TABLE OF CONTENTS

Recession or Not, This 5.3%-Yielding Perpetual Dividend Raiser Will Perform

By Marc Lichtenfeld • Chief Income Strategist • The Oxford Club

In the September Federal Reserve meeting, interest rates were held steady, but the Fed stated that elevated rates may be in place for longer than expected to fight inflation.

That can be interpreted two ways.

The “glass half full” folks see the higher rates and inflation as proof that demand and the economy are strong – a sentiment I agree with and talked about in last month’s issue of The Oxford Income Letter. And last month’s recommendation of Capital Southwest Corp. (Nasdaq: CSWC) should do well in a higher rate environment, as it can lend money to growing businesses at those higher rates.

Those in the “glass half empty” camp – which seems to be much of the population, including most experts – believe that higher rates will send the U.S. economy careening into a recession.

But The Oxford Income Letter’s portfolios are built for the long term to handle all kinds of economic conditions. And today’s recommendation does just that.

It’s strong in good times and recession-resistant in bad times.

The Best REITs

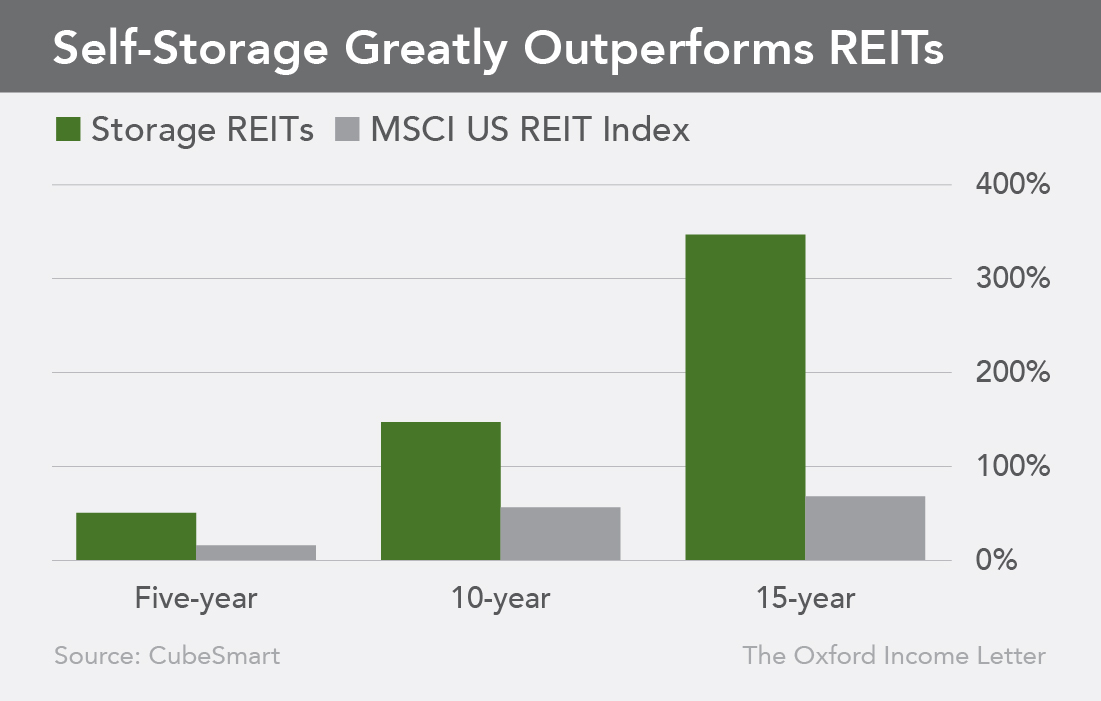

In commercial real estate, nothing comes close to the self-storage sector in terms of outperformance and being able to weather downturns in the economy.

In fact, during the Great Recession, commercial real estate stocks fell anywhere from 25% to 67% depending on the sector. Self-storage actually gained 5% in 2008. And over the long term, self-storage blows away all other real estate investment trusts (REITs).

And despite calls for recession, the self-storage market is expected to grow 7.5% per year through 2027.

It makes sense. When times are good, people accumulate more stuff. That pushes older possessions to storage facilities because no matter how many times we’re asked, we’re not throwing away our high school championship trophies.

Also, housing booms lead to homebuyers waiting to move into their newly built houses, often storing furniture and other items temporarily. And when the market turns south, some folks need to downsize their homes and move some of their belongings into storage.

Because it’s a low-cost industry, self-storage needs an unusually low 60% occupancy rate to be profitable. And unlike the eviction process for landlords, which can take months or longer, eviction in self-storage is quick. If the renter doesn’t pay, the facility auctions off the contents of their space.

(Storage Wars is a reality TV show that follows bidders as they try to find treasure in these units with only a cursory look at what’s inside.)

My favorite stock in the space is CubeSmart (NYSE: CUBE). The company owns or operates 1,338 facilities in 171 markets in 41 states. It has more than 750,000 customers. But what I especially like is that 89% of its portfolio is in the top 40 largest markets.

Despite the return to office not gaining momentum and crime rates rising in big cities, people are no longer fleeing urban areas the way they did during the pandemic.

New York City, CubeSmart’s largest market, saw its population grow last year.

In the most recently reported quarter, same-store sales in New York City grew 7.1%, while those in Houston grew 12.1%, Chicago’s grew 13.1% and San Diego’s grew a whopping 15.7%. New York is the most undersupplied top 31 market, and new supply is expected to be tight due to legislation and zoning changes. In fact, the New York boroughs of Queens, Brooklyn and the Bronx have the lowest national square foot of storage supply per capita at 2.7. The national average is 7.6.

Additionally, small and midsize businesses have turned to self-storage for mini-warehousing.

All of this means healthy cash flow growth.

