How to Achieve a Seven-Figure Retirement Account…

Even if You Think It’s Too Late

Building up your retirement account – and starting early in particular – is one of the most important things you can do to create a nice-sized nest egg for your golden years.

Each type of retirement account discussed below grows tax-free, giving you a huge opportunity to let the power of compounding do its magic.

Unfortunately, the percentage of people contributing to any type of retirement account is in the low double-digits. And the number of people contributing the maximum amount is in the low single-digits.

Before we get into some strategies that will help you accelerate your savings, let’s cover the three basic types of retirement accounts. After reading over the descriptions below, review the strategies and decide which type of account (or accounts) works best for you.

Individual Retirement Account

A traditional Individual Retirement Account – or simply IRA – is a tax-advantaged account that the government created specifically to help people save for retirement. When used properly, IRAs can save you thousands of dollars in taxes while creating thousands in savings.

Taxpayers are allowed to contribute up to 100% of their earned income up to a set limit per year. Currently that limit is $6,000 for anyone under the age of 50; and for anyone older, it is $7,000. The reason for that higher limit for the “older” crowd is to encourage catch-up saving for folks who put it off. And to account for inflation, these limits are raised over time.

Traditional IRAs let you lower your current taxable income. For example, if you made $90,000 last year (and weren’t covered by a retirement plan at work) and contributed $6,000, your taxable income would drop to $84,000. That means a person in the 32% tax bracket would save $1,920 in taxes. Even more importantly, money put into an IRA grows tax-free until it’s withdrawn.

Now, to start withdrawing from your IRA, you must wait until you’re aged 59 1/2 and your account is at least five years old to avoid a 10% penalty. And once you start taking distributions, you have to pay income tax on them.

Then there’s required distributions. After turning 70, you must start taking some money out. IRS.gov provides a worksheet online to determine the amount. In retirement, most folks don’t receive work income anymore. So they’re in a lower tax bracket, and the required distributions are taxed as such.

The distinctive advantage of a traditional IRA is the upfront tax deduction received on contributions. If you properly plan your income and cash flow, you’ll save thousands from Uncle Sam while building a large nest egg for yourself.

Roth IRAs

Roth IRAs are similar to traditional IRAs. But they don’t lower your current taxes. You don’t receive any tax benefits for making contributions.

However, you aren’t taxed on withdrawals when you take the money out during retirement. Taxes have already been paid on what you contributed, so the government doesn’t tax you again… or on any of the earnings.

If you’re in a lower tax bracket than you expect to be in the future, it’s best to contribute to a Roth IRA. Once again though, you can only contribute up to $6,000 per year (or $7,000 if older than 50). Moreover, that limit covers both kinds of IRA. So if you’re 49 years old, you can contribute $3,000 to a Roth and $3,000 to a traditional IRA. But that’s it.

With that said, one benefit Roths have is that they don’t involve any required minimum distributions. You can keep the money in the account for as long as you like and even leave it to family members in your will.

Plus, you can withdraw your contributions on a tax-free, penalty-free basis at any time for any reason. Though that rule doesn’t apply to any earnings or interest you’ve earned on it. In order to withdraw those tax- and penalty-free, you have to be older than 59 ½ and your initial contributions must have been made at least five years prior.

With all that said, both the traditional and Roth IRAs are easy to set up. Every bank, brokerage firm and mutual fund company offers them, with the online setup process taking less than 20 minutes. The distinctive advantage of a Roth IRA is that both your contributions and any earnings are tax-free on withdrawal (assuming you meet some minimum withdrawal requirements). With a traditional IRA, both your contributions and any earnings are taxed at withdrawal.

401(k) Accounts

401(k)s are like IRAs except that employers offer them, and they have a few different limits and rules. For one thing, folks younger than 50 can put in up to $19,000 this year. For those older, that limit jumps to $25,000.

These contributions are made on a pre-tax basis by your employer based on your directions. Because they’re pre-tax, they directly lower your adjusted gross income (AGI) and therefore lower your taxes, too. Because of the larger amounts you can put in… the tax savings can be considerable.

Withdrawals from a 401(k) are treated similarly to those from a traditional IRA and taxed when they’re taken out.

Once again, these accounts are easy to set up. Usually, it just involves reaching out to your human resources department.

How to Achieve a Seven-Figure Retirement Account

According to the Employee Benefit Research Institute, there are two key characteristics to achieving a seven-figure retirement account. A high percentage of million-dollar savers had constant participation and high contribution rates.

The EBRI also reported that one of the biggest mistakes people make when saving for retirement is that they can’t or don’t take full advantage of the benefits offered by the various retirement accounts at their disposal.

Making the most of these resources will provide you with your best chance of amassing a sizable retirement nest egg. However, how you go about investing in these accounts is very important. That’s why we’re also giving you some outstanding strategies to help you reach your goals.

A $2,220 Birthday Present From the IRS

Found in Section 408 of the tax code, this is great for anyone over 50…

If you’re older than 50, you can make catch-up contributions in your 401(k), 403(b) or IRA account. These payments can save you up to $2,220 every year at tax time.

