ANNUAL FORECAST ISSUE

TABLE OF CONTENTS

Position Your Portfolio Now for “The Big Reversal” in 2026

Overhyped Names Will Fade... and These Low-Risk Plays Will Soar

Alexander Green, Chief Investment Strategist, The Oxford Club

Are you ready for my big investment prediction for 2026? I expect the return of rational investing.

Growth stocks have had an extraordinary run lately. But valuations – as I’ve been warning for weeks now – look more than a little extreme.

Just eight stocks – Nvidia, Amazon, Alphabet, Meta Platforms, Apple, Tesla, Microsoft, and Broadcom –make up an astonishing 40% of the total market cap of the S&P 500.

Yes, these are excellent companies and their market dominance is unlikely to end soon. However, they are expensive stocks whose prices reflect not just optimistic but sky-high expectations.

Meanwhile, the case for value stocks – as I’ll explain shortly – looks more compelling than ever. I expect a major market reversal in 2026, with value stocks substantially outperforming the growth sector.

And I have a great new way to play it. It’s a major pharmaceutical leader that is unloved, undervalued, and set for prodigious profit growth in the year ahead.

The stock trades at a single-digit earnings multiple, yields almost five times as much as the S&P 500, and offers minimal downside risk.

That’s just the combination we look for – and the reason why it’s the newest addition to our Oxford Trading Portfolio.

Primed to Outperform

Investors have made a lot of money over the past two decades by zeroing in on companies that lead the market in sales and earnings growth. Yet it will surprise many to learn that, over the long haul, value stocks have outperformed growth stocks, often by a wide margin.

From 1926 through the early 2000s, value stocks – defined as companies trading at lower price-to-earnings, price-to-book, and price-to-sales ratios – consistently beat growth stocks on a risk-adjusted basis.

Even after factoring in the last 10 to 15 years – when growth clobbered value – value stocks still hold a long-run edge. (My colleague Kristin Orman has more to say on this important subject in the Building Wealth column that follows.)

According to data from Dimensional Fund Advisors, over the last 98 years U.S. value stocks outperformed U.S. growth stocks by roughly 2.5 percentage points a year on average.

That difference may not sound dramatic, but compounded over decades, it’s the difference between a solid return and mind-boggling wealth.

From 2009 to 2021, growth stocks – led by names like Apple, Amazon, Microsoft, and Nvidia – benefited from zero-interest-rate policies, massive liquidity from central banks, the rise of the digital age, and investors’ appetite for disruption.

These conditions created the perfect storm for growth dominance, and the spread between growth and value performance has reached historic levels. Yet that outperformance comes at a cost: valuation risk. Simply put, investors are paying extreme prices for future earnings – assuming they will arrive consistently, on time, and at scale.

History shows that market leadership rarely stays fixed. The Nifty Fifty dominated the 1970s. Tech stocks ruled the late ’90s. Then came energy and financials in the 2000s. And the FAANG era in the 2010s.

Now, after years of dominance, many growth names are priced for perfection. Even minor earnings misses could lead to major drawdowns. Meanwhile, companies with strong balance sheets, low debt, and consistent dividends are well positioned to outperform in a market that is set to reward stability and cash flow over hype and narrative.