Funds from operations (FFO), the cash flow metric used for REITs, are expected to grow 6% per year through 2025, which is above its peers’ growth rates.

Management Excellence

CEO Christopher Marr has been at the helm since 2014 and has been with the company since 2006. Marr is part of a disciplined management team.

There are many acquisition opportunities, as 73% of storage facilities are owned by small operators and only 18% are owned by public companies and REITs. So with never-ending pressure to grow, a lot of companies just buy… buy… buy…

Not CubeSmart.

On the most recent quarterly conference call, Marr said…

Currently, many of the acquisition opportunities available in the market are of inferior quality and would be dilutive to our current portfolio quality. As a result, we are being patient and disciplined, waiting to deploy capital until we are confident in the ability to realize attractive risk-adjusted returns.

But talk is cheap. Let’s look at performance…

-

- Operating margin has grown – it was 25.7% in 2021 and is expected to hit 38.4% next year.

- Over the past five years, FFO has grown 59%.

- Capital expenditures have plummeted from $468 million in 2020 to an expected $31 million this year.

- The occupancy rate this year is 92.7%. Remember, on average, the industry needs only around 60% occupancy to turn a profit.

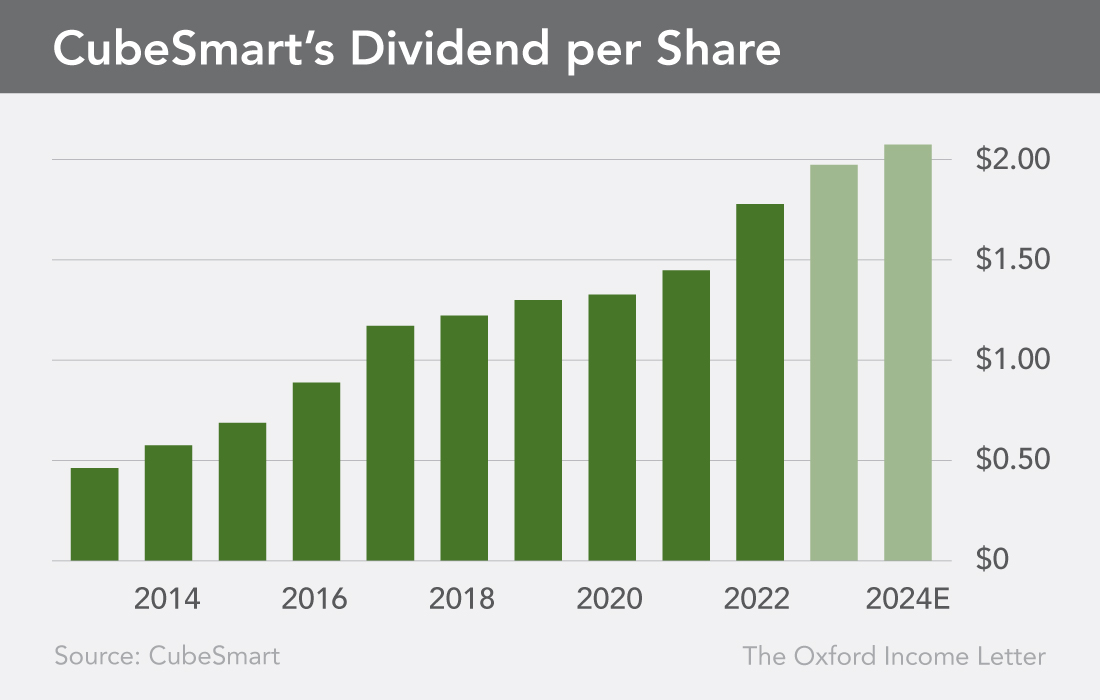

And the dividend has grown an average of 16.6% per year for the past decade versus just 2.4% for the sector average.

The current dividend is $0.49 per share, giving the stock a nice 5.3% yield, but we should see an increase in the first quarter of next year.

A Screaming Bargain

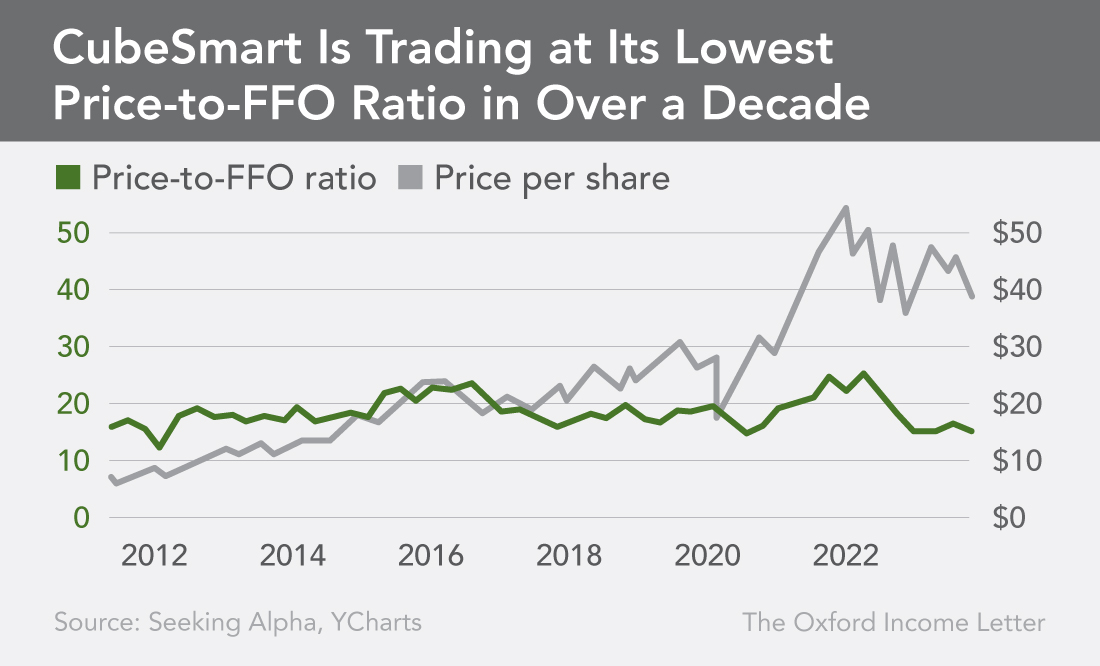

Not only is talk cheap, but so is the stock… Other than when the market plummeted at the beginning of the pandemic in March 2020, CubeSmart is trading at its lowest price-to-FFO ratio in more than a decade.

