The 10X Portfolio

The “frenzy phase” of our current tech stock boom is a rising tide set to raise a lot of ships. Many more than one microcap tech stock is solving the critical problems faced by the modern economy and transforming entire industries overnight.

This is a once-in-a-generation wealth creation event we haven’t seen since the 1990s.

Between the second term of Trump’s presidency (the most pro-stock-market president in history), the $18 trillion in cash held by Americans ready to flood into the market, and the inevitable intervention of the Federal Reserve, we are looking at a perfect storm to send microcap stocks into the stratosphere…

Especially if they have the key criteria of 10X, 50X, and even 100X millionaire-maker stocks:

- Three consecutive quarters of sales growth

- Increased earnings per share (EPS) year over year

- A relative strength index (RSI) over 40 during the last 14 trading days

- Insider buying

- Innovative and disruptive products or services.

And the three stocks in this report are hidden champions positioned to absolutely explode during this rare market event. Each one is shaking up its industry in profound ways. Each has the potential to soar 1,000% over the next 12 months. And each has the potential to make you millions, like Netflix, Apple, and Nvidia made their early investors…

Navigating the Future

Up first is a company revolutionizing a service that has become totally ubiquitous in the modern world: GPS.

Traditional GPS uses satellites to show your location on a map and can give you road directions or help you find a location you’re looking for. But the main limitation of traditional GPS is verticality. It can only display your location on the x- and y-axes; it’s two-dimensional.

McLean, Virginia-based NextNav (Nasdaq: NN) is changing that, though. Its GPS, dubbed the TerraPoiNT system, doesn’t use satellites at all. Instead, it uses the terrestrial 5G network to build a 3D map that overcomes the limitations of GPS, which doesn’t work indoors and sometimes malfunctions in urban areas.

NextNav’s system can tell a first responder, for example, exactly which floor of a skyscraper someone is on. If someone has a heart attack on the 20th story of a building, seconds could mean the difference between life and death, and the paramedics can save that time by not having to search for which floor the person called from. They will be able to see exactly where the call came from and go directly to them.

A terrestrial GPS network is also more robust and can act as a backup to the satellite-based GPS network if it were to be disabled due to inclement weather or a cyberattack. A one-day outage of a satellite network would create an economic loss of $1.6 billion. But NextNav’s terrestrial network can soften that blow by lowering that cost by $663 million.

NextNav is adding an entirely new dimension to GPS technology, and its network is now available in 4,400 cities around the United States. That means it satisfies the disruption and innovation criterion I look for in a stock. It’s also making a mint doing it…