Here’s how you can get the biggest benefit… use these catch-ups to max out your 401(k) contributions.

Anyone 50 or older can add an extra $6,000 to his or her 401(k) account (for a total of $25,000), which lowers your gross income and reduces your tax liability. As previously stated, if you’re under 50, the most you can annually contribute to your 401(k) is $19,000.

(A 403(b) also allows an additional $6,000, while a traditional IRA or Roth allows an extra $1,000 if you’re age 50 or older).

A worker in his 50s or 60s who falls in the 37% tax bracket and maxes out his employer-sponsored retirement account could reduce his tax bill by $2,220, since income tax won’t be due on the contributions until the money is withdrawn.

The $2,000 Saver’s Rebate

This one’s a bit of a shocker.

In 2002, legislators were looking for ways to encourage Americans to save more money. And with good reason…

The median American household has just $11,700 in savings.

So Congress passed a law allowing citizens to collect a cash rebate each year if they simply socked a little money away for a rainy day. Lawmakers made the program permanent in 2006.

Many people who elected to save money last year are now eligible to receive up to a $2,000 cash rebate for doing so.

To join their ranks, just fill out a Retirement Savings Contributions Credit, or Saver’s Credit, form along with your taxes. These are available to anyone making contributions to an IRA or employer-sponsored retirement plan.

The credit amount is 50%, 20% or 10% of your retirement plan or IRA contributions up to $2,000 ($4,000 if married filing jointly), depending on your AGI (as reported on your Form 1040 or 1040A). Go to www.irs.gov to see what the current limits are.

How to Add $155,000 to Your Retirement Account

What we’re talking about here is reducing the cost of your 401(k).

Retirement plan providers have been overcharging investors for decades, creating a huge drag on returns. As a result, many 401(k) plans are much too expensive…

The average investor’s annual charge is 0.83% of assets. In small plans, it’s often much more: as high as 3%. In large plans, it’s a little less.

There can also be additional “wrap fees” of up to 1% of your assets. And that’s to say nothing about the mutual funds inside 401(k)s. Many plans only offer funds that charge fees of 1.5% or more – far higher than the median 0.77% for stock funds.

Consider this jarring figure from think tank Demos: An ordinary American household with two working adults will cough up almost $155,000 in 401(k) fees over a lifetime.

Worse still is that a stunning 70% of those polled in a recent AARP survey said they didn’t think they were being charged anything!

Fortunately, that confusion is about to change.

Thanks to a new rule issued by the Labor Department, investors will start receiving reports that detail all the fees their providers are charging. Every investor must get a report.

It’s a landmark moment that should go a long way toward maximizing regular savers’ nest eggs.

Be sure to check and see what you’re paying in fees. If they’re not reasonable, make changes to your plan. And if needed, put pressure on your employer to offer additional investment options that charge less.

The Instant Return… Instantly Get a 100% Return on Your 401(k) Investment Every Year

This is the easiest money you’ll ever make.

Find out if your employer matches contributions to your retirement account…

Many offer an immediate 401(k) matching contribution up to a certain percentage of your pay.

Generally, they’ll match anywhere from 3% to 6% of an employee’s pay up to a certain dollar limit or percentage of their pay (e.g., 50% to 100% of employee contributions up to 3% of their salary).

According to U.S. News Money, a 30-year-old employee earning a $50,000 salary who saves $5,000 per year and gets a 3% 401(k) match will accumulate $747,662 by age 65, assuming 6% annual investment returns. An employee who saves the same amount without getting an employer match would retire with just $575,125.

That’s a $172,537 difference.

It seems obvious that employer contributions make it much easier to amass a bigger nest egg… but it’s mind-boggling how many people don’t take full advantage of this.

Your employer match is an immediate 100% return on your investment. You automatically make 100% on those matched dollars before you’ve even invested the money. That’s why it’s critical you contribute up to the amount your employer will match (at the very least).

You also earn a tax-free return on those funds in addition to what you’ve contributed. So you’re crazy if you don’t take advantage of this. It’s the simplest, most reliable way you can find to double your money…

Make sure you contribute enough in your 401(k) to receive the maximum contribution from your employer. This is free money to you… and it will make a huge difference in the long run.

How to Keep the Government from Taking a 20% Cut of Your 401(k)

Here’s the right way to do a retirement plan rollover…

The whole point of a 401(k) is to save tax-free money for retirement. So once you’ve accumulated a nice nest egg, don’t let this mistake happen.

It happens too often already, and it can take a big bite out of your savings.

I’m talking about a particular decision involved in transferring your retirement savings out of your 401(k). If you ever do this… be sure you do a direct rollover.

In other words, ask your former employer to directly transfer the money to an IRA or different 401(k).

If it makes out the check to you, 20% of your account balance will be withheld for income tax. You’ll then have 60 days to deposit the cash – including the amount withheld – in a new tax-deferred retirement account.

If you miss the deadline, Uncle Sam keeps the 20% and you become responsible for any additional income tax due.

