Apple’s Space Partner

Apple may be on the verge of its most disruptive launch since the original iPhone.

It’s the foundation for a new era of connectivity that could seriously disrupt the $200 billion wireless carrier industry.

And at the heart of this quiet revolution is a company almost no one on Wall Street is paying attention to.

It’s a $5 billion microcap stock… One that has already embedded its technology into over a billion iPhones.

Apple has already committed up to $1.5 billion to this partner, yet much of the market hasn’t caught on to the potential here yet.

But history shows that when small suppliers become essential to Apple’s biggest product waves… quadruple-digit gains are not uncommon.

So what is this potential launch I’m predicting – and, more importantly – who’s the new partner Apple has chosen for the rollout?

It starts with a feature that’s been around since 2022…

Apple’s Next Step Toward Mobile Domination

Apple debuted a new feature in its iPhone 14 called Emergency SOS via Satellite, allowing users to send emergency texts when outside cell or Wi-Fi coverage.

Not the most exciting upgrade. But certainly useful.

Most iPhone owners will never trigger it. But for those in danger or in unreachable locations, it offers a potentially lifesaving connection.

But what caught my attention was what happened in 2024.

That’s when Apple quietly committed up to $1.5 billion to expand its satellite footprint with its “space partner” – satellite network provided, Globalstar Inc. (Nasdaq: GSAT).

Of that total, $1.1 billion is allocated for prepayments for Globalstar’s satellite services.

The other $400 million gives Apple a 20% equity stake in Globalstar.

And Globalstar has committed 85% of its upgraded network capacity to Apple’s cause.

When this announcement hit, Globalstar’s stock jumped over 30% in a single session.

I can easily understand why…

While Apple hasn’t revealed any serious plans to upend existing mobile carriers with the iPhone’s built-in satellite connection, this partnership puts it in a prime position to do so.

And when it flips the switch on such a project, it could send Globalstar to the moon.

The Hidden Satellite Backbone Powering iPhones

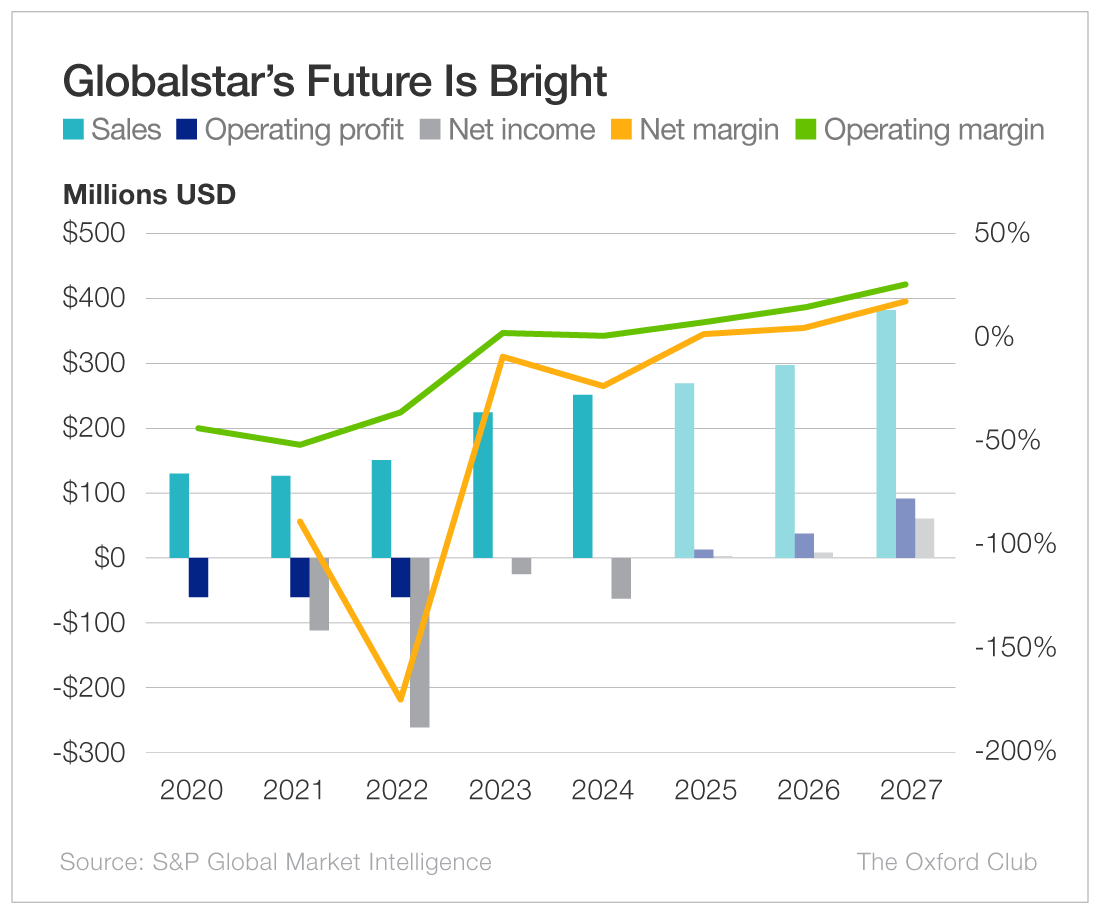

For years, Globalstar was written off as just another struggling satellite operator – long on vision but short on profitability. That narrative is now completely broken.

