Retire Rich With Five Small Cap Dividend Stocks

Although these stocks are considered “small cap” based on their market capitalization…

There’s nothing small about the dividends they’re paying!

If you’re looking for additional ways to make more income in this economy and give yourself a great opportunity for big capital gains…

Then this report is for you.

You could end up collecting rising income for the rest of your life as these small caps become midcaps and, ultimately, large caps.

Here are my top five small cap dividend stocks.

UMH Properties

UMH Properties (NYSE: UMH) is a real estate investment trust (REIT) that owns and operates 136 manufactured home communities containing approximately 25,800 developed homesites.

UMH is the leading owner and operator of manufactured home communities. Its homes are sold and leased to residents in New Jersey, New York, Ohio, Pennsylvania, Tennessee, Indiana, Michigan, Maryland, Alabama, South Carolina and Georgia.

And business is booming!

UMH communities are seeing strong demand because the company provides high-quality and affordable housing.

At the end of fiscal year 2023, the company owned 9,743 rentals – an increase of 755 homes from year-end 2022.

In UMH’s 2023 annual report, management reported that rental home occupancy increased to 94.1%.

Because of the strong demand for UMH’s properties… the company can rent to tenants that have higher-quality financials. As a result, economy-related rent trouble has not been an issue.

Last year the UMH team generated an increase in same property income of 9% and same property net operating income of 13%.

Higher Earnings on the Horizon

UMH is perfectly positioned for future growth.

For years, the company’s business strategy has been to purchase underperforming properties and improve their output.

And now, thanks to the shaky economy, there’s a fire sale of manufactured homes taking place. UMH, looking longer term, is a willing buyer.

By the end of fiscal year 2023, UMH rented approximately 900 more homes than the previous year. UMH added 1,040 new rental homes to its portfolio last year, compared to only 392 units added in 2022. The latest additions bring the total number of its rental homes to 10,000, and increase of 10% from 2022.

UMH plans to grow its portfolio of rental homes by 800-1,000 units each year going forward.

The company also expects to increase its occupancy rate by upgrading the homes and selling them or by converting them to higher income rental units.

UMH has a strong track record of success in doing just that. Time and again, it has added value through acquisitions and expansions.

Another thing that will increase income is the company’s efforts to reduce its higher-cost and near-term debt.

And the company’s earnings power is already strong and growing…

UMH finished fiscal year 2023 with $220 million in revenue, an increase of 12.8% compared with $195 million in 2022.

And the results for the first quarter of 2024 produced solid numbers and gave UMH an excellent start to the year. The total income for the quarter ended March 31, 2024 was $57.7 million compared to $52.6 million year over year.

The second quarter of 2024 for UMH Properties proved to be stronger than the first. Total income for the quarter ending June 30, 2024 was reported at $60.3 million representing a 9% increase year over year.

UMH was also pleased to report that Normalized FFO for Q2 2024 increased to $.23 from $.21 last year, amounting to approximately a 10% increase.

