The markets are in turmoil.

We’re mired in the worst fourth quarter in seven years.

And we’re not having roller-coaster weeks… we’re having roller-coaster days. The Dow Jones Industrial Average is experiencing several hundred-point swings nearly every session.

There’s unease, uncertainty and even some panic.

We hit a couple of stops this week on Quidel (Nasdaq: QDEL) and Kornit Digital (Nasdaq: KRNT).

But four of our seven open positions are up double digits!

Shares of our Chinese e-commerce platform, Baozun (Nasdaq: BZUN), are already up nearly 10% since we got in at the end of November.

Our shares of the dividend-paying marijuana play, Innovative Industrial Properties (NYSE: IIPR), are up almost 20%. The flight to safety, not just in the cannabis space, is buoying our position.

Plus, The Trade Desk (Nasdaq: TTD) is defying the tech sell-off with our shares up more than 10%. And then our 5G play, Keysight Technologies (NYSE: KEYS), is holding strong, up more than 37%.

Not to mention, we also have a single-digit gain on our cybersecurity play, CyberArk Software (Nasdaq: CYBR).

So we continue to hold strong despite the weakness in the broader markets. And our strategy of focusing on high-growth companies that are outpacing their peers is putting profits in our pockets while other investors struggle with declines.

Today, I have another such gem for you to act on…

New VIPER Recommendation!

On Thursday, ailing General Electric (NYSE: GE) got a massive boost as the company announced it was spinning off its digital assets to establish a dedicated Internet of Things company.

This is a big step for the General, which got soft around the middle in recent years with its fingers in too many pies.

But Internet of Things is just one of the areas we like to focus on here.

The other is cloud and big data.

The more things connected to the internet and one another, the faster and more robust the connections need to be.

Consider that in 2016, the industrial Ethernet market was valued at roughly $20 billion.

By 2024, it’s expected to top more than $72 billion.

That’s a 260% increase.

And there’s one company perfectly positioned to snag the lion’s share of profits… Mellanox Technologies (Nasdaq: MLNX).

The company develops hardware and software products that allow computers to share data. As we know, this is an enormous market.

More importantly, though, Mellanox is also a leading supplier of Ethernet products, especially high-speed ones that are coveted by companies like Alibaba (NYSE: BABA).

Now, here’s why that’s a big deal…

If you use any sort of internet connection (not just an industrial one), you’re likely using one of Mellanox’s products. And you might not even know it.

This market is the main engine of Mellanox’s growth.

In the third quarter, the company’s Ethernet business grew by 59% year over year.

At the same time, Mellanox saw its market share in the high-speed Ethernet market rise to 69%, even as the market doubled in size over the past year.

This puts the company far out in front of its peers, including even tech giants such as Intel (Nasdaq: INTC) and Cisco Systems (Nasdaq: CSCO).

And Mellanox continues to demonstrate faster growth than its competition does.

In the third quarter, it reported that revenue jumped 23.7% year over year. Its peers managed to post revenue growth of just 14.3%.

Mellanox reported third quarter earnings per share of $1.33. This not only was an 87% year-over-year increase but also exceeded the analyst consensus of $1.20 by nearly 11%.

