, or even exceed, the extraordinary returns of the last century.

You simply can’t recreate this kind of business.

You can’t manufacture nearly a million acres in the Permian Basin, you can’t retroactively secure royalty rights before development accelerates, and you can’t build a better setup to meet AI’s water, land, and energy demands. Assembling a comparable footprint today would require enormous capital.

In short, dethroning TPL would be almost impossible.

An Income Investor’s Dream

Let’s be clear about one thing: This investment doesn’t come with a fixed yield or a guaranteed return.

What it does offer, though, is ownership in a company that converts long-term economic activity into cash with almost no incremental cost. Over time, that cash compounds.

TPL ended the third quarter of 2025 with no debt and approximately $532 million in cash and equivalents on its balance sheet. That financial strength gives management flexibility − and they’ve used it.

Rather than chase growth for its own sake, TPL has consistently returned excess cash to shareholders.

In 2024 alone, the company returned $347 million through dividends, including a $10 per share special dividend, the largest in its history. It also raised its regular quarterly dividend from $1.17 to $1.60, a sizable 37% increase. The regular dividend has now been increased for 22 consecutive years.

TPL has also repurchased shares, reducing the share count and increasing each shareholder’s claim on the business.

This combination of high-margin cash flow, minimal reinvestment needs, and disciplined capital returns is a textbook setup for compounding − and helps explain why TPL is one of the top-performing investments in the market over the past quarter-century.

Now, the 29% figure isn’t a promise, and it isn’t magic.

But it is math.

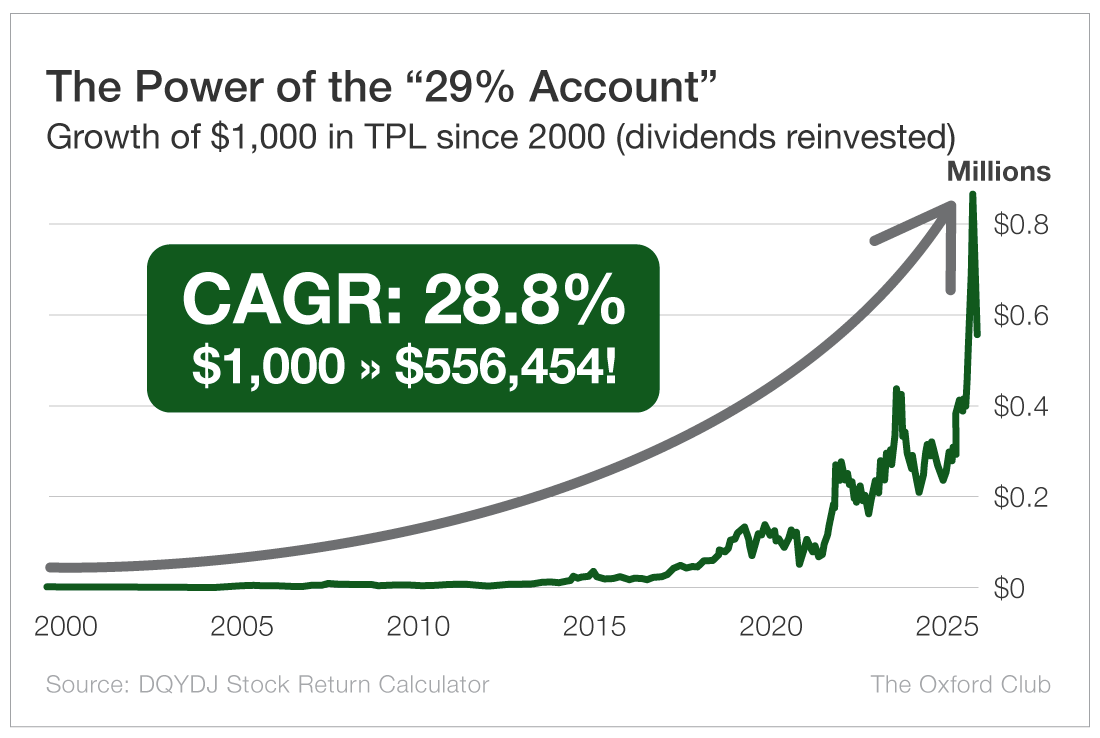

Specifically, it’s a compound annual growth rate calculated over 25 years, starting in 2000, when TPL shares were thinly traded and largely ignored.

From 2000 to 2025, TPL posted a cumulative return of over 55,000%, with dividends reinvested. Annualized, that comes out to just under 29%. (Since TPL assumed its current structure in 2021, the annual return is actually even higher − over 31%.)

That means a $1,000 investment in 2000 would’ve grown to $556,454 by the end of 2025. If you’d simply added $10 each month, you’d be sitting on close to $1 million.

With the company’s two-decade track record of boosting its dividend, reinvesting your dividends is the best way to maximize your gains. (Plus, if you hold the stock in a Roth IRA, all of that money grows tax-free.) That being said, its performance has still been terrific even without dividends reinvested. What works best for someone else may not be the best option for you, so reach out to a tax professional with any questions about your specific situation.

Keep in mind that those returns were earned through long stretches when energy stocks were unpopular, volatile, or outright dismissed. They included major drawdowns and years of flat performance, and the company’s revenue is still influenced by commodity prices and operator activity.

But that’s the difference between a bank savings account and ownership in a real business. You don’t get this kind of upside without a measure of risk.

Even so, this is one of the best risk-reward profiles you’ll find in this market.

The Real Meaning of the “29% Account”

Balancing risk and reward is where most investors fail. They want the outcome without enduring the process.

Texas Pacific Land rewarded investors who understood the business and were willing to hold it through cycles − not because the stock was always loved, but because the underlying economics kept working.

The real difference between institutional investors and everyday investors isn’t access. BlackRock, Vanguard, JPMorgan Chase, and Bank of America own the stock for the same reasons individuals do: scarce assets, exceptional margins, a fortress balance sheet, and exposure to long-lived economic activity. And you can buy the stock right alongside them.

The difference is patience.

Buying a great business is easy. Holding it long enough is not.

TPL’s stock history includes long periods of stagnation and sharp declines. Investors who treated it like a trade often sold before compounding had time to work.

Institutions, by contrast, are built to wait. They measure results over years, not quarters. That structural patience is the hidden edge behind numbers like 29%.

The lesson here is straightforward: Wealth isn’t built by parking money in low-yield accounts. It’s built by owning productive assets with durable advantages and allowing time to do the work.

Texas Pacific Land is not a shortcut, and it won’t produce the same results every year. But it is a clear example of how ownership, discipline, and patience can compound into extraordinary outcomes.

The “29% Account” is more than just a stock. It’s a way of thinking. For the few investors willing to adopt it, history shows what’s possible.

Recommendation: Buy Texas Pacific Land (NYSE: TPL) at the market. Set a 25% trailing stop to protect your principal and profits.