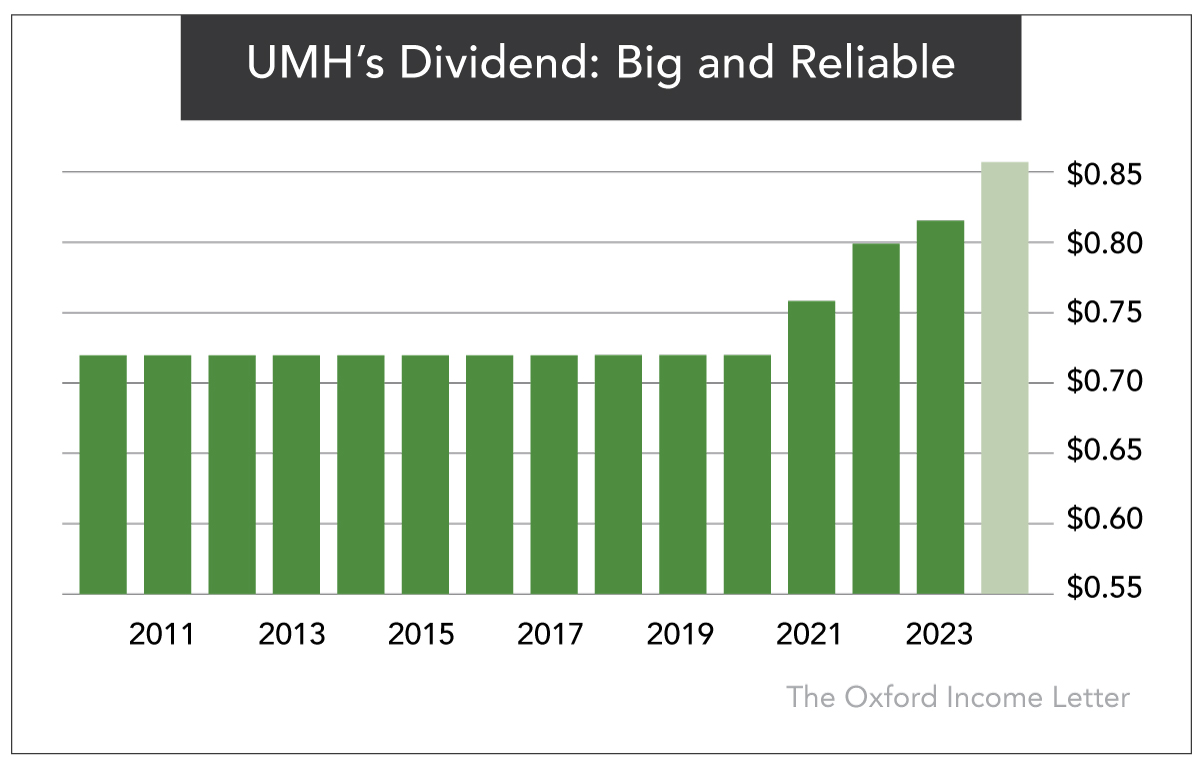

So far in 2024, UMH Properties, Inc. announced its board of directors approved a 4.9% increase in the quarterly common stock dividend to $0.215 per share. This represents an annual dividend of $0.86 per share, which comes out to a yield of 5.7%.

Furthermore, the dividend can have some tax advantages to it…

In past years, part or most of the dividend was considered a return of capital and, therefore, not taxable as dividend income. However, it will lower your cost basis, which means your capital gains will be higher when you sell it.

Action to Take: Buy UMH Properties (NYSE: UMH) at market. Place a 25% trailing stop below your entry price.

TFS Financial Corp.

TFS Financial Corp. (Nasdaq: TFSL) does business like a traditional retail bank – making money by collecting deposits and lending funds out to borrowers.

However, TFS Financial, which operates Third Federal Savings & Loan, is a very different type of bank. It’s a mutual holding company (MHC).

An MHC is similar to a credit union in that it’s owned by depositors and borrowers. MHCs are a true form of community bank. They are usually started to assist the local community with homeownership.

TFS Financial has over $17 billion in assets and approximately 1,000 employees. It lends in 25 states from offices in Ohio and Florida. The company’s headquarters is still in the same neighborhood in Cleveland where it began.

The CEO is Marc Stefanski, the son of the founders. He’s been at the helm since 1987.

The Dividend Keeps Improving

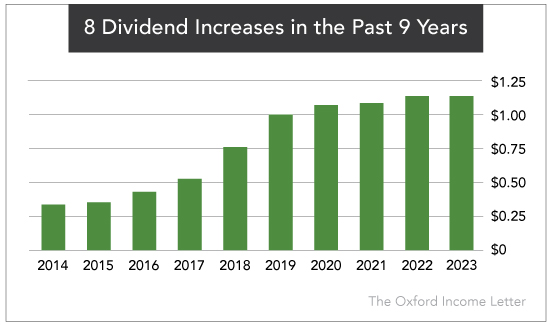

TFS Financial pays a $0.2825 per share quarterly dividend, or $1.13 annually, which comes out to a 8.68% yield. It has raised its dividend eight times since 2014.

In the fourth quarter of fiscal 2023 (the company’s fiscal year ended on September 30, 2023) it achieved 11% growth in net income compared with the same quarter in 2022. Net income for fiscal 2023 was $75.3 million, compared with net income of $74.5 million in fiscal 2022.

In its fiscal 2023, the company added $1.86 billion worth of new residential mortgage loans and increased total deposits by $381 million. Total assets increased by $1.13 billion to $16.92 billion. Cash and cash equivalents increased $97.1 million, or 26%, to $466.7 million.

With TFS Financial’s increase in loans, total assets and net income in 2023, I expect it to continue hiking its dividend for the foreseeable future.