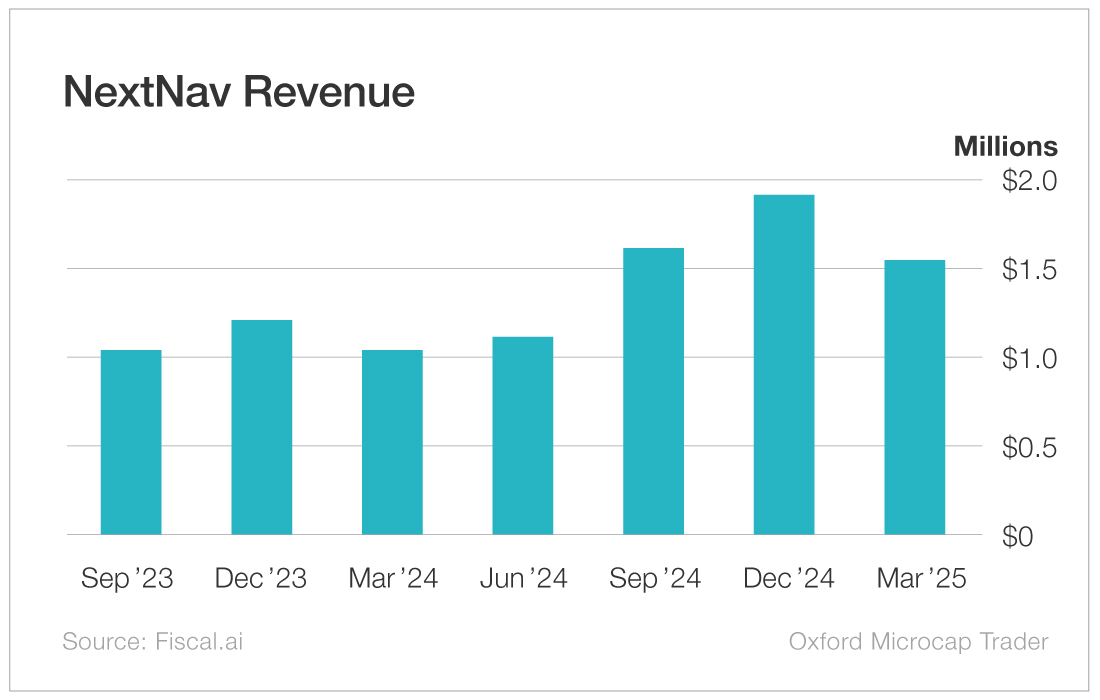

The company’s revenue has been growing by leaps and bounds over the last seven quarters, more than double what I look for. In the last three quarters, Q3 2024, Q4 2024, and Q1 2025, revenue has grown by 56.5%, 58.6%, and 47.1%, respectively, year over year. This easily satisfies the revenue growth criterion.

EPS surged 57% year over year in Q1 2025, the most recently reported quarter. So that’s the EPS growth I look for sorted, another criterion met.

Up next is RSI. An RSI of 30 or below means the stock is oversold, that there’s too much selling pressure. An RSI of 70 or above means the stock is overbought, that there’s too much buying pressure, and the stock is likely to run out of momentum soon. So, 70 is high, but even if it drops, as long as the RSI remains over 40, this stock has what I’m looking for., and NextNav easily satisfies my third criterion.

NextNav’s RSI or relative strength index, is sitting at 70.39 at the time of writing. That means it has some considerable buying pressure driving it upward but it is about to run out of runway. Still, like I mentioned, as long as the RSI remains over 40 this stock fits my criteria.

Finally, insider buying. It’s the ultimate good sign for a company’s prospects when the people who know it best are buying up shares. They do that for only one reason: They think it will go up. And here, NextNav does not disappoint. Neil Subin, a director, bought 225,000 shares in August 2024. He hasn’t sold since, and that’s the sort of thing I like to see. And that means NextNav meets all the criteria I am looking for.

It’s also trading at bargain-basement prices at the moment. Buy in while it’s still a bargain…

Action to Take: Buy NextNav (Nasdaq: NN) at market. Set a 25% trailing stop to protect your principal and your profits.

Drill, Baby, Drill

One thing we can be absolutely sure of is that Trump will be a godsend to the oil and gas industry in his second term. He was very pro-American energy in his first term, and he has already doubled down on his energy policy in his second term…

And companies like Denver, Colorado’s SM Energy (NYSE: SM) will take off as a result.

The company’s business is straightforward. It produces oil and natural gas in the states of Texas and Utah. As of its most recent estimates, it had 492 million barrels of oil equivalent in its estimated and proven reserves. It also has interests in 825 gross-productive oil wells and 483 gross-productive gas wells in the Midland Basin and South Texas.

What makes SM so innovative are two factors.

First, the company’s best wells operate more efficiently than its peers. Its Midland Basin assets produce as much as 50% more oil than the competition.

Second, the company is very committed to both environmental stewardship and the safety of its employees, bucking the public perception of oil and gas companies. It is committed to not flaring, that is, burning off excess gas without capturing or using it, more than is absolutely necessary. If SM is extracting gas, it wastes as little as possible: 99% of what it pulls out of the ground is captured and sold or used immediately.

SM is also aiming to reduce its greenhouse gas emissions by 50% by 2030. It also actively works with many state and federal organizations to keep environmental damage to an absolute minimum.

By producing fuel as efficiently as it does with as little environmental damage as possible, SM easily meets my criterion that a company be a disrupter and an innovator in its industry. And it proves that environmental protection need not come at a huge cost to the bottom line…

Revenue has been growing steadily despite a slight hiccup in Q3 2024. Before that slight interruption, Q2 2024 saw growth of 16.8%, then a dip of 4.2% in Q3 2024 before surging 38.4% in Q4 2024 and 50.2% in Q1 2025. I would say it satisfies my first criterion well enough, especially considering its five-year compound annual revenue growth of 13.2%.

EPS has also been growing. Q1 2025 saw EPS climb 40.3% year over year. So SM easily meets my second criterion.

