The Next 5 Profit Storms Hitting Wall Street

If you’ve ever been unlucky enough to find yourself in the eye of a hurricane, you’ve experienced Mother Nature’s awesome power firsthand.

At first, the ocean is so calm and flat that it almost seems eerie. But then the storm rolls in with torrential rains and pounding winds so powerful it can change the entire coastline. And in some cases, storms have even been known to split islands in two!

I’ve found that the same phenomenon occurs in the stock market. Seemingly calm and quiet stocks suddenly ramp up into cash-gushing storms!

The same types of natural forces that create Category 5 hurricanes in our oceans happen on Wall Street all the time.

And I’ve found a way to forecast them.

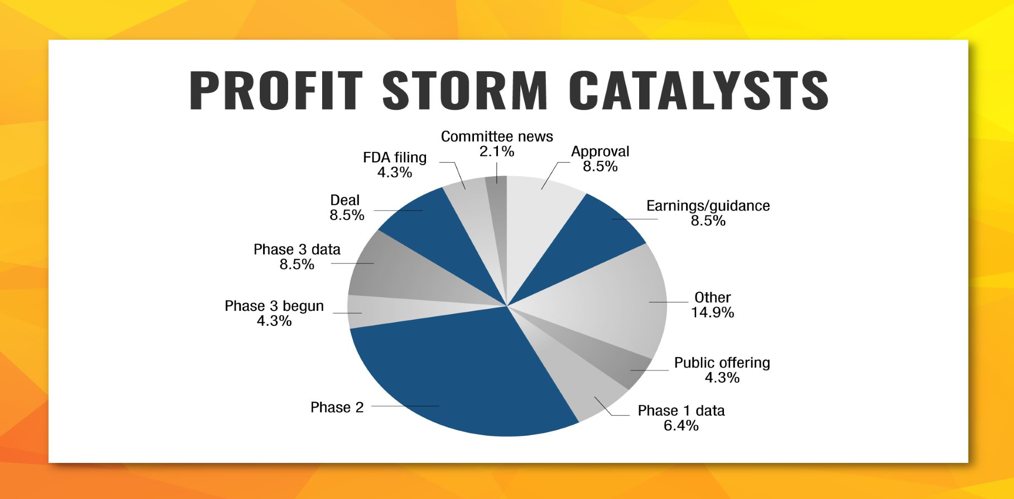

I grade these profit phenomena from Category 1 to Category 5 based on their catalysts.

- CAT-1: Phase 1 Data

This is the earliest phase of testing new medicines on human subjects – positive results also ignite CAT-1 Profit Storms. - CAT-2: Phase 2 Data

This is when companies begin to focus on the safety and effectiveness of their medicines as they get refined. It also creates a CAT-2 Profit Storm. This is my bread and butter, and, as you can see in the chart below, it is the most common trigger that sends a stock soaring. - CAT-3: Phase 3

This is when clinical trials begin and when these revolutionary treatments begin entering select treatment programs. Phase 3 creates a powerful CAT-3 Profit Storm. - CAT-4 FDA Filing or Approval

As you may have guessed, this is when the medicine becomes readily available and you start seeing commercials for it on TV. The Food and Drug Administration (FDA) approval triggers CAT-4 Profit Storms, but they are very difficult to predict without a system like mine. - CAT-5: Takeover Deal

This is like throwing gasoline on a fire and can create a 100-year storm in the market, leading you to CAT-5 profits!

Using mathematical precision, I can track stocks that are set to go from a blip on the ticker tape to full-force CAT-5 profits in just days… sometimes in even as little as 24 hours.

It’s one of the most powerful moneymaking forces I’ve ever seen in the stock market.

Here are the five Profit Storms I’m tracking right now, including a CAT-5!

CAT-1 Profit Storm Pick: Ultragenyx Pharmaceutical

A RARE Gene Therapy Play With Two Upcoming Catalysts

I’m a big fan of gene therapy as I believe it has the potential to be a game changer in medicine. It already is for the diseases it treats. As treatments for more diseases are approved, we will begin to see horrible diseases not just treated but cured.

Ultragenyx Pharmaceutical (Nasdaq: RARE) uses various gene therapy techniques to treat rare diseases.

It has two approved products. Crysvita treats X-linked hypophosphatemia, which is also known as rickets. The disease causes soft and malformed bones as well as breathing difficulties and weakness.