And its fiscal year 2024 is off to a good start. First quarter ending December 31, 2023 resulted in an 18% increase in cash and cash equivalents. And another 8% increase for the same metric in Q2 of 2024. The third quarter of 2024 ending June 30, 2024 decreased cash and cash equivalents by less than 1% due to normal fluctuations. The first nine months of fiscal year 2024 resulted in a $5.7 million increase in net income over the first nine months of the previous fiscal year.

This company is a stable, safe and high-yielding community bank – exactly the kind of company I love to add to our portfolio.

Action to Take: Buy TFS Financial Corp. (Nasdaq: TFSL) at market. Place a 25% trailing stop below your entry price.

Innovative Industrial Properties

Headquartered in San Diego, Innovative Industrial Properties (NYSE: IIPR) has found a very lucrative niche and offers a great combination of growth and income in a brand-new industry.

The company is the leading provider of real estate capital for the medical cannabis industry.

Legal sales of cannabis in the U.S. is expected to reach $32.1 billion in 2024 – an increase of approximately 90% over 2020’s total of $17.5 billion. And sales are expected to grow to more than $58 billion by 2030.

That’s an enormous opportunity…

All this coming demand means the supply of cannabis will need to rapidly increase. And hundreds of startup companies are jumping at the opportunity to provide it.

The essential component all these companies need is facilities to grow the cannabis…

Innovative Industrial Properties plays a crucial role in an industry lacking access to growth capital. In essence, the company acts as a commercial bank and landlord to state-licensed medical-use cannabis growers.

Innovative Industrial’s unique strategy is to buy cannabis companies’ land and grow operations and then lease the space back to those companies on a long-term basis. Those leases typically extend beyond 15 years, and Innovative Industrial usually builds in yearly rent hikes.

Innovative Industrial owns 108 properties in 19 states. Of its total 9 million square feet of rentable space, 95.6% is leased with an average term of 14.9 years.

It’s a win-win arrangement…

By selling the real estate to Innovative Industrial and then leasing it back, growers can redeploy the proceeds into their company’s core operations.

Instead of having hundreds of millions of dollars locked up in real estate purchases… Innovative Industrial’s clients can direct their capital to growing cannabis.

The cannabis growers love it… and so does Innovative Industrial.

Growing Like a Weed

When it had its initial public offering in December 2016, Innovative Industrial had one property under contract. Now it has 108.

As of the end of the second quarter of 2024, Innovative Industrial had $210.9 million in cash and short-term investments to snap up more properties. The firm has been able to raise capital on very favorable terms thanks to its excellent cash flow.

