Fed Fortunes: 3 Power Stocks Set to Skyrocket

The Federal Reserve was too late in raising rates to tame inflation and has been too late in cutting rates to stimulate the economy.

The market has become more volatile, and fears that a recession is looming on the horizon have begun circling in the media.

Fed Chairman Jerome Powell needs to do something big to respond. He needs to reassure people living in an unstable economy.

After the most recent meltdown and troubling economic data, the chances of a rate cut have gone up to 100%, according to CME Group.

But I predict this will be the first of many interest rate cuts… and the cuts will be more dramatic than what most people think.

When these cuts happen, the markets will soar and investors will cheer, but Wall Street will miss out on the biggest gains…

They will be so focused on the S&P 500 that they’ll miss a rare group of overlooked opportunities I call Power Stocks, which historically skyrocket when the Fed cuts rates.

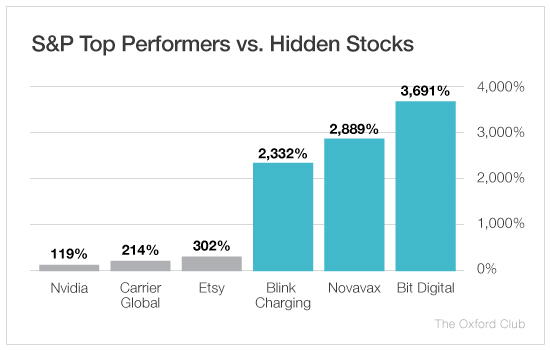

The last time the Federal Reserve cut rates in 2020, the big S&P 500 winners included Etsy with a 302% gain, Carrier Global Corp. with a 214% return, and Nvidia with a 119% gain. All respectable, but nothing compared with the top performers among the Power Stocks.

Their returns were as big as 2,332% on Blink Charging, 2,889% on Novavax, and even 3,691% on Bit Digital. They absolutely crushed the performance of the best of the S&P 500’s top winners.

And that was far from a fluke. That’s routine for these stocks. In fact, over the past 75 years, Power Stocks have delivered more than twice the return of the S&P 500 in the three months after a rate cut…

Power Stocks are, of course, microcap stocks. That means companies with a market cap of less than $300 million. However, I consider some companies on the small end of small caps in the same category as Power Stocks. They’re small, they’re agile, and they can deliver enormous gains in short order.

Now, that might sound like penny stocks, but Power Stocks couldn’t be further from those. Penny stocks are companies with nothing to them aside from a gimmick and maybe a bit of media hype. But they’re poorly run, their products or services have no staying power, and investing in them is like gambling.

Microcap Power Stocks, on the other hand, are small, innovative companies with lots of potential. And I look for three criteria to determine if a company is a Power Stock…

- Sales increasing for three quarters in a row or more

- Low share prices and great valuations

- Heavy insider buying, ideally in large clusters.

With this new rate cut, there’s another opportunity to take home enormous profits that Wall Street has to leave on the table. See, the big boys of the market, the BlackRocks, Warren Buffetts, and State Streets of the world, can’t invest in microcap stocks.

They simply carry too much risk for the amount of money these companies invest.

But Power Stocks are the perfect size for a small investment to go a long way, especially if you add in an options play. They’re the perfect stocks for the individual retail investor to make a killing with on the first rate cut and all the cuts to follow.

And I’ve found three Power Stocks that I believe will be some of the biggest winners of this first rate cut…

An Energizing Pick at the Crossroads of Past and Future

We’re at a crossroads with the energy infrastructure that supports our modern economy. Countries around the world are attempting to shift to renewable and green energy. But the world is still powered by fossil fuels.

Fortunately, there’s one company sitting right at that crossroads. And it’s facilitating that shift with the help of AI and a fleet of cutting-edge robots.

It’s called Helix Energy Solutions Group (NYSE: HLX). Its main goals are to maximize the efficiency of existing offshore oil production and support the shift to a wind-powered offshore energy generation model.

Its three-part business model is making it happen.

First, Helix extends the life and expands the efficiency of existing offshore oil wells. It can modify and repair older wells to keep them around and efficient for longer periods. This both prevents the need for new wells and produces more oil per well.

Second, it decommissions and helps companies abandon wells safely. That means tearing down enormous offshore wells in a way that doesn’t cause a massive oil leak, like the Deepwater Horizon disaster. (Helix played a key role in stopping that spill.)

Third, the company is using the technology it perfected in offshore oil wells to construct new offshore wind farms. Deep sea construction, maintenance, and repair are skills easily transferrable from oil production to wind power generation.

That’s possible thanks to a fleet of robots that can both build new things and repair broken wells before they create an ecological disaster.

The company has participated in more than 1,750 underwater interventions for oil wells worldwide (most famously the Deepwater Horizon spill). The Helix Fast Response System uses the company’s state-of-the-art ships and robots to repair broken wells. Today, it’s the spill response system on record for roughly 160 new drilling permits issued in the Gulf of Mexico since 2014.

Those machines, powered by AI, can also be used to build new wind farms in the ocean.