The company’s RSI is almost perfect, at 47.48, it has plenty of room to grow. What’s more, this industry, and by extension this company, has been operating with a hostile administration for four years. I fully expect it to turn around in Trump’s second term.

As for insider buying, this company hasn’t seen much activity. In February 2025, Barton Brookman Jr., a director, bought 7,000 shares and in May 2025, Herbet Vogel, the CEO, bought 1,000 shares. That tells me they’re anticipating growth in the future and have likely been working on taking every advantage from the return to sensible energy policy under the Trump administration. Consider my fourth criterion fulfilled, with the caveat that we will keep an eye on insider activity as the company’s leadership reacts to Trump’s energy policies.

SM is a bit more speculative, but the potential for oil and natural gas companies in Trump’s second term is very enticing. And SM is an innovator with solid growth and financials.

Action to Take: Buy SM Energy (NYSE: SM) at market. Set a 25% trailing stop to protect your principal and your profits.

Go With the Data…

A company you can always bet on doing well is a company that does something simple – and does it better than anyone else. And that’s NIQ Global Intelligence (NYSE: NIQ) in a nutshell.

NIQ is one of the most powerful – and least understood – data companies in the world. It tracks trillions of individual retail transactions across more than 90 countries, covering consumer packaged goods, grocery, e-commerce, and now real-time AI-driven demand forecasting.

If brands like Coca-Cola, Nestlé, Procter & Gamble, Walmart, Amazon, and Target want to know what consumers are buying, where they’re buying it, how price changes affect demand, and what will sell next month, they turn to NIQ.

What the company does is simple: It sells data and predictive insight.

But the way it does this – by layering artificial intelligence over one of the largest consumer datasets on Earth – is highly innovative and has pushed subscription revenue, enterprise contracts, and pricing power steadily higher. That easily satisfies my criterion of innovation and disruption. And that shows up clearly in the company’s financials…

Starting off with revenue growth…

Over the past two years, NIQ has produced consistent double-digit revenue growth as a public company. Revenue moved from roughly $3.7 billion in 2023 to more than $4.1 billion in 2024, and through the first three quarters of 2025 was tracking in the $4.5-$4.7 billion range on a trailing-12-month basis.

That places its year-over-year revenue growth firmly in the 10%-13% range, with recurring subscription revenue accounting for more than 80% of total sales. That easily satisfies my first criterion.

EPS growth year over year is also improving…

As a recently listed company, NIQ has moved through its post-IPO investment and restructuring phase and is now entering a margin-expansion cycle.

Through 2025:

-

Adjusted EBITDA margins moved into the high-20% range

-

Free cash flow expanded meaningfully

-

Wall Street expects double-digit adjusted EPS growth in 2026

That comfortably satisfies my second criterion. And the company’s RSI is just about perfect…

As of early December 2025, NIQ’s 14-day relative strength index has been fluctuating between the mid-50s and low-60s. That’s exactly what I want to see – strong momentum without being overbought.

That satisfies my third criterion.

And the insiders agree…

Since the IPO, senior executives and directors have made open-market share purchases during periods of post-IPO volatility, while private-equity sponsors KKR and Advent remain major long-term shareholders.

Just as important, there has been no pattern of aggressive insider selling. That tells me management and long-term sponsors are aligned with shareholders and expect the business to continue compounding.

That satisfies my fourth criterion.

Put all that together and you have a winner. NIQ doesn’t depend on consumer fads, advertising cycles, or single products. It monetizes data subscriptions, enterprise analytics, and predictive AI – the backbone of modern retail decision-making.

As long as commerce exists, NIQ’s data will be in demand.

Action to Take: Buy NIQ Global Intelligence (NYSE: NIQ) at market. Set a 25% trailing stop to protect your principal and your profits.

Millionaire’s Microcap Portfolio

The “frenzy phase” of this tech boom will be one of the greatest wealth-creation events since the 1990s. Microcap stocks like the three in this report will be the biggest wealth creators in that event.

Each one is trading for bargain-basement prices but has great financials, innovative products, and serious potential. They’re hidden champions in the making, set to flourish as soon as the myriad triggers in this market are pulled.

These are the stocks with the potential to be the next Google, Netflix, Amazon, or Nvidia… and, a few years from now, you’ll be glad you invested in them.