The Next Cash Flow Superstars

It’s a well-kept secret that only the top market analysts know. Contrary to popular belief, earnings are not the ultimate predictor of stock market success.

While most investors chase flashy earnings numbers that can be manipulated with accounting tricks, the smartest money follows the one metric that never lies: cash flow.

As Warren Buffett says, “If you attempt to assess intrinsic value, it all relates to cash flow.” And Richard Branson puts it even more bluntly: “Never take your eyes off cash flow, because it’s the lifeblood of business.”

The data proves it. From 2010 to 2024, stocks selected using our proprietary, cash flow-centric criteria delivered a total return of 1,397% – absolutely crushing the S&P 500’s 601% return over the same period.

Research from The Wall Street Journal backs this up too, finding that companies in the top 10% of cash flow growth were the best performers in the entire market.

Pacer ETFs even discovered that cash flow beat out every other metric – including earnings, sales, dividend yields, and P/E ratios – in predicting the best-performing stocks.

Today, I’m going to reveal the top three companies that were identified by my rigorous cash flow screening process.

Each of these companies meets my strict criteria:

- Small companies (under $10 billion market cap) flying under Wall Street’s radar

- Assets valued higher than debt for ultimate safety

- Strong cash flow growth that’s accelerating year after year (the lifeblood of any successful business)

- Efficient business models that specialize in turning assets into cash.

All three companies have the potential to deliver the kind of life-changing returns we’ve seen from past cash flow superstars like Eaton (NYSE: ETN), NextEra Energy (NYSE: NEE), and Broadcom (Nasdaq: AVGO) − stocks that turned $10,000 into hundreds of thousands while paying growing dividends every year.

Let me introduce you to your next cash flow superstars…

Cash Flow Superstar #1: Tecnoglass (NYSE: TGLS)

The Company That DOMINATES Architectural Glass Manufacturing in America

Tecnoglass is a refreshingly straightforward business in a market dominated by complicated tech stocks. The company manufactures high-end aluminum and vinyl products and architectural glass for residential and commercial buildings.

What makes Tecnoglass special, however, is how it’s quietly dominating its market while generating massive amounts of cash.

Let me show you why Tecnoglass caught my attention…

While most investors were focused on earnings, the real story was hidden in the company’s cash flow.