Since then, the stock rose more than 400%, but it’s down about 35% from its highs in 2021.

And with an $8.5 billion market cap, CubeSmart is much smaller than its competitors like Public Storage (NYSE: PSA), which has a $46 billion market cap, and Extra Space Storage (NYSE: EXR), with its $27 billion market cap. That gives CubeSmart plenty of room to grow and makes it an attractive acquisition candidate – especially if those competitors want more exposure to New York and other major metropolitan areas.

CubeSmart is exceptionally good at running its business in good times and bad, has a terrific dividend-raising history, and is historically inexpensive.

Regardless of whether the economy goes up or down (and it will), CubeSmart will continue to attract customers and maximize returns for shareholders.

Action to Take: Buy CubeSmart (NYSE: CUBE), and add it to the Compound Income Portfolio. Place it in a tax-deferred portfolio if possible.

Small Cap Preview

It’s Time for a Small Cap Rally

By Jody Chudley • Contributing Analyst

For the past decade, the market has been dominated by large cap growth stocks.

Between December 31, 2012, and December 31, 2022, the Russell 1000 Growth Index (which is made up of large cap growth stocks) outperformed the Russell 2000 Growth Index (which is made up of small cap growth stocks) by nearly 5% per year.

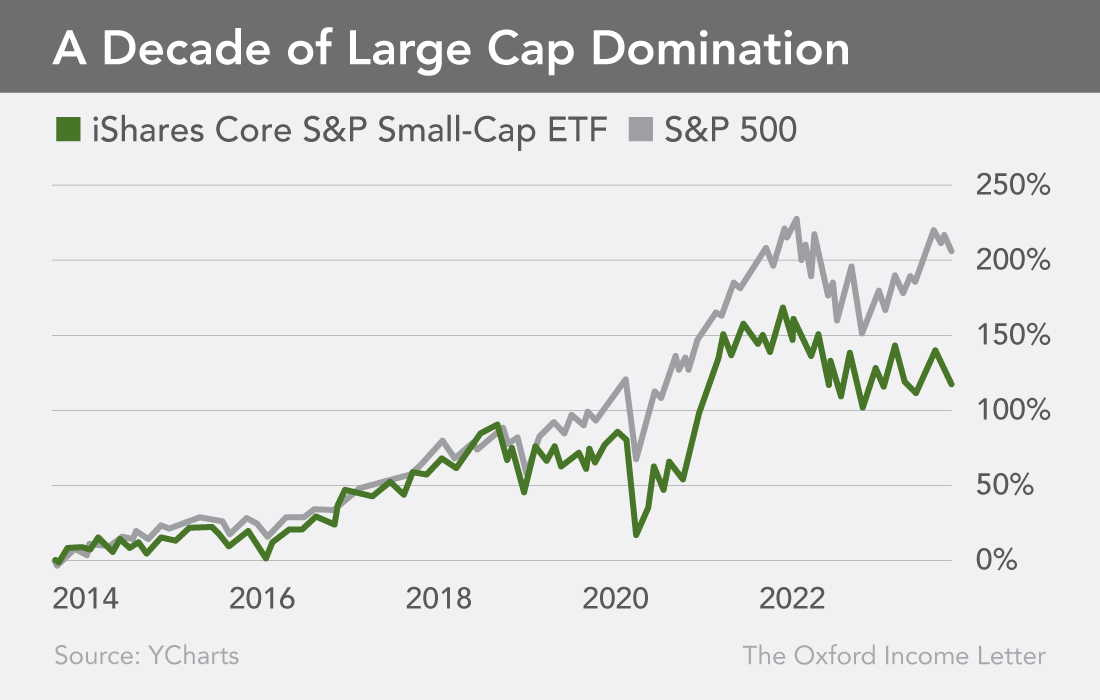

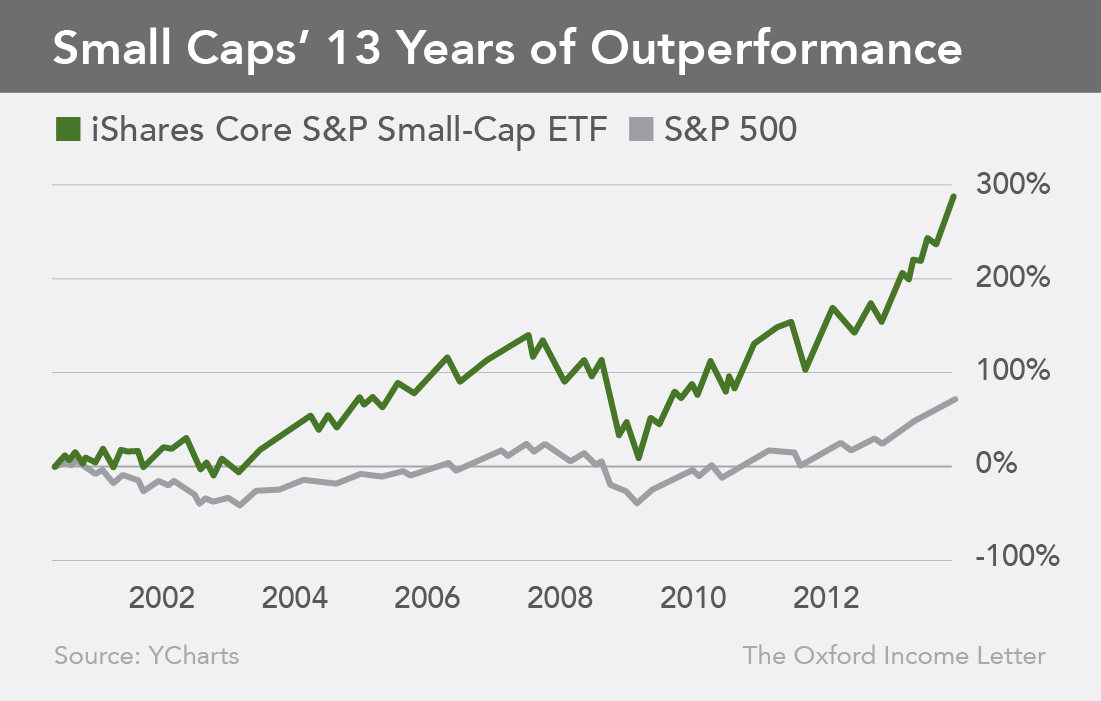

And it hasn’t been among just growth stocks that large caps have dominated. The chart below compares the total 10-year return of the iShares Core S&P Small-Cap ETF (NYSE: IJR) with that of the large cap-heavy S&P 500.

These two indexes include growth and value stocks, and the chart shows that large caps have had a terrific run.

Given this long-term outperformance from large cap stocks, you won’t be surprised to learn that – right now – small caps offer an attractive value proposition.

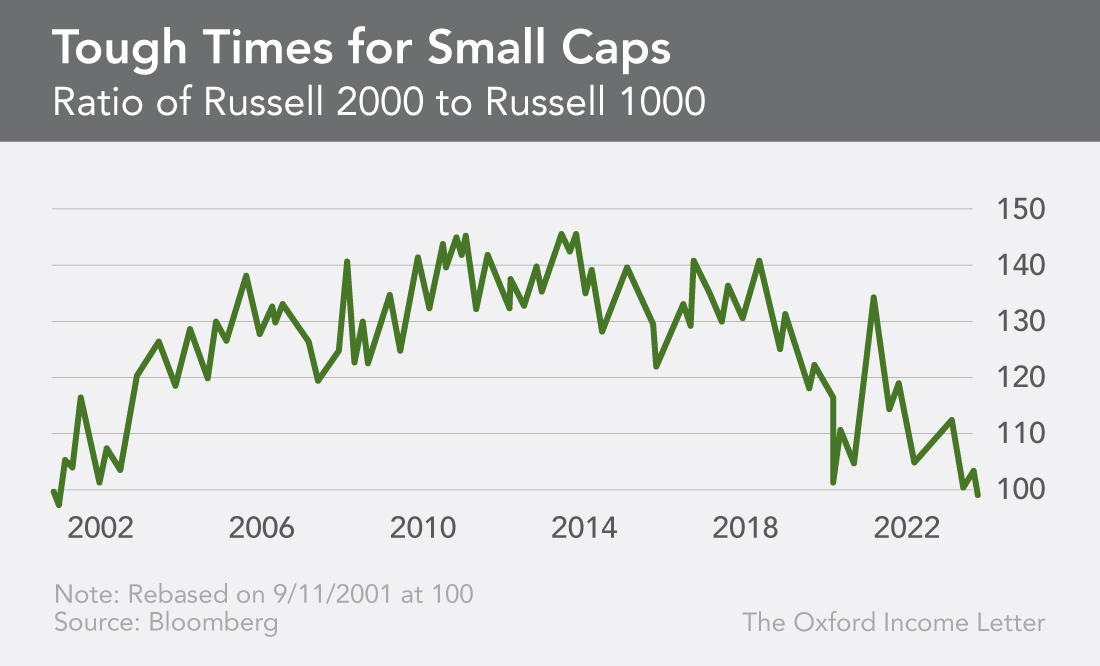

The ratio of the Russell 2000 (which is composed of small cap stocks) to the Russell 1000 (which is composed of large cap stocks) is currently at a 22-year low. We haven’t seen small caps this inexpensive relative to large caps since the turn of the century.

Interestingly, the last time the ratio hit this level was one of the best moments in history to pick up small cap bargains.

Beginning in 2001, small caps outperformed large caps by more than fourfold over the following 13 years.