If you’re under the age of 55, you’ll also have to pay a 10% early withdrawal penalty on any amount not deposited in a new retirement account.

Bottom line: If you’re going to roll over an old 401(k), make sure you always have the check made payable to the new custodian.

One Simple Mistake Retirees Make that Accidentally Doubles Their Income Tax-rate…

This strategy revolves around when, how much and from where you withdraw money in your retirement accounts.

Retirees need to carefully weigh their retirement account withdrawal options when it comes time to take money out. That’s because the IRS taxes Social Security benefits beginning at very low income levels.

If combined income (AGI + nontaxable interest + ½ of your Social Security benefits) is between $25,000 and $34,000 for a single individual or $32,000 and $44,000 for a married couple, 50% of their Social Security benefits are taxed. Combined income above these maximum amounts results in up to 85% taxation.

So figuring out where you withdraw money from will make a big difference in understanding your personal tax bracket and Social Security tax.

Here’s a great way to reduce your tax bracket and eliminate, or lower, your social security taxes…

First, hold off collecting your Social Security payments until age 70. That will also ensure the maximum Social Security benefit. Then, when you retire (say at age 66), use your traditional IRA as the main source of cash.

Yes, you’ll have to pay tax on those withdrawals, but you’ll eventually have to do that anyway. And since your income won’t be simultaneously inflated by Social Security payments, your withdrawals should be taxed at a lower rate.

Once you reach age 70 and start collecting Social Security, you can reduce the amount being withdrawn from your traditional IRA and start tapping into your Roth, where distributions are tax-free.

However, keep in mind that when you reach age 70 ½, you have to start making required minimum distributions from your traditional IRA. So be sure to figure that into your calculations.

Why You Should NEVER Invest in Your IRA/401(k) Right Before the April 15 Deadline…

The saying “time is money” definitely applies to your retirement accounts. It’s all about the power of compounding.

If you make your IRA contribution on the first day possible (New Year’s Day of the tax year) rather than the last (April 15 of the following year), your money will have an extra 15 ½ months to grow tax-deferred. Over a decade, that just about gives you an extra 13 years of compounded growth. And over three decades, it’s nearly an extra 39 years.

Here’s what it would mean for two investors. Tom and Jerry both contribute $5,000 and get the same return of 9%… the one difference being that Jerry makes his full contribution on January 1 while Tom waits until April 15 of the following year.

After 30 years of last-minute $5,000 IRA contributions, Tom will have some $687,000, but Jerry will have about $762,000, a $75,000 difference. Over 40 years, the difference increases further, with Jerry accumulating $1,889,797 versus Tom’s $1,696,998.

The moral of the story: The sooner investors make contributions, the better off they’ll be.

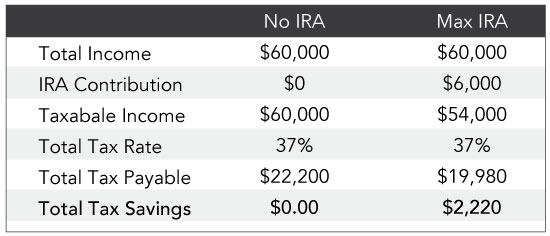

Rake in 37% Returns Every 12 Months With Practically No Risk!

There are few layups in the investment world. So when you see one, YOU MUST TAKE IT.

This one involves a guaranteed instant 37% return with no risk. But you’d be surprised how many people overlook or underfund this opportunity.

Here’s the “secret”: You must always – with NO EXCEPTIONS – fund your IRA to the maximum allowable.

To see why, let’s do the math together.

Currently, a traditional IRA allows for a maximum of $6,000 ($7,000 if you’re 50 or older) to be deposited each year. Let’s assume you’re in the 32% federal tax bracket and your state has a 5% income tax – for a combined income tax rate of 37%.

If your annual taxable income is $60,000, your tax on this would be $22,200 ($60,000 x 37%). But if you put the full $6,000 into an IRA, that figure drops to $54,000 and your tax falls by $2,220 to $19,980.

That’s EXACTLY like making 37% risk-free ($2,220 ÷ by $6,000 = 37%).

How to Take Money out of Your Retirement Plan

and Not Pay a Single Cent in Taxes

While it may sound too good to be true, there’s more than one way to withdraw money from your retirement plan without incurring taxes or penalties.

The first and most obvious way is to open a Roth IRA. As mentioned earlier, you may withdraw your contributions to a Roth on a tax-free, penalty-free, basis at any time for any reason.

But there’s one more tax-free withdrawal possibility…

You can also get money out of your Roth under a first-time homebuyer’s clause. By meeting some very basic criteria, you can withdraw up to $10,000 from the account just as long as it’s been open for five years and the funds are used directly toward acquiring the home (e.g., down payment, closing costs, etc.).

In this report we’ve given you the techniques and strategies that everyday people use to build million-dollar fortunes… even if they aren’t the top income earners in America. Use these powerful and actionable wealth-building and cash-saving secrets to create your own seven figure retirement account.