Mepsevii is used for MPS VII, an enzyme deficiency that results in short stature, joint stiffness, enlarged liver and spleen, hearing loss, and cataracts.

In the first quarter, Ultragenyx generated $36 million in revenue, double the amount a year ago. Management expects 2020 revenue to be between $120 million and $140 million.

It has several drugs in the pipeline.

- Burosumab in tumor-induced osteomalacia, which causes benign tumors that lead to bone pain, muscle weakness, fatigue and fractures. It affects between 2,000 and 4,000 patients worldwide.

- UX007 in long-chain fatty acid oxidation disorders. These are a type of genetic disorder in which long-chain fatty acids are unable to be converted into energy. It can lead to severe depletion of glucose and cause liver damage, heart disease and early death. The only current treatment for the 8,000 to 14,000 patients around the world with the disease is using diet to try to control the symptoms.

- DTX401 to treat glycogen storage disease. Patients with this accumulate glycogen in organs, which can result in kidney failure and cause death in children and infants. There are no treatments for the 6,000 patients who suffer from it. In recently released data, all patients in one cohort reported increased time to lowered blood sugar.

- DTX301 is being studied in ornithine transcarbamylase (OTC) deficiency. In a Phase 1/2 study, six out of nine patients responded to therapy. One patient showed a 188% increase in urea from 25% of normal to 73% of normal. Two patients have shown durable responses of two years and 1.5 years with urea levels above 100% of normal. OTC deficiency is caused by a genetic defect in a liver enzyme that is responsible for detoxification of ammonia. Normally, excess ammonia is converted to urea. In OTC patients, it is not. The buildup of ammonia causes neurological deficits and can be fatal.

Catalysts

The company has two major catalysts coming up this summer.

In just a few weeks, on June 18, the FDA will rule on whether burosumab in tumor-induced osteomalacia will be approved. This is an ultra-rare disease and would likely command a very high price per dose.

Then on July 30, the company will find out if UX007 will get the green light from the FDA.

There could be additional data on the other drugs by the end of the year, but we’ll especially be paying attention to the two PDUFA dates coming up over the next two months. A PDUFA date is the date by which the FDA must make its approval decision on a drug.

Lightning Strike

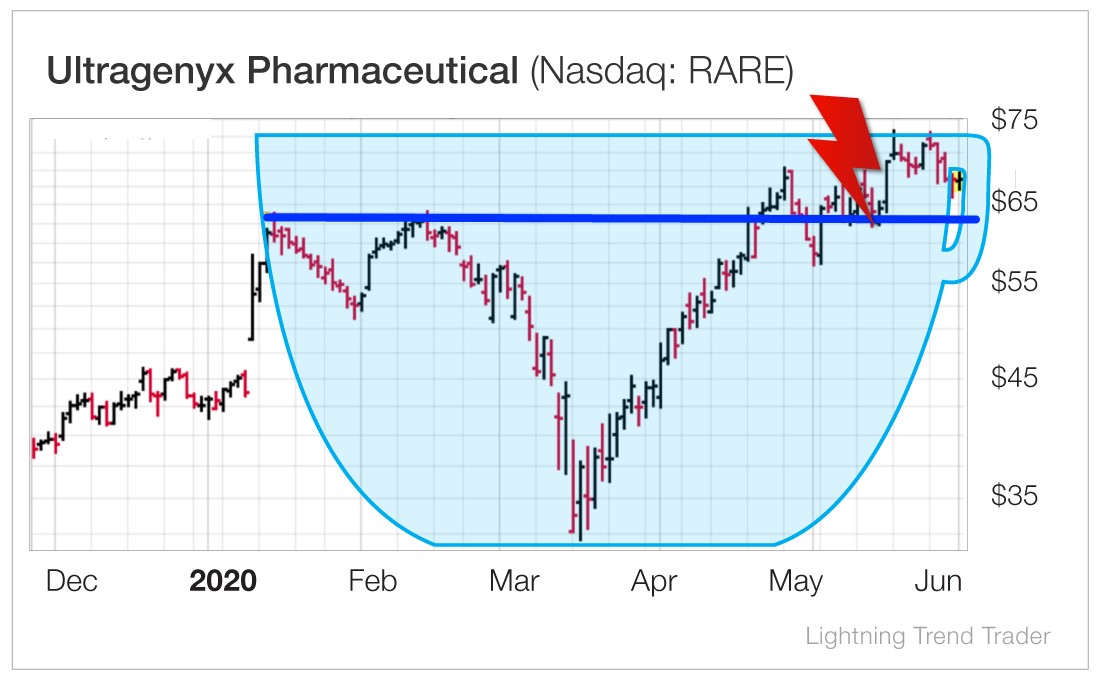

I love Ultragenyx’s chart right here.

