Superbonds: Grow Your Nest Egg and Lock In Up to 334%

Every once in a while, you get a good stock that doubles… triples… maybe even quadruples your money in a few short years.

We all love those stocks…

But it’s the remaining stocks in the market that can be nerve-wracking…

Especially with all the volatility this year.

For those of you who can’t stand the uncertainty of it all… the constant ups and downs… the vulnerability to elections and pandemics and who knows what else… and the dramatic crashes that occur in the stock market…

That’s why my research service is dedicated to teaching American Stock Quitters how to use the power of certain bonds to increase their returns.

Now, we’re not suggesting that you pull your money out of the market. Instead, we’ve been sidetracking stocks by investing in the bond market.

And here’s the strangest thing: You can often get BETTER returns than you can in the stock market.

These are a very special type of bond (I call them superbonds). They offer much bigger returns… locked in and backed by a legal contract.

So, most importantly, we’ve been able to collect these returns with peace of mind, not worrying about a sudden market crash, a political event or a disease cratering our hard-earned savings.

And if you’re reading this report, you’ll learn how to get that peace of mind for yourself… with an untouchable return on your nest egg.

In this report, you’ll learn about the three superbonds I promised you…

But first things first…

Let’s talk about asset allocation.

Most people are aware of buzzwords like “diversification.” But what exactly does that mean to you?

Well, it’s quite simple. Diversification means spreading out your risk across many different types of assets or investments.

In short, it means never put all your eggs in one basket. Try to spread them out over several baskets.

In the case of bond investing, the principle is the same. You should never put everything into a single bond. Even better, you should try to buy bonds in different industries with different risk profiles.

Here’s what we mean…

Let’s say you’ve just bought five bonds from five separate companies. It’s a good start that you’ve spread your money across more than one company.

And while investing in bonds is one of the safest investments on the planet, that doesn’t mean you should take unnecessary risks with your money.

Now that you understand the importance of diversification, let’s talk about credit ratings.

Credit ratings are a measure of a bond’s risk of defaulting. The lower the risk, the higher the rating. And vice versa.

Occasionally, a perfectly sound company might sport a relatively low credit rating. In fact, if you can sort the right ones out, you’ll find a treasure trove of high-yielding bonds backed by companies that are fully in the black.

On the other hand, some bonds have a low rating because they’re very risky – either the company’s fundamentals are a mess or the industry is getting clobbered with no end in sight, affecting the business’s bottom line.

Sorting between the chaff and the wheat takes some due diligence. But here’s the main takeaway…

Your bond portfolio should be spread out between bonds of different credit ratings to minimize the overall risk to your portfolio.

While bonds are very safe compared with other assets in the market, diversifying your bonds will make investing even safer and more profitable.

Now here are the three superbonds we recommend you buy right now.

3 Superbonds to Grow Your Nest Egg

Superbond No. 1: QEP Resources

This is an oil and gas producer with assets in all the major fracking and drilling areas in the U.S., and its numbers are fantastic…

Well, fantastic for an energy producer in a market disrupted by a global pandemic and an oil price war between Saudi Arabia and Russia.

Its debt is down 20% from 2018. It has $166 million in cash, and last year, it generated $567 million in cash flow.

In 2019, the company stopped the cash hemorrhage it experienced in 2018 and better prepared itself to move forward into 2020 as a leaner, more efficient company with a focus on financial discipline over production.

That’s good for us, as financial discipline means QEP will be better able to pay out the interest on its bonds.

In short, this is a fantastic bond for the yields it offers. Its BB- rating is well-deserved.

Buy the QEP Resources bond with a coupon of 5.375% that matures on 10/1/2022 at $600 or better. The CUSIP is 74733vab6, and it’s rated BB-.

At its current price of about $550, the bond has a current yield of 9.83% and a yield to maturity of 33.15%. If you buy and hold this one to maturity, you’ll enjoy a total return of 108.59%.

Superbond No. 2: Oasis Petroleum

Oasis Petroleum is an oil and gas exploration and production company. It has core positions in the two top oil basins in North America – the Williston Basin in North Dakota and Montana and the Delaware Basin in Texas.