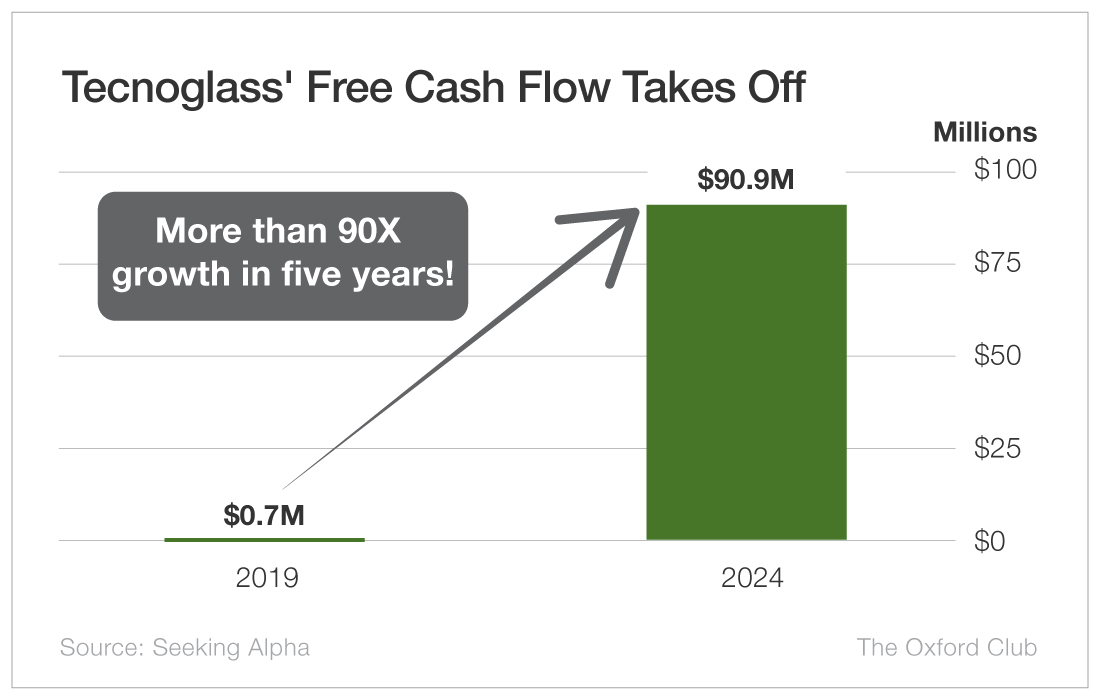

In 2019, the company generated less than $1 million in free cash flow. By 2022, that figure had jumped to over $70 million, and in 2024, it reached more than $90 million.

That’s cash flow growth of over 90X in just five years. That kind of explosive acceleration often precedes major stock price moves.

Even more impressive, Tecnoglass converted 61.8% of its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) into operating cash flow in 2024. When this company reports profits, those profits are real dollars hitting the bank account.

Tecnoglass operates what I call a “cash-printing machine.” It manufactures its own glass and produces its own aluminum frames, which allows it to maintain substantial control over costs and quality while reducing dependency on outside suppliers.

The company ended 2024 with a record backlog of $1.1 billion, up 27.6% year over year. By the second quarter of 2025, that backlog had grown to $1.2 billion. When a company has that much future business already locked in, cash flow becomes incredibly predictable.

Tecnoglass has been sharing its cash bonanza with shareholders. The company has increased its dividend by an astounding 445% since 2021. In late 2024, it raised the quarterly dividend by 36% from $0.11 to $0.15 per share. Its recent dividend-raising history suggests that another increase is likely coming in the second half of 2025.

Remember, I demand safety alongside growth. Tecnoglass delivers on both fronts. The company achieved a net cash position at year-end 2024, meaning it actually has more cash than debt. It paid down $65 million in debt throughout 2024 and held $138 million in cash as of the second quarter of 2025. Total assets of nearly $1.2 billion versus a minimal debt load gives the company exactly the kind of rock-solid financial foundation I look for.

Several powerful tailwinds are accelerating Tecnoglass’ cash flow growth. The April 2025 acquisition of Continental Glass Systems for $30 million expands its U.S. manufacturing footprint and opens new commercial markets. Ongoing infrastructure investment and construction activity are driving demand for architectural glass. Federal tax incentives for energy-efficient windows are spurring replacement projects, while continued commercial development provides additional growth opportunities.

The company has also built a massive competitive moat. The barriers to entry in architectural glass are enormous. You need specialized equipment, technical expertise, and years to build customer relationships.

With a market cap of just $3.5 billion, Tecnoglass is still flying under Wall Street’s radar… yet it’s generating more cash flow than many companies twice its size. And with 2025 revenue guidance of $980 million to $1.02 billion and adjusted EBITDA guidance of $310 million to $325 million, Tecnoglass is positioned for continued explosive cash flow growth.

Eaton turned $10,000 into $225,000 over 16 years while growing its dividend alongside its cash flow. It also has the distinction of generating the largest return in the history of The Oxford Income Letter: a 584% gain in under 10 years.

Tecnoglass may not become a nearly seven-bagger like Eaton, but I could see it following a similar path.

Recommendation: Buy Tecnoglass (NYSE: TGLS) at market. Set a 25% trailing stop to protect your principal and your profits.

Cash Flow Superstar #2: United States Lime & Minerals (Nasdaq: USLM)

The Ultimate Cash-Generating Royalty Business

If you want to understand the power of cash flow investing, United States Lime & Minerals is the perfect example. This company operates one of the most cash-gushing business models I’ve ever seen… and most investors have never even heard of it.

The company owns lime and limestone quarries across Arkansas, Colorado, Louisiana, Oklahoma, and Texas. But it doesn’t just dig rocks out of the ground. It controls nearly every step of the process, manufacturing pulverized limestone, quicklime, hydrated lime, and lime slurry for essential industries.

Lime and limestone products are vital inputs for construction, environmental applications, industrial processes, and agriculture. These aren’t discretionary purchases that disappear in tough times. They’re necessities that create steady, predictable demand regardless of economic conditions.