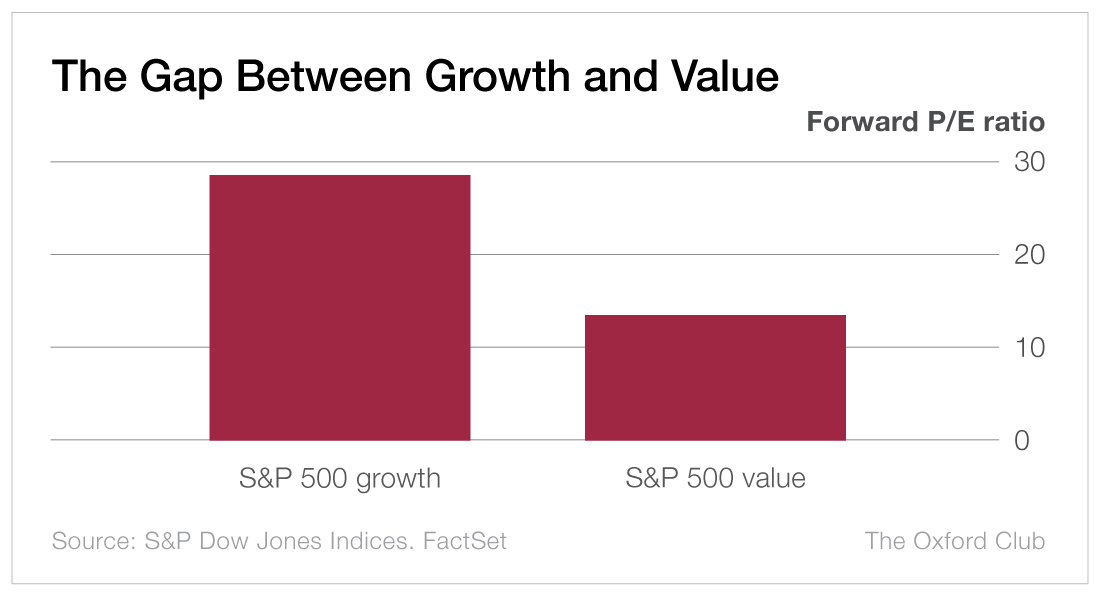

The forward price-to-earnings ratio for growth stocks in the S&P 500 is more than double that of value stocks in the index. That kind of disconnect sets the stage for a serious reversion to the mean. Value stocks don’t need heroic assumptions to outperform.

Many are already profitable, generate free cash flow, and return capital to shareholders via dividends and buybacks.

In short, you’re paying less for greater certainty. As Warren Buffett famously noted, “Price is what you pay. Value is what you get.” And right now, Bristol Myers Squibb (NYSE: BMY) is an exceptional value.

Value Wins Over Time

Founded in 1887 and based in Princeton, New Jersey, Bristol Myers is one of the world’s leading biotech companies, with products for oncology, cardiology, immunology, hematology, neuroscience, and other areas.

Big Pharma offers investors a big opportunity... and a big challenge. The opportunity is that firms can create new lifesaving drugs that generate billions in sales and profits. The challenge is that the patents on those drugs typically expire in 20 years. Competition from generics entering the market quickly erodes demand and rolls back years of success.

That’s exactly what has happened with Bristol recently. It is experiencing a sharp drop in sales for Revlimid, a leading treatment for multiple myeloma that lost patent protection in 2022.

Other Bristol products approaching a loss of exclusivity include Eliquis (a blood thinner) and Opdivo (an intravenous immunotherapy drug that fights cancer).

In addition, the firm has seen failed clinical trials for some of its experimental drugs and disappointing attempts to expand indications with a few existing drugs.

These negative developments have weighed on the stock, which has dropped 40% over the past three years despite a roaring bull market. But as I continually remind Members, look forward not back. No stock rises or falls in the future based on things that happened months or years ago.

The company’s next generation of therapeutics supports an optimistic outlook. A major 2024 restructuring is about to bear fruit, resulting in $3.5 billion in cost savings in the year ahead. Moreover, the stock sports a ridiculously cheap valuation, making it quite the bargain.

So let’s take a closer look... Bristol has a portfolio of more than 30 products and an extensive pipeline across many fields with unmet needs. Growth products now represent a majority of its business.

Breyanzi has emerged as its newest oncology blockbuster, hitting more than $1 billion in annualized sales in 2025.

The early success of its antipsychotic drug Cobenfy is also promising. The treatment has been approved for schizophrenia – an estimated $17 billion market by 2031 – and is being tested for Alzheimer’s.

The real story here isn’t about Bristol’s fading legacy drugs. It’s about the next wave. Management expects around 15 clinical readouts by the end of 2026, including six new molecules – all in core therapeutic areas like oncology, hematology, and immunology.

The firm has a portfolio of well-timed catalysts that will drive revenue growth for over a decade. So while most analysts fret over the company’s looming patent cliff – we are focused instead on the potential of its current pipeline. One that is likely to be augmented by strategic takeovers.