It has formed what is known as a cup-and-handle formation. This pattern is very bullish.

It has formed what is known as a cup-and-handle formation. This pattern is very bullish.

You can see the stock broke out above previous resistance around $65. Once it breaks above the next resistance level of $75, it should really get moving. On a purely technical basis, the stock should go to about $96. However, approval by the FDA or other positive developments could send it even higher.

Let’s get in on one of my favorite gene therapy companies, before the FDA decisions.

Action to Take: Buy Ultragenyx Pharmaceutical (Nasdaq: RARE) at market. Place a 25% trailing stop to protect your principal and profits.

CAT-2 Profit Storm Pick: Fate Therapeutics

CAR T-cell therapy is a way to fight cancer by taking a patient’s T-cells, reprogramming them to fight specific cancers and then reintroducing them into the body. It has shown great promise to fight certain kinds of blood cancers, but it also causes severe and sometimes fatal side effects.

This company uses a therapy that is similar to CAR T-cell therapy in that a patient receives cancer-fighting cells, but these cells are stem cells that have been reengineered into specific types of cells to attack the cancer. The difference is that this therapy would be “off the shelf,” meaning it wouldn’t be dependent on extracting the patient’s own cells. And in early trials, it appears to be much safer, not causing the cytokine storms associated with CAR T-cell therapy. A cytokine storm is the body’s release of too many immune system cells. Cytokine storms are also a harmful effect of COVID-19.

As a result of the new therapy being “off the shelf,” the process would be much cheaper than the current $1.5 million CAR T-cell treatments and can be administered much faster.

Fate Therapeutics (Nasdaq: FATE) is an early-stage company that has several drugs in development that use iPSC (induced pluripotent stem cells) technology to treat cancer.

The Food and Drug Administration (FDA) recently cleared Fate’s drug FT538 to begin a Phase 1 trial that will be the first to edit the stem cells using CRISPR. The plan is to treat 105 patients with acute myeloid leukemia (AML) with FT538 alone and in combination with daratumumab.

It has several drugs in early development.

FT596 is in Phase 1 trials for advanced diffuse B-cell lymphoma. It is the first immunocellular therapy with three ways of fighting cancer.

FT500 is in Phase 1 trials for advanced solid tumors. So far, three patients have been dosed. There have been no dose-limiting toxicities. Fifteen patients will be treated in the trial.

And FT516 is also being studied in a Phase 1 trial of AML. In December, it showed that after 42 days, one patient had no evidence of leukemia. It is also being tested in up to 20 high-risk COVID-19 patients in a study conducted by the University of Minnesota. The University of Minnesota is paying for the trial. And it’s an accelerated dose escalation study, so if it shows that it’s safe, Fate can use the data in its own work.

The company has various collaborations, including partnerships with Memorial Sloan Kettering Cancer Center, Oslo University Hospital and Juno Therapeutics.

In April, it closed a deal with Janssen, which is part of Johnson & Johnson (NYSE: JNJ), that paid Fate $50 million upfront plus a $50 million equity investment at $31 a share and up to $3 billion in developmental milestones and royalty payments.

The company has $219 million in cash, so there is no need to raise money anytime soon.

Catalysts

Fate is soon expected to provide an update on its Phase 2 trial of FATE-NK100 in ovarian cancer.

We will also see data readouts throughout the year that could move the stock. Fate is expected to release data on FT516 this summer and FT500 and FT596 by the end of the year.

There will also be new trials beginning and new submissions to the FDA for approval to begin other trials.