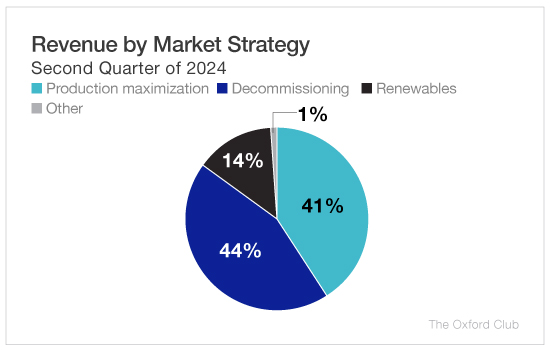

But it’s decommissioning that represents the bulk of Helix’s revenue. The company’s AI gives it an edge… and as we move away from oil and gas, the need for decommissioning of existing oil wells increases.

Decommissioning accounted for 35% of the company’s revenue in 2022 but has been on the rise… amounting to 44% in the second quarter of this year.

And this company has been growing fast. Over the last 12 months, it grew its revenue by 24.4%. For the whole of 2023, it took home revenues just shy of $1.3 billion, up 47.7% over 2022’s number.

For the first and second quarters of 2024, it has grown its year-over-year revenue by 18.4% and 18.1%, respectively, topping $364.8 million in the second quarter. Revenue has been growing regularly quarter over quarter and year over year… In fact, over the past three years, the company has increased its revenue at a compound annual growth rate (CAGR) of 27.05%. So this one easily satisfies the increasing sales criterion I look for.

Net income in Q2 2024 topped $32.3 million, up a staggering 354.8%. The company’s cash reserves are sitting at $275.1 million, up 50.6% from where they were in Q2 2023. And debt sits at a manageable $404.22 million.

This is a company on a growth trend. It’s up 7% over the last six months. Despite that, it will run you just $10 per share. And it’s trading at just 1.2 times book value. It’s dirt cheap and satisfies both the low share price and great valuation criteria I target.

Once rates fall and borrowing becomes cheaper, that will give it a serious shot in the arm. This company’s growth is going to accelerate even faster than it’s already been moving. And you’ll be glad you bought in now…

The company’s leadership certainly thinks so. In the last six months, company insiders have bought 823,763 shares. The largest one was from Owen Kratz, the company’s CEO, who bought 3.7 million shares on May 22, 2024. That means it also has the insider buying I look for in a Power Stock.

This is not an opportunity you can afford to miss.

***Action to Take***

Buy Helix Energy Solutions Group (NYSE: HLX) at market.

Making Lemonade

Dealing with insurance companies is an oftentimes irritating experience. If you’re filing an insurance claim in the first place, things have gone wrong for you that day – you’ve gotten into a car accident, a storm has damaged your home, or something along those lines has occurred. That puts you in a stressful position.

You just want to get the damage fixed as soon as you can as well as possible. But your insurance company is trying to get it done as cheaply as possible. Traditional insurance companies generate profit from whatever premium is left after paying claims and expenses.

The lower the cost they can get your repairs done for, the more profit they can pocket. To them, the ideal insurance payer is one who never needs to file a claim and pays the premium ad infinitum. This creates a frustrating and antagonistic relationship between the customer and the insurer.

But Lemonade Inc. (NYSE: LMND) is different. Instead of collecting its profit from unclaimed premiums, this AI-driven insurance company takes a flat fee out of your premium for its profit. Then, after paying its employees and handling any claims you make, the difference is paid out to a charity of your and the insurance payer’s choice (this is called the Lemonade Giveback).

That model allows Lemonade to offer some of the cheapest premiums on the market. And the company’s AI usage allows it to cut premiums even further. Rather than having to play phone tag with insurance agents and worry about your claim being approved, Lemonade allows you to file a claim through an AI-driven app.

If your claim is approved, the approval is instant, and it’s paid out in seconds. And I mean that literally. The company managed to complete a claim in just two seconds, setting the record for an insurance claim.

If your claim is not instantly approved, Lemonade’s AI hands it over to a human insurance agent. The AI allows the simple and straightforward claims to be paid out quickly and leaves the more complicated claims for human agents. The result is a cheaper insurance option that makes the majority of insurance claims easier and faster to handle…

And if we take a look at the company’s balance sheet, we see this novel take on the insurance industry appears to be working out well…

For 2023, the company took home premium and annuity revenues of $315.2 million, up a staggering 82.8% over 2022’s. Total revenues for 2023 totaled $429.8 million, up 67.4% year over year.

The company continued that growth into 2024. Total revenues topped $119.1 million in the first quarter of 2024, up 25.1% over Q1 2023’s. Revenues for the second quarter of 2024 totaled $122.1 million, up 16.7% over Q2 2023’s. Those are just the latest in the company’s 15-quarter revenue growth trend that makes Lemonade easily pass the three quarters of sales growth I look for.

Over the past five years, the company has increased its revenue at a CAGR of 63.29%. That has accelerated in the past three years, with the CAGR reaching 73.65%. It’s also operating with a gross margin of 41.16% and has cash reserves of $343.2 million.