U.S. Lime & Minerals’ products are crucial for everything from building roads and making concrete… to water treatment and pollution control… to steel and paper production.

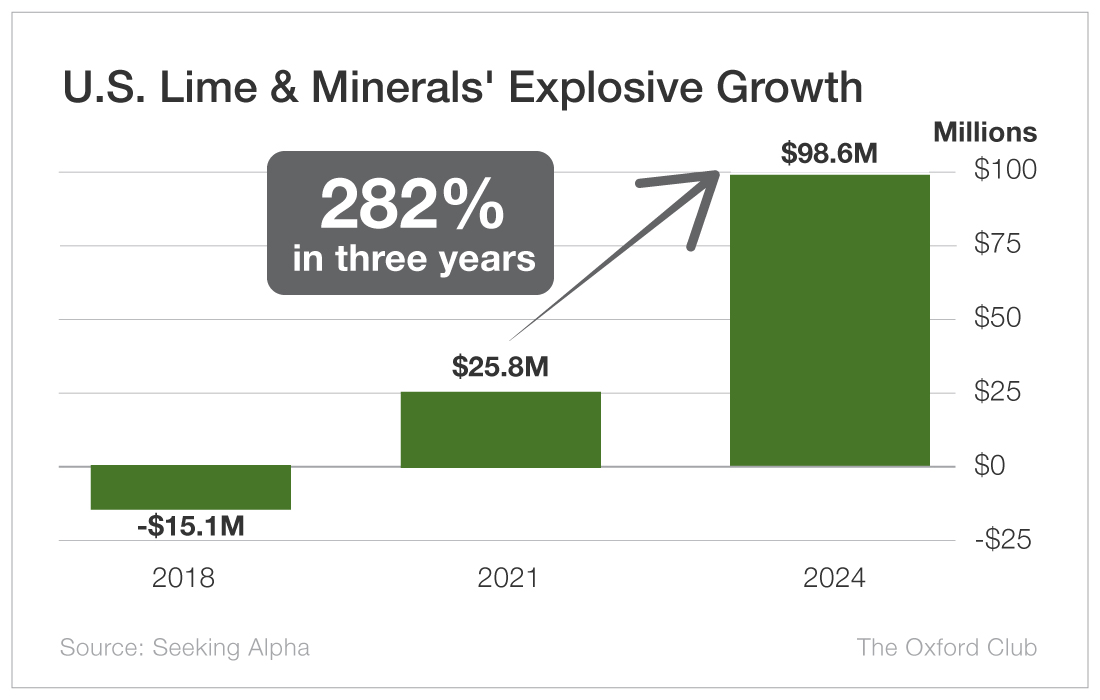

The cash flow numbers tell an incredible story. In 2018, the company’s free cash flow was negative. As recently as 2021, it was just under $26 million. But by the end of 2024, it had surged to nearly $100 million – a 282% increase in three years.

I expect that strong cash flow growth to continue.

Opening a new lime quarry requires massive capital investment, geographic proximity to customers, technical expertise in processing and quality control, and environmental permits that can take years to obtain. These barriers are so high that United States Lime & Minerals faces minimal competition in its regional markets. That gives it tremendous pricing power, which is exactly what we want to see as investors.

The Infrastructure Investment and Jobs Act is a massive catalyst for the company. This $1.2 trillion spending program is driving strong demand for construction materials, particularly lime products used in road construction and repair, bridge and tunnel projects, water treatment facility upgrades, and environmental remediation projects. United States Lime & Minerals is well positioned to benefit from this multiyear infrastructure boom.

The company also owns natural gas wells on its Texas property in the Barnett Shale Formation. While this is a smaller part of the business, it provides additional cash flow and acts as a hedge against energy price inflation.

U.S. Lime & Minerals operates with an incredibly strong balance sheet. It has no debt and nearly $320 million in cash. This net cash position provides ultimate flexibility, and the company’s conservative capital allocation focuses on high-return projects.

This financial strength allows U.S. Lime & Minerals to invest in growth opportunities while returning cash to shareholders through dividends.

The company’s dividend has grown alongside cash flow too. From 2014 to 2019, the dividend increased by just 8%. But in less than six years since, it has more than doubled from $0.108 to $0.240 per share annually. That’s a terrific 122% increase, reflecting management’s confidence in its ability to continue to generate cash and reward shareholders.