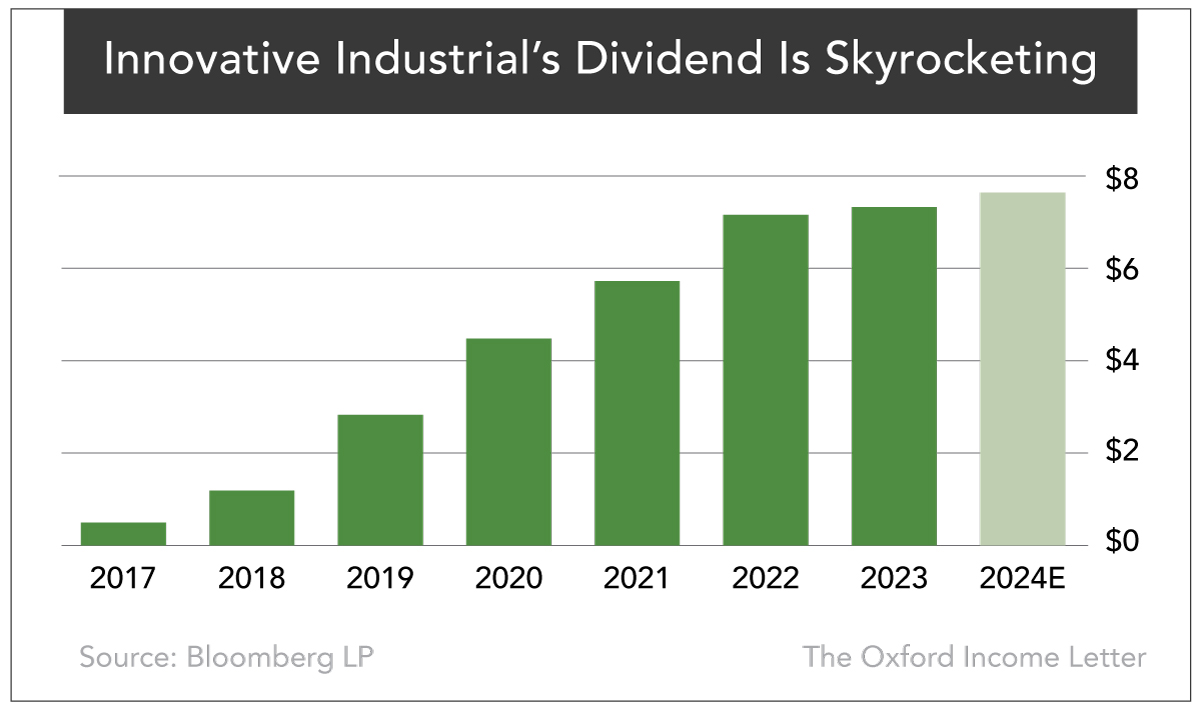

Going forward, the $7.60 annualized dividend creates a current yield of 5.68%.

And payouts are rising at a rapid rate. The $7.60 per share annualized dividend for 2024 is the result of a second quarter dividend increase of 4.4%. This increase continues the company’s track record of increasing the dividend every year since its inception.

A Bright Future Ahead

Since Innovative Industrial sees such a high volume of appealing properties, it can afford to be selective.

And this management team has a proven record of not overpaying for desired properties. The team scrutinizes every potential deal to ensure it will produce those very impressive dividend yields.

No facility is bought unless it is purchased from a cannabis grower ready, willing and able to lease it back… immediately.

Innovative Industrial keeps on growing… For the first quarter of 2024, the company generated total revenues of $75.5 million. Net income in the first quarter was reported at $39.1 million. And second quarter 2024 financials were even stronger. Total revenue for Q2 2024 were reported as $79.8 million, a 4.4% increase year over year. These numbers show a solid start to the year. And over the past 5 years, Innovative Industrial Properties revenue has grown at an outstanding compound annual rate (CAGR) of 66.85%

More U.S. states continue to propose, or have passed, legislation to legalize cannabis.

That means there’s still plenty of upside here… for the stock and the dividend.

Action to Take: Buy Innovative Industrial Properties (NYSE: IIPR) at market. Place a 25% trailing stop below your entry price.

Upbound Group

You may not be familiar with this name, but you know this company. Upbound Group (Nasdaq: UPBD) was known as Rent-A-Center before changing its name in February 2023.

And to make things even more confusing, Upbound has operations under an assortment of names, including Rent-A-Center, Get It Now! and Home Choice,.

Headquartered in Plano, Texas, Upbound has more than 2,400 stores across the country and is one of the leading rental and lease-to-own providers of durable household goods in the nation.

And no matter the name, the business strategy is the same. The company offers a rent-to-own model to its customers for household items, including furniture, appliances and electronics.

If customers don’t have good enough credit to borrow through traditional means, the company gladly provides loans.

It’s a good business. Margins are high, and there’s a growing customer base.

But what’s most appealing about buying shares right now is that the company is in the midst of a significant turnaround.

Expenses have increased as Upbound continues transitioning more of its business operations to an omni-channel platform.

A Big Partner

Upbound made a big move in December 2020 to accelerate its turnaround when it acquired Acima Holdings for $1.3 billion. Salt Lake City, Utah-based Acima is a leading provider of virtual lease-to-own (LTO) solutions.

The acquisition vastly expanded Upbound’s virtual LTO product offerings and greatly broadened its retail partners. Acima’s proprietary digital platform and large online presence gives Upbound a much bigger footprint in e-commerce sales.

Looking ahead, Upbound estimates that 50% of its 2024 revenue will be from e-commerce sales compared with just 12% four years ago.

The management team has made the right moves and has done a good job of getting the company back on track after being derailed by the COVID-19 pandemic.

Management is working to cut millions of dollars in overhead, eliminating unprofitable locations, rebranding critical stores, adding to its product offerings, growing its e-commerce business and shoring up its balance sheet.

It’s paying off… The past several quarters have exceeded analysts’ forecasts. The customer base is expanding, there’s strong demand for its products and the company is generating higher profits per customer.

For the full year 2023 Upbound reached a significant milestone of $4 billion in revenue with over $1 billion attributed to Q4 of 2023 alone. So Upbound seems to be making all the right moves during its turnaround.