For example, six years ago I recommended the drugmaker MyoKardia in our Ten-Baggers of Tomorrow Portfolio.

In the Portfolio Update on September 29, 2020, I wrote, “MyoKardia is a prime takeover candidate. Major drug companies need to continually replenish their pipelines with new treatments... Rather than starting drug investigations from scratch, Big Pharma often looks at smaller biotechs’ pipelines and either partners with them or buys them outright.”

Seven days later, I wrote another Portfolio Update with the headline “MyoKardia Soars on Takeover News.” The stock jumped 61% when Bristol agreed to acquire the company for $225 a share, and we locked in a 331% gain on the stock.

Expect plenty more announcements like this in 2026. Even as pricing pressure looms, these high-unmet-need categories remain insulated.

I expect earnings per share to rise from $6.54 in 2025 to $7.30 in 2026. That means the company is currently trading for just seven times projected earnings for the next 12 months compared to 23 times earnings for the S&P 500.

Even pharmaceutical peers like AbbVie, Amgen, Merck, Pfizer, and Sanofi trade with an average forward multiple of 12.5 times earnings.

Plus, Bristol sports a dividend yield of 5%. And with $16.5 billion in cash on its balance sheet and excellent growth prospects, that payout is easily sustainable.

The firm represents an excellent opportunity for 2026 – and it plans to launch at least 10 new medicines by 2030. That will provide multiple catalysts for growth and offset legacy drug declines in oncology, immunology, and cardiovascular disease.

In short, Bristol’s strong growth prospects, low valuation, high dividend, and limited downside risk make an attractive combination.

Action to Take: Buy Bristol Myers Squibb (NYSE: BMY) at market. And use a 25% trailing stop to protect your principal and your profits.

Building Wealth

Why Value Is Your Portfolio’s MVP for 2026

Kristin Orman, Research Director, The Oxford Club

For the last decade or so, investors have been trained to believe there is only one way to win in stocks: Chase whatever is growing the fastest.

As a result, a small group of companies with rapid sales and earnings growth has dominated the major indexes. Now many portfolios rise or fall based on what happens to a handful of popular “must-own” names.

It’s what investors are excited about at the moment. But there’s another story – value – which is what investors are discounting. These companies and their respective stocks have been thrown to the side as broken businesses.

Here’s the thing... Many of these value stocks are far from broken. They’re real companies in steadier industries and often pay higher dividends. Their share prices have simply slipped out of favor. As a result, these stocks trade at lower price-to-earnings, price-to-sales, and price-to-book ratios.

True, when only the recent past is considered, growth looks unbeatable. Over the last decade, U.S. growth stocks beat U.S. value stocks by almost 8 percentage points a year on average – an unusually wide gap by historical standards. But the long-term record tells a very different story.

Looking back to 1927, research using the well-known Fama-French dataset finds that U.S. value stocks outperformed growth stocks by about 4.4 percentage points a year on average. That may not sound dramatic in a single year. But compounded over an investing lifetime, it can mean several times as much wealth.

Periods when growth races ahead have often been followed by long stretches when value quietly catches up and pulls in front. Valuations are a big reason.Today, large cap U.S. growth stocks (Russell 1000 Growth Index) trade at a forward price-to-earnings ratio of about 35.1, while large cap value stocks (Russell 1000 Value Index) trade around 19.5. The gap between them is the widest since the peak of the dot-com bubble.

Investors are paying a rich price for every dollar of expected earnings on the growth side and much less for each dollar on the value side. When starting prices are that far apart, the odds tend to favor the cheaper group over the next five to 10 years.

Income tilts the balance even further. The dividend yield on the Russell 1000 Growth Index is near 0.5%. The yield on the Russell 1000 Value Index is closer to 1.9%. And many individual value stocks pay far more than that. Those extra percentage points of income matter!

Dividends can be reinvested into more shares. They also provide a real cash return even in flat or choppy markets, rather than leaving investors dependent on price gains alone. All of this is happening against a very different backdrop than the one that fueled the last growth boom. Although interest rates are falling, they’re no longer pinned near zero. The cost of capital matters again.

That may not impact companies generating substantial cash today. But high-duration growth stocks – whose value rests heavily on earnings far in the future – are more sensitive to interest rate shifts.