With a market cap of approximately $3.6 billion, United States Lime & Minerals is dramatically undervalued relative to its cash-generating power. The company’s annual free cash flow would justify a much higher valuation.

Compared with oil and gas royalty companies that trade at much higher multiples despite having more volatile cash flows, this company provides similar cash generation with much greater stability.

I expect United States Lime & Minerals to follow the path of NextEra Energy, providing steady, consistent cash flow growth that translates into rising stock prices and dividends. With the infrastructure spending cycle just getting started and environmental regulations driving increased lime demand, the company has multiple years of growth ahead. This is the type of “boring” business that quietly creates massive wealth for patient investors who follow the cash flow.

Recommendation: Buy United States Lime & Minerals (Nasdaq: USLM) at market. Set a 25% trailing stop to protect your principal and your profits.

Cash Flow Superstar #3: A10 Networks (NYSE: ATEN)

The AI Security Play That Could Be the Next Broadcom

Here’s my “moonshot” pick − the company I believe has the potential to deliver the biggest returns of the three.

A10 Networks is perfectly positioned at the intersection of two massive growth trends: artificial intelligence and cybersecurity.

While tech giants like Microsoft and Google get all the headlines for AI, A10 Networks is quietly providing the essential security infrastructure that makes AI data centers possible.

Data centers consume massive amounts of power. A10’s security and infrastructure solutions are specifically designed for these high-performance environments.

As CEO Dhrupad Trivedi explained, “AI continues to serve as a significant catalyst for spending in general, and for A10 customers’ priorities in particular, because of the efficiency of our high-throughput, low-latency solutions. Our solutions lower the total cost of ownership, utilizing less power and integrated security capabilities, creating a durable competitive advantage within energy-hungry AI data centers.”

The company was recently selected to partner with global leaders in AI data centers − a validation that A10’s technology is becoming essential infrastructure for the AI revolution.

Like Constellation Energy’s partnership with Microsoft for nuclear power, A10 Networks works directly with household names in Big Tech to secure their AI projects. These are strategic partnerships that position A10 at the center of the AI buildout.

As data centers expand to handle AI workloads, every major tech company needs A10’s security and infrastructure solutions. This creates a massive, multiyear growth opportunity.

In February 2025, A10 also acquired ThreatX Protect, bolstering its capabilities to protect web applications and software interfaces – a critical area for enterprise customers concerned about AI security threats. This strategic acquisition expands A10’s total addressable market while enhancing its competitive positioning.

A10 Networks operates two key segments, both of which are showing strong growth. Trailing 12-month service provider revenue grew 14% year over year in the second quarter of 2025, driven by data center expansions and AI infrastructure investments. Enterprise revenue increased 8% year over year, supported by growing demand for cybersecurity solutions. This diversification provides stability while the AI boom drives acceleration.