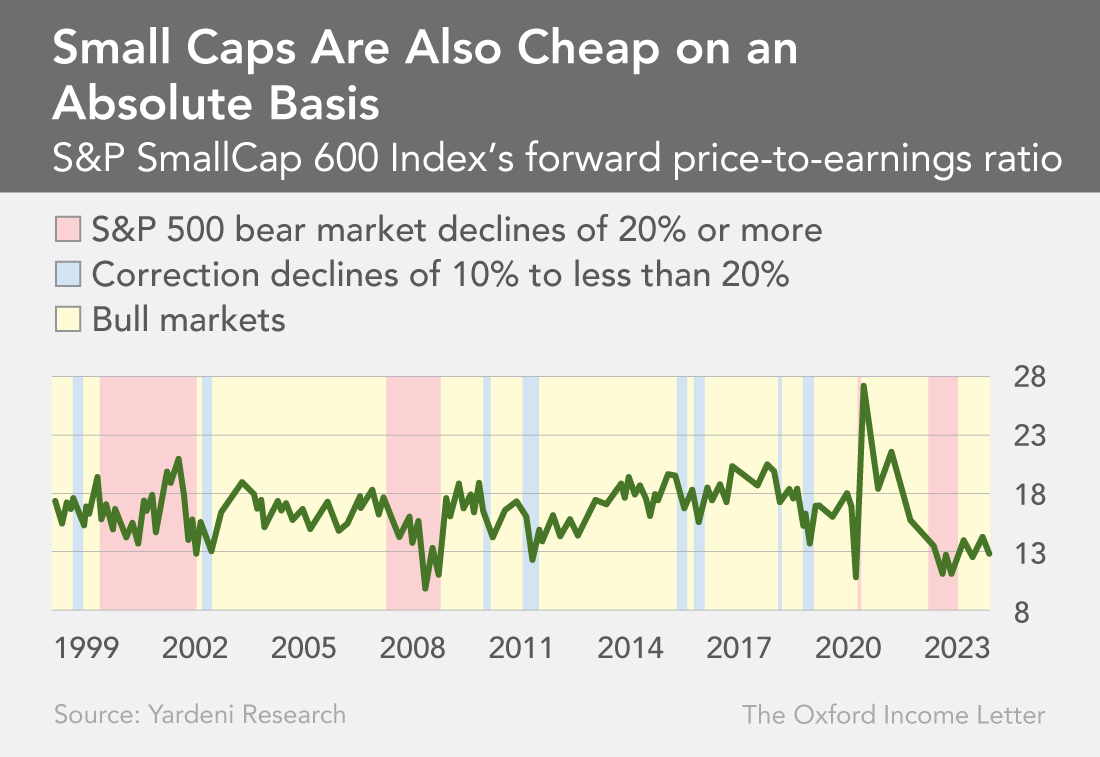

Also, it’s important to note that small cap stocks aren’t cheap only relative to large caps. They’re cheap on an absolute basis as well.

With a forward price-to-earnings (P/E) ratio of 12.6, small cap stocks, as represented by the S&P SmallCap 600 Index, have rarely been less expensive.

The only two times this index has traded at a lower forward P/E ratio in the past 20 years were at the bottom of the financial crisis in 2008 and during the COVID-19 crash in March 2020.

Those were another two moments when buying small caps paid off incredibly well.

The case for small caps is already convincing, yet there is even more data that supports stocking up on small caps now.

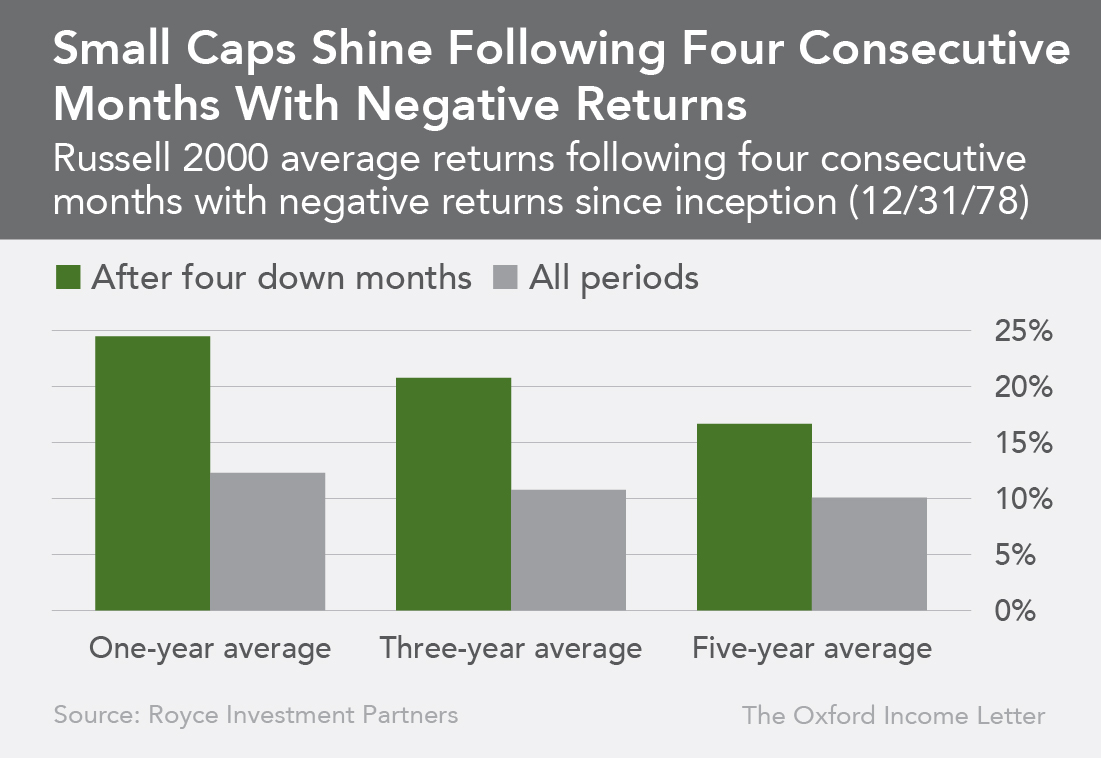

Earlier this year, the Russell 2000 Index declined in value over four consecutive months. This is an extremely unusual occurrence.

Since the Russell 2000 was created in 1984, it has gone down in four consecutive months only eight times.

And the returns for the index coming out of these drops have been exceptionally strong. One-year returns have averaged 24.7%, three-year returns have averaged 21% and five-year returns have averaged 16.8%.

The recent four-month decline of the Russell 2000 suggests that small caps could be ready for another long run of strong performance.

While large caps are rather expensive at the moment, small caps offer an almost historically attractive value.

It is no wonder, then, that Marc recommended shares of small cap business development company Capital Southwest Corp. (Nasdaq: CSWC) in last month’s Oxford Income Letter.