Keep in mind, none of this means that growth is “over” or that investors should abandon innovative companies. But it does suggest that the market is offering better forward odds on the value side right now: lower entry prices, more dependable cash flows, and less need for perfection.

Beyond Wealth

Editor’s Note: With the holidays almost here, many Members are looking for a unique and uplifting gift for family members, friends, and colleagues. An excellent suggestion is Alexander Green’s new book, The American Dream: Why It’s Still Alive... and How to Achieve It. In it, he dispels much of the negativity about modern life in the U.S., not with opinions but with facts. You’ll find an excerpt below.

The Truth About “The Good Old Days”

Alexander Green, Chief Investment Strategist, The Oxford Club

There is a widespread misconception in this country that things were far better for most Americans back in “the good old days.”

A recent Gallup poll asked, “Overall, do you think life in America today is better, worse, or about the same as it was 50 years ago for people like you?” Nearly 6 out of 10 Americans (58%) responded that life was better 50 years ago.

That response shows just how poorly history is taught in our public schools. Especially when you consider that at least 58% of Americans are female, Black, or gay. Conditions were not better for these groups half a century ago.

There is also a strong belief that life was easier for middle-class Americans in the second half of the 20th century because life was more affordable.

Yet this view is based more on nostalgia than on a sober analysis of the facts. Many Americans – especially those from older generations – look back at the 1950s and 1960s as a golden era when one income could support a household, homes were cheap, and college was affordable.

While it’s always tempting to romanticize the past, the idea that Americans in the mid-20th century had a better lifestyle than Americans today just doesn’t stand up to scrutiny.

For starters, Americans were far poorer in 1960 than they are today. Poverty rates were higher, particularly among minorities and rural populations. (And for those who fall through the cracks today, our social safety net is broader and more robust than it was then.)

It’s true that one income could support a household back then – but that income was modest, and luxuries were few. In 1960, median household income was about $5,600, or roughly $57,000 in today’s dollars. That income covered food, housing, medical care, transportation, education, and everything else.

According to the U.S. Census Bureau, median household income today is over $83,700 – a 47% real increase from 1960. And while costs for some things have risen, most essential goods and services have become vastly more affordable when adjusted for hours worked, as I discuss later on in the book.

People also have far more flexibility in how they earn today. Remote work, freelancing, and side hustles allow millions of Americans to create multiple income streams and manage their own schedules – unheard of in the mid-20th century.

Communication in the 1950s and 1960s was limited to landline phones, snail mail, and three network television stations. No internet. No smartphones. No email. No GPS. No videoconferencing. No global connectivity.

Homes built in the 1960s were roughly 25% smaller, and square footage per person was about a third of what it is today. Modern homes are not only larger – they’re better built, better insulated, and filled with appliances and technologies that didn’t exist a generation ago.

In 1960, the average home had no dishwasher, no central air conditioning, and likely just one black-and-white TV. Today’s homes are packed with conveniences: computers, tablets, multiple smart TVs, washers, dryers, microwaves, and HVAC systems that keep us cool in the summer and warm in the winter.

Back then, only about 60% of American households owned a car – and the cars they did have were far less safe, less reliable, and less efficient. Today, there are about 290 million registered vehicles in the United States – more cars than licensed drivers.

Medical technology in the 1960s was crude by modern standards. Antibiotics were still relatively new. There were no MRIs, CT scans, or minimally invasive surgeries. Childhood diseases that are now largely preventable – including measles and polio – were far more common. Cancer detection and treatment were far less effective. Heart surgery was risky and rare.

Life expectancy in 1960 was 69.8 years. Today, it’s just under 79 years. Infant mortality has dropped by over 80%. Most diseases that were deadly or debilitating in 1960 are now manageable – or preventable.

A common lament is that the United States has a lower life expectancy despite spending more on healthcare than other developed countries.

But America also has more chronic disease and drug addiction, which have more to do with poor lifestyle choices than failures in our healthcare system. U.S. cancer survival rates are higher than in most developed countries because Americans have access to more treatments than any country in the world.