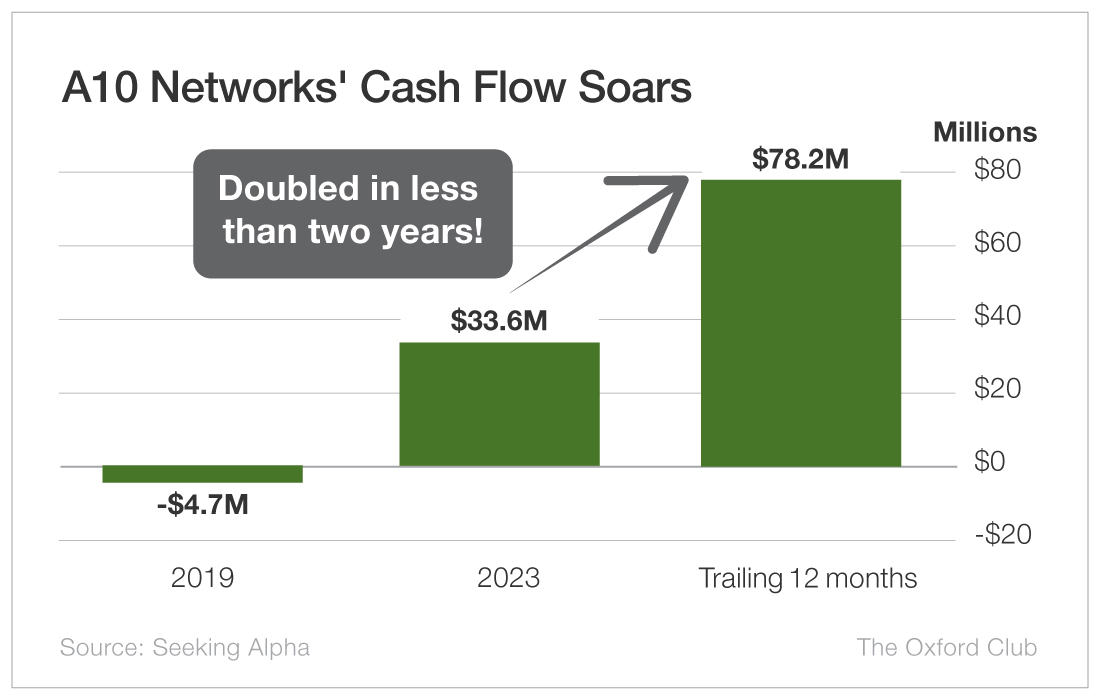

Overall, A10 Networks is showing exactly the kind of cash flow acceleration that preceded massive stock gains in companies like Broadcom. The company generated over $70 million in free cash flow over the last 12 months, more than double the $34 million it made in 2023. As recently as 2019, free cash flow was negative.

The company held $367 million in cash and short-term investments as of the second quarter of 2025, nearly double the $196 million it held at the end of 2024. Plus, its accrual ratio shows excellent cash conversion – meaning when it reports profits, those profits represent real cash in the bank.

Furthermore, the cybersecurity market is projected to grow from $173 billion in 2022 to $266 billion by 2027. Within that market, AI security is the fastest-growing segment. Despite having a market cap of just $1.3 billion, A10 Networks is capturing an increasing share of this massive market while maintaining high margins and strong cash generation.

So, why do I think A10 Networks could be the next Broadcom?

Consider the parallels…

- Like Broadcom’s chips, A10’s security solutions are becoming essential for AI infrastructure.

- A10 maintains 80%-plus gross margins, similar to Broadcom’s high-margin business model.

- A10 pays a consistent quarterly dividend ($0.06 per share) and buys back shares, just as Broadcom does.

- A10 is positioned at the beginning of the AI infrastructure buildout, similar to Broadcom’s early positioning in mobile chips.

In 2024, Broadcom became the third-biggest winner in the history of The Oxford Income Letter, with a 403% gain in just four years. Those phenomenal returns came from being positioned at the center of major technology transitions, and A10 Networks has that same positioning today with AI and cybersecurity.

At current levels, A10 Networks offers an extremely intriguing risk/reward profile. The downside is limited by the company’s strong balance sheet and consistent cash generation. The upside is potentially massive if it captures even a small percentage of the AI security market.

Recommendation: Buy A10 Networks (NYSE: ATEN) at market. Set a 25% trailing stop to protect your principal and your profits.

The Power of Cash Flow Investing

These three companies represent everything I look for in cash flow superstars:

- Small enough to fly under Wall Street’s radar

- Strong, accelerating cash flow that’s outpacing earnings

- Solid balance sheets with assets exceeding debt

- Efficient business models that specialize in turning assets into cash.

They demonstrate why cash flow is the ultimate investment metric: While earnings can be manipulated, cash flow tells the truth about a business’ real performance.

Remember, Bloomberg data proves that stocks selected using cash flow metrics delivered 1,397% returns from 2010 to 2024, more than doubling the S&P 500’s performance.

Together, these three companies could form the foundation of a portfolio designed to crush the market over the next five to 15 years while providing growing income every year.

The choice is yours. You can continue to follow earnings like everyone else, or you can follow the one metric that Warren Buffett, Richard Branson, and every other successful long-term investor rely on.

These three cash flow superstars won’t stay hidden forever. Once Wall Street discovers their cash-generating power, the opportunity to buy at today’s prices will disappear.

Start building your positions today, and let the power of cash flow investing work for you.