And Marc doubled down on small cap dividend payers at The Oxford Club’s Private Wealth Seminar at Lake Tahoe just a few weeks ago.

The stock market moves in cycles. Large caps have had the lead for an unusually long time. I believe that a small cap surge is near, and the valuation data supports that belief.

There are plenty of small cap businesses that now offer solid dividends, great balance sheets and very attractive valuations. Income investors should take note and get their portfolios ready.

Fixed Income Investing

A Rare Occurrence…

A Shift Is About to Take Place in the Bond Market

By Marc Lichtenfeld • Chief Income Strategist

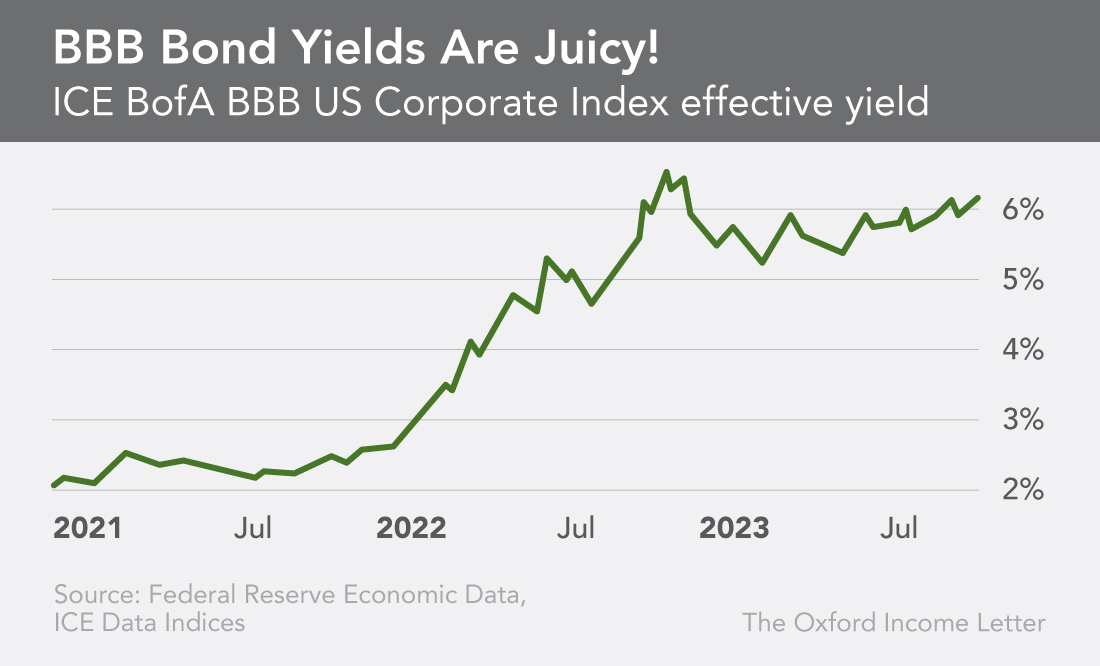

We’re currently seeing the best investing opportunity in investment-grade corporate bonds in my 16 years at The Oxford Club.

In fact, the current average yield on these bonds is 2 percentage points higher than their average yield since 2010.

“Investment grade” refers to corporate bonds that are rated as being BBB- quality or better by the bond rating agencies. These bonds have the lowest risk of default. Bonds rated below BBB- are referred to as non-investment grade.

The entire BBB rated investment-grade bond class is now yielding more than 6%.

We haven’t seen yields like this from high-quality companies since the global financial crisis.

The current economic climate is obviously nothing like 2008 and 2009. Our economy is doing just fine.

Despite everyone’s fears of recession, unemployment is near record lows, wages and productivity are rising, and more dollars are being invested in the U.S. by overseas companies than ever before.

The risk of investing in anything was exponentially higher during the financial crisis because we were on the verge of our entire financial system failing.

Yet here we are today able to lock in similarly attractive bond yields from rock-solid companies in a stable economy.

These bond yields are a gift.

Inflation Isn’t Completely Under Control – But It’s Close

There’s more to this bond story than just the attractiveness of current yields.

Where we are in the Federal Reserve’s interest rate hiking cycle also offers us an opportunity to play both offense and defense with our investments.

It allows us to purchase high-quality investment-grade bonds yielding 6% or more in a solid economy and know that our worst-case scenario is that we’ll earn a generous income stream.

These companies are going to repay us in full at maturity and make good on all scheduled interest payments.

Inflation is still too high, and I suspect we could see another rate hike or two. However, we are unquestionably getting close to the end of this rising rate environment.

Should the economy start to struggle, rates will come down. If that happens, the bonds we’re purchasing today are going to make good on their contractually obligated payments to us and the market is going to bid up the prices of those bonds so that we end up with some capital gains.

If you own a bond yielding 6% and interest rates drop next year, an equivalent bond may then yield 5%. So your 6% bond will jump in price because it’s more desirable.

Eventually, it will rise in price enough to yield 5% – for someone else. Yet you’ll still earn 6% until maturity, or you could sell the bond for a profit.

That’s why we’re in a win-win environment for bonds.

If rates keep rising or stay the same, we’ll earn the high yields we are locking in today. If rates fall, we’ll have a chance to realize some capital gains.

Remember, bonds are called fixed income assets.

The interest won’t vary; it will stay fixed. If rates drop, you’ll continue to earn the same yield as you did the day you bought the bond. So today’s bond yields may be even more attractive in a year or two if interest rates decline.

Now Is the Time to Buy Corporate Bonds

I’m bullish on corporate bonds because yields are high and the rate hiking cycle is nearing an end.