The company’s latest results don’t just show improvement… they signal a full-blown financial turnaround.

In the second quarter of 2025, revenue climbed 11% year over year to $67.1 million. But the headline number isn’t the only story…

Globalstar turned the corner on profitability. It flipped from a net loss to a $19.2 million profit, delivering earnings per share of $0.13.

Adjusted EBITDA surged to $35.8 million, translating to a 53% margin – a level that rivals far larger peers in the satellite communications space. Adjusted free cash flow for the first half of 2025 came in at $77.9 million, up sharply from $51.9 million in the same period last year.

Globalstar holds $308 million in cash and controls $1.91 billion in total assets. And thanks to Apple, a significant portion of future revenue is already locked in – reducing uncertainty and creating a powerful financial cushion.

With a solid cash position, minimal financing risk, and a long-term partner in Apple (already footing the bill for much of its expansion), Globalstar now has the financial stability to fully capitalize on its growth initiatives.

And this combination of profitability, free cash flow, and locked-in revenue streams is what gives this stock room to run…

4 for 4: How Globalstar Meets Every Microcap Benchmark

When I recommend a microcap stock like this, I’m not looking for a flashy story or a quick pop. I’m looking for four critical traits that separate real opportunities from the penny stock graveyard: consistent sales growth, rising earnings, undervaluation, and strong insider or institutional commitment.

- Sustained Sales Growth

Globalstar isn’t a “maybe someday” idea with a prototype on a napkin – it’s a fast-growing business with a real product in wide commercial use. Its satellite technology powers a core feature in Apple’s iPhone lineup, and that’s just one revenue stream. The company serves commercial, government, and defense clients around the globe. Its new strategic agreement with the U.S. Army opens the door to the $40 billion defense communications market. The result? Multiple consecutive quarters of rising sales – the first and most important indicator of a microcap poised to break out.

- Rising Earnings Power

Most microcaps burn cash for years. Globalstar has proven it can generate profits, cover its own operating needs, and reinvest in growth – all without the constant dilutive capital raises that crush shareholder value. The company’s improving bottom line reflects the second microcap benchmark: a clear trajectory of increasing earnings per share, signaling financial strength and operational discipline.

- Deep Undervaluation

Despite Apple’s prepaid capital and infrastructure investments – which have already funded much of its global network expansion – Globalstar trades at a market cap near $3 billion. That figure dramatically understates its intrinsic worth when you factor in its satellite constellation, global ground stations, and multi-year contractual revenues from one of the most valuable companies on the planet. This is the kind of overlooked value Wall Street typically notices only after the biggest gains have already been made.

- Powerful Insider and Institutional Backing

One of the strongest buy signals in microcap investing is when insiders or major institutions commit significant capital. Apple has done exactly that – taking roughly a 20% ownership stake in Globalstar. This is more than a vendor agreement; it’s a strategic, long-term partnership between a $3 trillion tech leader and a high-potential small cap. That kind of alignment is rare… and often a catalyst for explosive upside.

Put it all together, and Globalstar isn’t just a “check the box” story – it’s a microcap that hits every one of the proven criteria for turning small companies into big winners. With its technology already in millions of devices, a defense market foothold, and an expansion plan fully funded, it’s in the sweet spot where microcaps make their biggest moves.

A Growth Launchpad for Apple’s Satellite Network

So what’s next for Apple’s quiet satellite partner? In short… lift-off.

Globalstar is in the middle of the most significant expansion in its history. At the heart of this is a constellation refresh – 17 brand-new satellites (built by Canadian company MDA Space Ltd.) are already under order, with the option to add nine more. These next-generation satellites are scheduled to begin launching in the fourth quarter of 2025.

The modern, high-capacity network will be ready to serve Apple and other clients for years to come.

But the upgrades aren’t just in orbit…

Globalstar is also expanding its global ground infrastructure. It’s adding new gateway stations – which connect the orbiting Globalstar satellites to telecommunications networks here on Earth – and upgrading existing sites to improve coverage, reduce latency, and boost throughput. This will allow the company to serve more users simultaneously and deliver faster, more reliable connections in remote areas.

The impact of these rollouts on the bottom line could be transformative.

Management expects 2025 revenue to more than double once the new satellites and upgraded ground systems are fully online – a forecast supported by locked-in demand from Apple and growing interest from additional enterprise and government customers.

Globalstar isn’t just growing. It’s scaling with a built-in anchor client, fully funded infrastructure, and years of service revenues already booked. For a microcap investor, that combination is rare, and potentially very lucrative.

Recommendation: Buy Globalstar (Nasdaq: GSAT) at market.