Lightning Strike

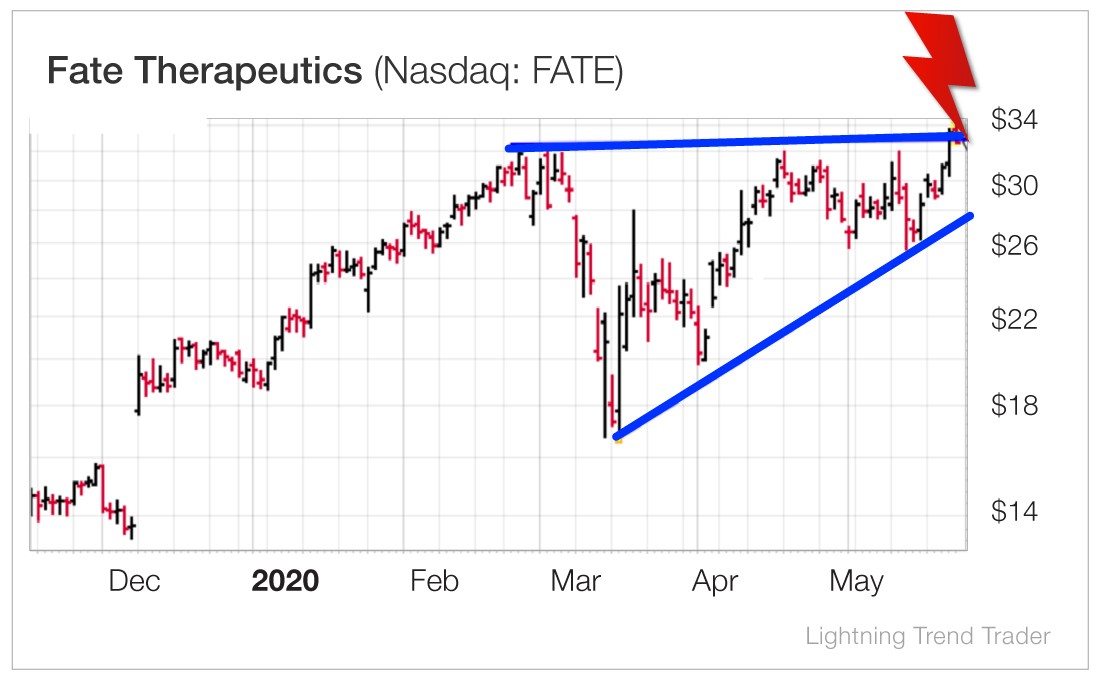

Fate Therapeutics is breaking out of an ascending triangle, which is a reliable bullish pattern. The $34 area acted as resistance several times in the past, but the stock has now broken above resistance and looks to be heading toward at least $50 in the next few months.

This is an exciting early-stage company with plenty of cash, many upcoming catalysts and a great-looking chart.

Action to Take: Buy Fate Therapeutics (Nasdaq: FATE) at market. Place a 25% trailing stop to protect your principal and profits.

CAT-3 Profit Storm Pick: Myovant Sciences

Our CAT-3 Profit Storm pick is Myovant Sciences (NYSE: MYOV). Myovant Sciences is a U.K.-based healthcare company focused on addressing unmet needs of patients in women’s health and prostate cancer.

Myovant Sciences’ lead drug candidate is called relugolix. It’s a small molecule, gonadotropin-releasing hormone (GnRH) receptor antagonist being studied to treat uterine fibroids, endometriosis and advanced prostate cancer.

The drug works by blocking GnRH receptors to decrease the release of gonadotropins. This in turn decreases the production of estrogen and progesterone in women and testosterone in men.

The company’s HERO study is a Phase 3 clinical trial that is evaluating relugolix in men with advanced prostate cancer. Data from the study is due to be reported in the second quarter of this year.

Doctors, patients and investors are optimistic that relugolix will prove to be effective in treating castrate-sensitive prostate cancer – cancer that can be controlled by limiting testosterone levels.

Relugolix has shown in Phase 2 to prevent testosterone flares or temporary increase in body testosterone levels.

That means that Myovant Sciences’ CAT-3 Profit Storm is already beginning to build. Investors should hunker down, acquire shares and wait for the profit winds to begin to blow… especially since there’s a second CAT-3 disturbance coming behind it.

Topline results from the company’s Phase 3 SPIRIT trial will be released in the first quarter of this year. It’s evaluating relugolix in women with endometriosis-associated pain.

With two shots on goal, a CAT-3 Profit Storm is all but assured.

Action to Take: Buy shares of Myovant Sciences (NYSE: MYOV) at the market. Place a 25% trailing stop to protect your principal and profits.

CAT-4 Profit Storm Pick: Vertex Pharmaceuticals

It’s difficult to find companies that aren’t negatively impacted by the COVID-19 virus. Nearly any company that depends on consumers surely is. And most companies that rely on business spending are too.