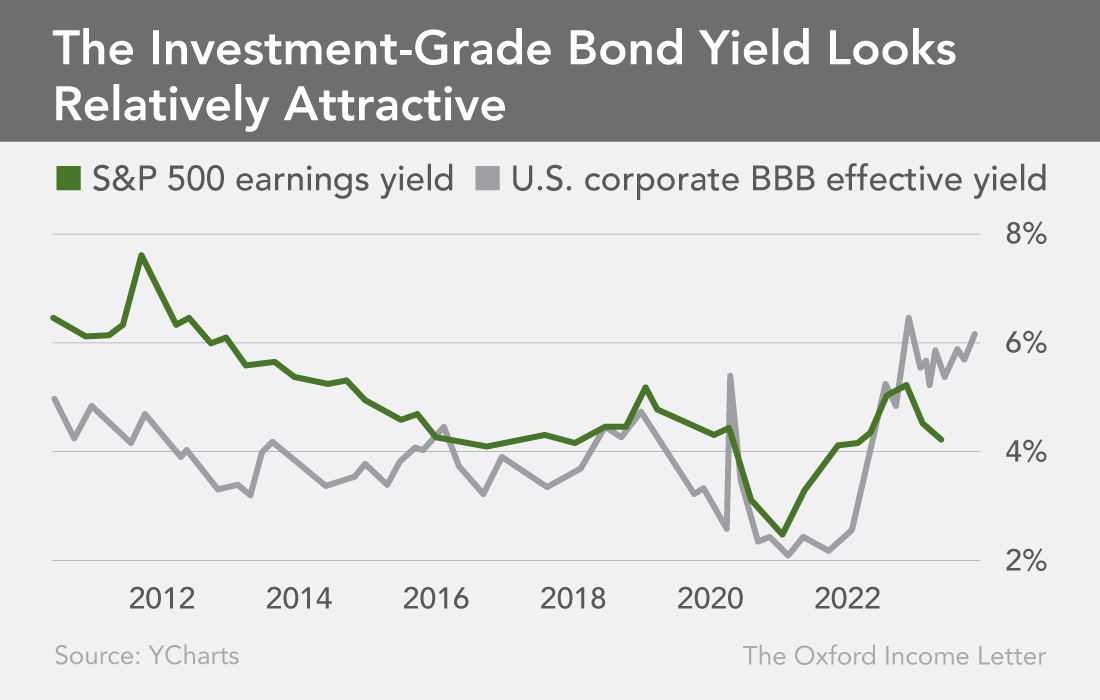

There is one other key reason for my bullishness… Relative to stocks, corporate bonds are attractively valued.

A key metric that I use to assess the relative valuation of bonds versus stocks is the yield of investment-grade bonds versus the earnings yield on the S&P 500.

The earnings yield is the total earnings for the S&P 500 companies divided by their total market capitalization.

The S&P 500 earnings yield is cumulative of all 500 companies in the index. It is the inverse of the price-to-earnings ratio.

Currently, the earnings yield on the S&P 500 is 4.26%. That is almost 2 percentage points lower than the 6.15% yield being offered by BBB rated investment-grade bonds.

As you can see, for most of the past decade, investment-grade bond yields haven’t been significantly above the S&P 500 earnings yield.

We had a blip higher in bond yields during the COVID-19 crash in the spring of 2020, but for the most part bond yields have been considerably lower than the S&P 500 earnings yield.

Now the bond yield line is well above the S&P 500 earnings yield line. This is a rare occurrence and likely suggests something is about to change.

That means you absolutely need bonds in your portfolio, not only for income but to provide some upside should stocks fall.

Snapshot

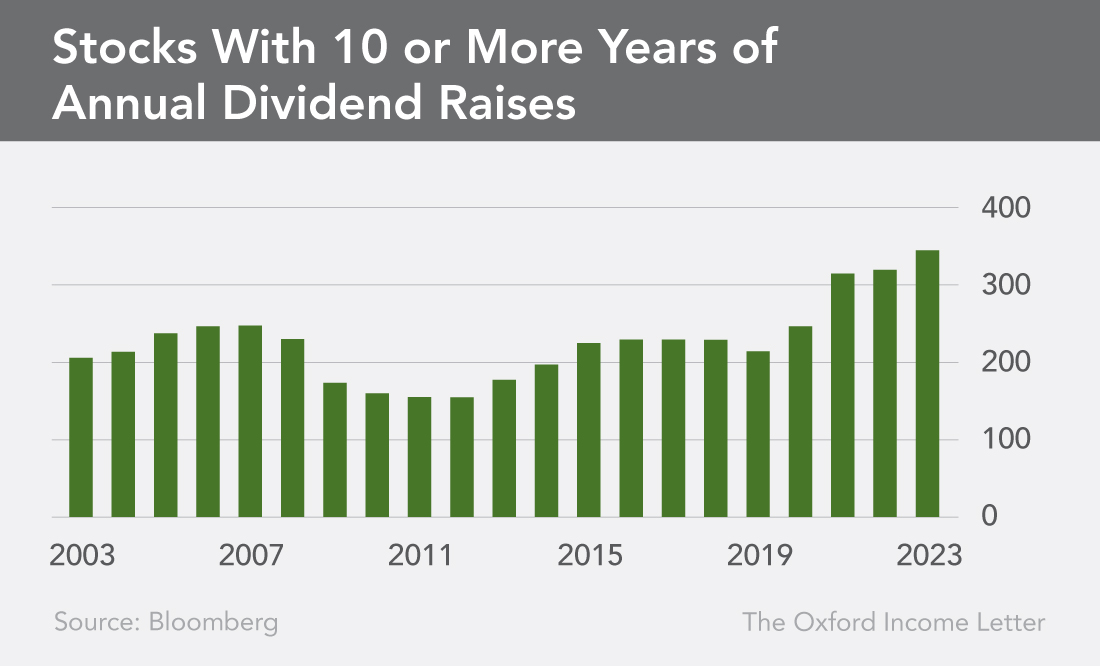

A Record Year for Perpetual Dividend Raisers

By Kristin Orman • Research Director

While all of the major indexes are up for the year, last month’s volatility has left many investors frustrated.