On top of that, this company is an incredible bargain. It’s trading at 1.8 times book value, and one share will run you just $15 at the time of writing, so it satisfies my second criterion by being a great value and having a low share price.

As soon as rates lower, expect Lemonade to take off. And Lemonade’s leadership certainly thinks so. In the past 12 months, insiders have purchased $398,050 worth of shares. The biggest purchase was from Lemonade’s CFO, Timothy Bixby, who bought 15,000 shares on June 14, 2024. That’s exactly the sort of insider buying I look for in a microcap, so it easily satisfies my third criterion.

This market has been giving us a lot of lemons over the past few years, but this Power Stock is a good opportunity to make some lemonade out of them. You’ll want to buy it now…

***Action to Take***

Buy Lemonade Inc. (NYSE: LMND) at market.

Lindblad, I Presume?

In an age where anyone with an internet connection can see high-resolution satellite photos of the entire planet at a moment’s notice, exploration might seem like a thing of the past.

The first person to discover a new river or mountain gets remembered in history books. Their name might even be immortalized on maps for centuries to come…

But there aren’t any frontiers left. At least, not on this planet. However, that doesn’t mean that human drive to dive headfirst into the unknown has gone anywhere…

In fact, one company has managed to fuel an entire successful business on the back of that all-too-human desire.

It’s called Lindblad Expeditions Holdings (Nasdaq: LIND), and it’s a cruise line that could have been dreamt up by Ferdinand Magellan or Dr. David Livingstone. It offers cruises to Alaska, Baja California, the Galapagos Islands, Egypt, and Patagonia, among others.

In addition, the company is the official partner of National Geographic and has been since 2004. And, like the magazine, it wants to inspire people to explore and care about this little blue marble of ours.

Since 2004, when its National Geographic partnership started, the company has seen its passenger capacity increase by a factor of 4 and its revenue increase by a factor of 10. Lindblad renewed that partnership for another 17 years in November 2023, so I expect that growth will continue for the foreseeable future.

Lindblad has been in business for over 50 years and sails its 17 ships to destinations across all seven continents. What’s more, the company has operated 100% carbon neutral since 2019.

The company even uses AI to help in conservation efforts. As National Geographic’s partner, it will take the magazine’s photographers and writers out on cruises, and it has begun using AI to identify individual whales within minutes to provide a more accurate idea of whale populations and movements.

Lindblad is primed for a takeoff, one that I think will happen as soon as the Fed lowers its rates. And the company’s leadership certainly thinks so…

Insiders currently hold 34% of the company’s shares, and they are loading up on more. In the last 12 months, insiders have bought $1.09 million worth of shares, and there has only been one sale, of $178,707 worth of shares, in that time.

In the second quarter of 2024, Alex Schultz bought up $580,000 worth of shares. He followed that up with a purchase of $275,000 worth of shares through the third quarter of 2024. Despite that, right now this company is trading for just $10 and has a market cap of under $400 million. So it has the massive insider buying I look for, and it’s flying under Wall Street’s radar… thought it won’t for long…

Revenue has surged in every one of the last 12 quarters. Most recently, Lindblad’s revenue grew 9.4% to $136.5 million in the second quarter of 2024. Coincidentally, that lines up with Schultz’s big share purchase. This company has the quarter-over-quarter sales growth I look for in Power Stocks…

And that’s not all. Cumulatively, revenue has increased at a CAGR of 217.77% over the last three years, and the company is trading at a -1.54 price-to-book ratio, meaning it’s extremely undervalued. In total, revenue is up 606% since 2020 and is showing no signs of slowing down.

Despite that, this company trades for just $7 per share and is a fantastic value at these miniscule prices. So it handily passes the second criterion I look for by being a fantastic value.

Lindblad has all the tailwinds surging behind it I like to see. It’s got massive insider buying, it’s growing its revenue rapidly quarter over quarter, and it’s got a dirt-cheap share price and bargain-basement valuation.

You’ll want to explore new economic horizons by adding a few shares of Lindblad to your portfolio before the Fed raises rates.

***Action to Take***

Buy Lindblad Expeditions Holdings (Nasdaq: LIND) at market.

Make a Fortune From the Fed…

When the Fed lowers rates, the market we’ve had since the COVID-19 pandemic will change completely. The rate decrease will be the catalyst that will send stocks into the stratosphere.

And Power Stocks, like the three companies in this report, will be far and away the biggest winners as the market changes. You’ll profit right alongside those companies if you buy in now.

Power Stocks routinely outperform their larger counterparts. The last time the Federal Reserve cut rates in 2020, they saw returns as big as 2,332%, 2,889%, and even 3,691%. They absolutely crushed the performance of the best of the S&P 500’s top winners.

The moves the Fed is about to make are going to kick off a long-term bull market in microcaps, the likes of which we’ve maybe never seen before – and may never see again. These microcap Power Stocks are poised to take off… and are your best shot at those 30X-type gains in the next year.