It’s one of the reasons I love the healthcare sector. No matter what is happening with the economy, patients need their meds and their procedures. The companies that can meet those demands can generate substantial profits for shareholders, whether we’re in a recession or not.

Vertex Pharmaceuticals (Nasdaq: VRTX) is one of those companies. It has four approved drugs for cystic fibrosis, a virtually untreatable disease until Vertex’s therapies hit the market.

Last year, Trikafta was approved in the U.S. for cystic fibrosis patients with a specific genetic mutation. Vertex’s four cystic fibrosis medicines now cover 90% of the patients who need a lifesaving drug.

Patients with cystic fibrosis have a life expectancy of the late 30s to early 40s, although that number is increasing every year thanks to the new therapies.

Last year, Vertex generated $4 billion in revenue due to its cystic fibrosis franchise, up 32%. This year, the company forecasts the number to balloon to between $5.1 billion and $5.3 billion. Vertex is profitable and cash flow positive. It also has $3.8 billion in cash.

Importantly, management stated earlier this year that the coronavirus outbreak will not affect the company’s guidance or its ability to get drugs to patients. It may delay some of the clinical trials it is operating. Though it will enable virtual consultations and home delivery of drugs in an effort to continue some studies.

Catalysts

Vertex has data coming out on various clinical trials throughout the year, so there should be many opportunities for the stock to take off.

Lightning Strike

Vertex is at the top of a symmetrical triangle, which features both an up trendline and a down trendline. I expect it to break through resistance and out of the triangle. If the breakout is successful, it should trade up to about $280 and maybe higher from there.

Let’s get in now before the stock breaks to the upside.

Action to Take: Buy Vertex Pharmaceuticals (Nasdaq: VRTX) at market. Place a 25% trailing stop to protect your principal and profits.

CAT-5 Profit Storm Pick: uniQure

Finally, our CAT-5 Profit Storm pick is uniQure (Nasdaq: QURE). This is the type of Profit Storm I get most excited about.

Founded in 1998 and headquartered in Amsterdam, uniQure is currently developing treatments that could provide cures for hemophilia, Huntington’s disease and other severe genetic disorders.

UniQure’s leading gene therapy product is AMT-061, which treats severe and moderately severe hemophilia B, a deadly blood disease. The therapy is in Phase 3 clinical trials, the last stage prior to FDA approval.

In the U.S., AMT-061 has been granted breakthrough therapy designation and orphan drug designation by the FDA. And it’s received a priority medicine (PRIME) regulatory initiative by the European Medicines Agency (EMA).

While AMT-061 will be the driving force behind uniQure, the company has a very promising pipeline of products in various stages of development to treat hemophilia B, Huntington’s disease, heart failure, hemophilia A, Fabry disease and more.

The competition in the market for promising gene therapy treatments is rapidly intensifying.

Big pharmaceutical companies are scrambling to shore up their product and developmental pipelines. Buying up the best candidates they can find has become the favored method.

Takeda (OTC: TKPHF) acquired biopharmaceutical company Shire for $62 billion, due in no small part to the company’s portfolio of hematology therapies – most specifically, a clotting infusion treatment.

In the largest-ever international acquisition by a Japanese company, Takeda – which had to raise its offer four times to satisfy Shire management and shareholders – paid roughly $66.21 per share, a 64.4% premium over the value of the shares at the time.

A report from Bloomberg reported that uniQure is currently working with advisors as it weighs options, including partnerships and a potential sale.

Brokerage firm Cantor Fitzgerald has speculated that uniQure “could be next,” and I agree.

Large cap pharmaceutical companies, such as Novo Nordisk (NYSE: NVO), Pfizer (NYSE: PFE) and Sanofi (Nasdaq: SNY), may be the most likely candidates to strike a deal… or make an offer. That’s when the Profit Storm will hit.

I think the reports swirling around uniQure are accurate. There’s a CAT-5 Profit Storm brewing around uniQure that I believe could strike before AMT-061 is officially approved by the FDA.

Action to Take: Buy uniQure (Nasdaq: QURE) at market. Place a 25% trailing stop below your entry price.

These five stocks are on the verge of forming the biggest moneymaking opportunities I see in the market today. The time to prepare for the next Profit Storm is now. This is the fastest and most consistent way to make money in stocks.