Despite September’s choppy market conditions, it’s still a great time to be an equity investor. And it’s an even better time to be a dividend investor.

There have never been more dividend-paying companies to choose from.

As this month’s snapshot shows, the number of 10-year dividend growers is the highest it’s been in two decades.

Today, there are 342 stocks with a 10-year or longer track record of raising their dividends. This means these companies have raised their dividends each and every year for the past decade or more.

That’s more than double the 150 companies that had a 10-year-plus streak of dividend raises back in 2011. That’s when Marc began working on his bestselling book Get Rich with Dividends and began writing about Perpetual Dividend Raisers.

Perpetual Dividend Raisers are stocks that raise their dividends year after year.

Companies with an established track record of raising their dividends every year will continue to do so unless it becomes absolutely impossible. Management knows that investors have come to expect a dividend increase every year. Any change in that policy could cause investors to abandon their shares.

Investing in Perpetual Dividend Raisers is an easy way to grow your income stream and generate wealth.

This month’s recommendation, CubeSmart (NYSE: CUBE), is a great example. The self-storage real estate investment trust has grown its dividend by 332% over the last 10 years, from $0.46 per share in 2013 to a projected $1.99 per share this year.

AbbVie (NYSE: ABBV) is another all-star Perpetual Dividend Raiser. When Marc recommended the biotech company in the Compound Income Portfolio in 2016, AbbVie paid a dividend of $2.35 per share. This year, AbbVie’s dividend is expected to come in at $5.91 per share.

Even better, Perpetual Dividend Raisers are also resilient during bear markets. They can be great hedges against inflation.

Here’s how…

If a stock is yielding 4.3% today and raises its dividend by 10% every year, you’ll receive a yield of 10% on your cost basis in 10 years.

But if you reinvest those dividends, as Marc suggests in the Compound Income Portfolio, your holdings will yield 15.7% on your original cost in 10 years.

Inflation can take a big bite out of your wealth, but it’s nice to know that there is an increasing stable of dividend growers to help you battle it.

Marc’s mailbag

We believe it’s helpful to share questions and clarifications on dividend investment strategies with all of our subscribers. Keep in mind, Marc can answer your general strategy and service questions, but he cannot give personalized advice. As always, feel free to send us your questions at mailbag@oxfordclub.com.

Q. Marc,

Apart from the recommendations in The Oxford Income Letter’s Fixed Income Portfolio and Compound Income Portfolio, I’ve purchased U.S. Treasury bills and Series I bonds as recommended. These investments let me sleep well at night.

Regarding U.S. Treasury bills, is the interest taxable when they mature, whether purchased from TreasuryDirect or in a Roth IRA brokerage account?

And is there an advantage of buying from TreasuryDirect instead of a brokerage account? – Pauline P.

A. U.S. Treasury bills are taxable on a federal level but are exempt from state and local taxes. If the bonds are in a Roth IRA, you will not pay any tax on the interest.

If your broker charges a commission or marks up the bonds (buys them at one price and sells them to you at a higher price), it may be cheaper to buy them through TreasuryDirect. Ask your broker about their policy regarding Treasurys. If there is no difference in price or commission, then there is no advantage one way or the other.

Q. What are the essential pros and cons of buying a callable AA+ bond with a yield to maturity of 6.28%?

If it’s callable, can I cash it in early? – Kim

A. If a bond is callable, that means the company can call, or pay off, the bond early. But it can’t just do it anytime it wants. There is usually a schedule of dates and prices when a company may call the bond.

For example, let’s say a bond is issued in 2023 and matures in 2028. The company may be allowed to call the bond starting on October 1, 2025, for $102 ($1,020). There is often a premium paid for calling a bond early. On October 1, 2026, the callable price may drop to $101 ($1,010). On October 1, 2027, the call price may be $100, or par value ($1,000).

This means between October 1, 2025, and September 30, 2026, if the company calls the bond, it will pay bondholders $1,020. Between October 1, 2026, and September 30, 2027, bondholders will receive $1,010. And starting on October 1, 2027, they will get $1,000.

The call dates and prices are in the bond’s prospectus.

If a bond is callable, the company has the right to call the bond. If it is called, it is done so automatically and the bondholder cannot continue to hold the bond. It is the company’s decision whether to call the bond.

Bondholders do have that right when there is a tender offer. That’s when a company offers to buy back the bond, often, though not always, at a premium.

For example, if a bond matures on October 1, 2025, and is currently trading at $975, a company may make a tender offer at a price of $980. The bondholder could choose to surrender their bond in exchange for $980 or opt to hold until maturity, when they’ll receive the $1,000 par value.

If the bond is called, the company makes the decision. If there’s a tender offer, it’s the bondholder’s choice.

Q. Regarding the recommendation of Capital Southwest Corp. (Nasdaq: CSWC), you indicated that it is planning to raise more capital (equity) soon. Isn’t that likely to involve selling more common shares and diluting the value of any that we would buy now? Isn’t that a reason to wait until that event occurs? – James B.

A. Normally, the answer would be yes. If we were looking at a biotech stock or another unprofitable company that is raising money to fund its business, we’d want to wait until after the dilutive event occurs.

With cash flow-positive business development companies (BDCs) and real estate investment trusts (REITs), the capital they raise in a stock offering is usually put right back into cash flow-generating investments. So while the share count will increase, cash flow will grow as well.

If the members of the management team are worth their paychecks, the newly raised funds will fuel a higher rate of cash flow growth than share count growth.

It’s very common for BDCs and REITs to offer stock in order to raise capital for these purposes.