And you can collect a nice dividend while you wait for the company’s turnaround to be recognized on Wall Street.

For 2024, the quarterly dividend was increased 9% to $0.37, or $1.48 annually, for a 5.46% dividend yield.

The company is also repurchasing shares. This should further enhance shareholder value.

Clearly, things are improving. But Wall Street hasn’t caught on yet… The stock is trading for a forward price-to-earnings ratio of 6.65 and an extremely low price-to-sales ratio of 0.33.

That gives us strong upside potential from today’s price and a nice yield to boot.

Action to Take: Buy Upbound Group (Nasdaq: UPBD) at market. Place a 25% trailing stop below your entry price.

Evercore Inc.

Evercore Inc. (NYSE: EVR) is an independent investment banking advisory firm in the United States, Europe and Latin America, among other places. It operates through two segments, Investment Banking and Investment Management, with clients in more than 50 countries.

The company has shown it can thrive regardless of market conditions or the state of the economy.

Established in 1995, Evercore has quickly established itself as one of the premier global investment advisory banking firms.

Assets under management have grown at an annual rate of 15% since 2010.

In an October 29 news release, Evercore ISI announced it was recognized as the #1 firm in U.S. equity research for the third consecutive year by Extel’s All-America Equity Research survey.

The company has been profitable every year since its initial public offering in 2006.

A Big Boost in Business

Evercore is taking careful steps to grow the business over the long term. It’s reducing head count, selling unprofitable subsidiaries, paring back its risky lending, and focusing on collecting fees and improving investment returns.

Those moves are paying off…

Evercore finished fiscal year 2023 with $2.4 billion in net revenue. With its fourth quarter revenue the strongest in the past five years.

The early weeks of 2024, continued with strong momentum as Evercore reported net revenues of $580.8 million in the first quarter.

Evercore also advised on five of the 15 largest global transactions, including:

- General Electric on its $37 billion spin-off of GE Vernova

- Synopsys on its acquisition of Ansys for $35 billion

- Clayton Dubilier & Rice on its acquisition alongside Stone Point Capital, of Truist Insurance from Truist Financial for $15.5 billion

- Global Infrastructure Partners on its sale to BlackRock for $12.5 billion

- Chesapeake Energy on its combination with Southwestern Energy for $11.3 billion

And keep in mind, investment banks play an important role when times are tough.

The strong start to 2024 paid off in the second quarter as net revenue was reported at $689.2 million. And the momentum continued through the third quarter of 2024 as Evercore grew its net revenue to $734.2 million. These metrics equate to $2 billion in net revenue for the first 9 months of 2024 and a 22% increase year over year.

Evercore is getting strong contributions across all services globally, including Mergers & Acquisitions, Capital Markets Advisory, and Strategic, Defense & Shareholder Advisory. Activity levels remain high, and backlogs are strong.

Don’t Wait for the All-Clear Signal

In the first quarter of 2024, Evercore increased its quarterly dividend by 5% to $0.80 per share.

Its annual dividend is now $3.20 for a yield of 1.21%. (The dividend yield is low only because the stock price has soared over the past 12 months, more than doubling the performance of the S&P 500.)

Evercore is thriving despite the difficult circumstances created by a weak global economy and higher inflation. I expect business to remain strong and then further expand when a more normal business climate is achieved.

The company has raised its dividend every year for the past 13 years.

Evercore is widely considered the top boutique investment bank. It generates more revenue than any of its similar-sized peers and even generates more investment banking revenue than most of its larger peers.

Evercore’s diversified business will allow it to pay you a big dividend regardless of whether the economy booms or busts.

And the company is flying under Wall Street’s radar.

While Wall Street focuses on the JPMorgans and Goldman Sachs of the world… Evercore is quietly attracting additional business and gaining market share.

In a nutshell, Evercore is a great little investment bank that’s outperforming the competition.

Action to Take: Buy Evercore Inc. (NYSE: EVR) at market. Place a 25% trailing stop below your entry price.

Retire Worry-Free

And remember, with dividend-paying companies, you get paid whether their stock goes down, up or sideways.

When you’re collecting regular, predictable income, it’s much easier to ride out stock market volatility. Not only that, but you can expect some of these companies to increase their payouts year after year.

This could be your chance to retire rich without lifting a finger…

Let the magic of compound interest work for you by collecting these massive dividend checks for years to come.