The company controls more than 408,000 acres in the Williston Basin and nearly 25,000 acres in the Delaware Basin. Oasis has an estimated net proved reserves of approximately 286 million barrels of oil equivalent.

And, as with all oil and gas producers, high U.S. production and the flood of oil coming from Russia and Saudi Arabia has put pressure on its numbers. But don’t worry, there will be a market for the huge oil and gas resources Oasis controls.

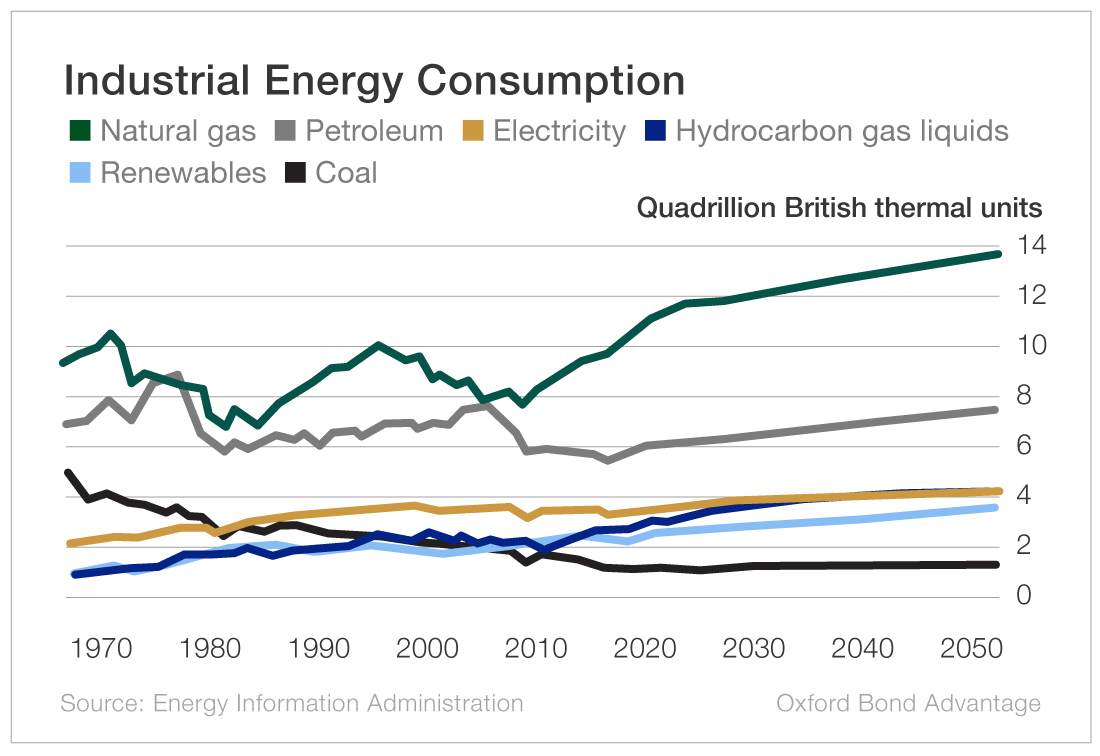

As you can see in the chart above, the projected increase in demand for natural gas and petroleum will keep Oasis busy for years to come. And remember, we are concerned only about the next few years until our bond matures.

Oasis has modest growth prospects over the next few years as it focuses on financial discipline, free cash flow generation (protected by hedges) and debt reduction. Management has stated that its top priority with free cash flow is debt repayment.

Despite the current low oil price environment, Oasis remains financially sound.

Long-term debt is high at $2.7 billion. But last year, the company generated $2.1 billion in revenue, and cash from operating activities was $893 million. Interest payments last year amounted to about $176 million.

It had $20 million in cash at year end, and it has a $575 million revolving line of credit available that it can expand to $775 million if needed.

This bond has been trading close to par for the past couple of years, reliably paying out interest to pleased investors.

But it has dropped to around $260 per bond as oil prices have tanked, creating an incredible buying opportunity.

It now offers a current yield of 26.15%. Its yield to maturity is 97.07%. If you buy now and hold to maturity, you can expect a total return of more than 334.09%.