But the momentum doesn’t stop there…

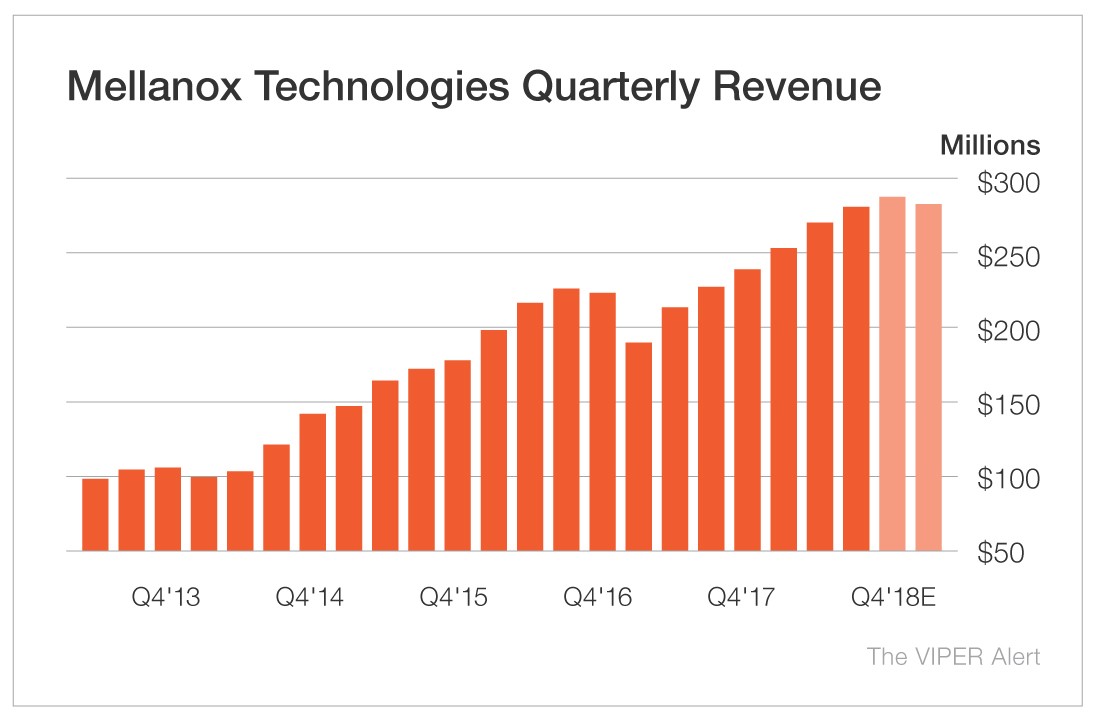

In the fourth quarter, the company is expected to generate $285.2 million in revenue. That’s a 20% increase over the fourth quarter of 2017. Plus, it’s projected to see a massive 219.7% increase in earnings to $71.3 million.

Last year, Mellanox reported revenue of $846 million. This year, I’m looking for revenue to surge at least 25.5% to more than $1.1 billion.

But I see the company’s growth continuing far into the future.

Already, Mellanox is outperforming its industry and the market, and it is a perfect complement to last week’s recommendation, cloud and data lake storage play Attunity (Nasdaq: ATTU).

So let’s go over what the VIPER System looks at…

Value: Shares of Mellanox are a little more than 9% below their 52-week high of $99.14. The company has a price-to-book ratio of 4.05, which is lower than its peer average of 6.29. And it has a price-to-sales ratio of 4.71, just slightly above its peers’ 4.60. But Mellanox has profit and operating margins twice that of its peer average.

Income: Non-GAAP income from operations has increased more than 90% in the last three quarters.

Profits: Mellanox’s trailing price-to-earnings (P/E) ratio is 35.98, which is lower than its peer average of 36.81. But the company’s forward P/E is 15.8. Remember, we’re always looking for forward P/E to be lower than trailing P/E.

Earnings: Net income per share has set records recently. And it has risen more than 87% in each of the last three quarters.

Revenue Growth: Revenue has increased more than 24% in each of the last three quarters. In the fourth quarter, revenue is projected to jump at least 20% to $285.21 million.

V Score (VIPER Score): 78.04. As a reminder, we’re always looking for a score between 70 and 100. So this is a very strong score. This is also considerably higher than its peer average V Score, which is in the “don’t buy” range.

Action to Take: Buy shares of Mellanox Technologies (Nasdaq: MLNX) at market. Use a 25% trailing stop to protect yourself. Speculators may want to look at the March $105 calls. The last trade here was $2.50. The current bid-ask is $2.00 to $3.50. Be patient. Go as low as possible. And don’t pay more than the ask.

Good investing,

Matt

To view the current VIPER Alert portfolio, click here.