Buy the Oasis Petroleum bond with a coupon of 6.875% that matures on 3/15/2022 at $280 or better. The CUSIP is 674215ag3, and it’s rated B+.

Again, with plays like this, please keep your positions small. Despite our confidence in this bond, it is still speculative.

Superbond No. 3: Superior Energy Services

Superior Energy Services currently provides oilfield services and equipment to oil and natural gas exploration and production companies in the United States and internationally.

What makes this bond play intriguing is that Superior is in the process of making a significant business transition that will reduce debt and improve cash flow.

At the end of 2019, Superior Energy Services combined its North American operations with Forbes Energy Services and created a new publicly traded company called Newco.

The transaction, which is expected to be complete within the next few weeks, has been unanimously approved by the board of directors of both companies. Once the merger goes through, both companies will have an approximate 50% interest in the company.

Newco is anticipated to be a leading supplier of production services like well services and fluid management, as well as completion services like wireline or coiled tubing. Newco gives Superior access to several major oil-producing regions, like the Permian Basin and the Rockies Basin.

This allows Superior to shift its focus to its real moneymaker – its offshore operations. Superior’s offshore and international operations provided nearly 75% of its revenue, according to a recent quarterly report.

In addition, the creation of Newco is significant to Superior bondholders…

Superior intends to reduce its debt by $250 million by issuing Newco bonds and using the proceeds to pay off Superior Energy bonds.

Management also plans to extend the maturity of up to another $250 million of Superior Energy notes.

CEO Dave Dunlap had this to say about the recent structural changes:

Superior Energy will now be focused on international and offshore markets… We believe this transaction, which reduces debt, and lowers interest costs, is a meaningful step towards our goal of improving our ability to generate free cash flow.

Currently, Superior has a total debt load of $1.28 billion, but it generated $146 million in operating cash flow last year and has $272 million in cash and equivalents. So debt servicing is manageable for the foreseeable future, and the Newco joint venture will be a further help in providing cash flow.

Freed from direct administration of many of its North American operations, the company is well-positioned to recover this year. And the price war between Saudi Arabia and Russia has created a perfect buying opportunity for us.

Buy the Superior Energy Services bond with a 7.75% coupon that matures on 9/15/2024 for $350 or better. The CUSIP is 78412fau8, and it’s rated B-.

The bond has been hovering between $560 and $650 for months, but now it’s only $325. At that price, it has a fantastic current yield of 23.67% and a yield to maturity of 42.47%. If you buy now and hold to maturity, this bond will deliver a total return of 315.10%.

Make Your Portfolio Super

Opportunities like these are exciting, especially in a market besieged by a pandemic and an election.

But here we’ve got predictable returns… protected by law.

To me, bond investing gives you the best of both worlds: consistent gains and very limited downside risk.

And with these superbonds in your portfolio, you can juice your portfolio’s growth just as simply.

Now, we do need to make one thing clear…

If you try to find these bonds and for some reason your online broker doesn’t have them in its inventory, you may have to contact the corporate bond desk and ask it to go out with an offer to get them.

Don’t worry. Folks do it all the time.

That said, you should expect the person on the phone at Fidelity, or wherever, to give you pushback about buying it.

In fact, most of these folks have little or no experience in bonds and will not understand what we are doing. Don’t give in. Make sure you demand to speak to someone competent who will execute the order as you wish.

You can always call the following brokers who are very familiar with our bonds and Oxford Bond Advantage.

- Ron Kramer: 917.887.2386 or 877.702.6637

- Ron McCoy: 407.614.2006 or 877.796.2269

- George Walters: 321.293.0284 or 800.329.1984

In Canada:

- Steven Osmak: 705.726.3453 or 800.669.7896

Another thing to keep in mind…

The expected total return on these will fluctuate, too, depending on when you get in on these bonds. So try to buy them around the prices we’ve mentioned above.

Don’t chase the price up on these. Just wait for them to come back down before buying so you can maximize your total return.

Remember, these are speculative bonds. But if they meet their obligations as required by law, the returns will be spectacular.