College is more expensive today. But it’s also more accessible. In 1960, only 45% of high school graduates enrolled in college. Today, that number is closer to 60%, and a far higher percentage of Americans complete some form of postsecondary education. Grants, scholarships, online degrees, and community college programs have expanded access dramatically.

More Americans than ever before attend college, start businesses, travel internationally, and pursue lifelong learning. The ability to switch careers, reinvent yourself, or learn new skills online was unimaginable in the 1960s.

Jobs back then were often repetitive, physically exhausting, and offered little upward mobility. The modern job market isn’t perfect, but it provides far more opportunity for flexibility, growth, and fulfillment. And for many Americans – especially women, people of color, and gays – the so-called golden age of the 1950s and 1960s was anything but.

Women were expected to stay home. Segregation was the law in much of the country. Gay Americans had to hide their identities at the risk of arrest, assault, or worse.

The idealized “American family” was not just a cultural archetype – it was a narrow, exclusive vision that left out millions.

Today, Americans have far more personal freedom. More legal protections. More opportunity to define family and career on their own terms. That’s progress.

While some elements of mid-century life may seem simpler, they came at the cost of comfort, freedom, and opportunity. Yes, our lives today are more complex. But we have more choices, better tools, and greater control over our destinies.

We have more liberty. More equality. More representation. More access to technology, travel, healthcare, education, information, and global markets than any generation in history.

We are safer, healthier, and, in most measurable ways, richer. In short, the American Dream hasn’t disappeared. It’s evolved. It’s now about building a life that aligns with your values – whether that means starting a business, working remotely, traveling the world, raising a family, or retiring early.

Romanticizing the past may feel comforting. But when we look at the facts – past and present – today’s society offers a better chance than ever to live a fulfilling, empowered life. And isn’t that what the American Dream is all about?

If you’re looking for an optimistic, last-minute Christmas gift for family members and friends, Amazon is currently offering 50% off one book when you buy two at the link above. Order now.

Portfolio Review

Two Secular Winners With Room to Run

Alexander Green, Chief Investment Strategist, The Oxford Club

Trading has turned choppy over the last week, and it’s not hard to discern why. Inflation remains 50% above the Federal Reserve’s 2% target. Hiring has been soft in many industries. And there is uncertainty about whether the Fed will continue cutting interest rates in 2026.

With these uncertainties, my advice is to focus on undervalued opportunities that are likely to lead in the next cycle. A good example is Welltower (NYSE: WELL). I added it to our Oxford Trading Portfolio in the July issue of the Communiqué. Our shares have already gained 39%.

Welltower is a $142 billion real estate investment trust (REIT) that operates at the convergence of three massive industries – housing, healthcare, and hospitality – each of them shaped by one of the most powerful demographic tailwinds of our lifetime: aging.

Unlike most REITs, which function as passive landlords, Welltower runs more like an operating company. It partners closely with healthcare operators, uses data science to improve resident outcomes and occupancy, and constantly reinvests in innovation.

The result? A portfolio that is both stable and built for growth, with approximately two-thirds of revenue coming from senior housing properties, 20% from triple-net healthcare leases, and the rest from outpatient medical and wellness assets. Healthcare real estate was one of the top-performing REIT sectors in 2025.

Why? Because it’s largely recession-resistant.

Whether the economy expands or contracts, older adults still need care. They still need a place to live. And they’re increasingly choosing communities that offer dignity, wellness, and convenience.

Demand is growing, supply is tight, and the best-run properties can raise rents without losing tenants. Welltower is positioned to benefit more than anyone. The company enjoys a 20% operating margin. And I expect earnings per share to rise from $1.82 in 2025 to $2.68 in 2026.

Owning shares of Welltower is investing in the infrastructure of aging. As more Americans live into their 80s and 90s, the need for vibrant, supportive living environments will explode. Bottom line? Welltower offers us a rare combination:

- A massive, multi-decade demographic trend

- A recession-resilient asset class

- Strong fundamentals and pricing power

- Operational excellence and innovation

- A management team that knows how to allocate capital.

Welltower has consistently invested in high-quality, irreplaceable real estate in demographically advantaged locations – think senior living communities, outpatient medical centers, and memory care facilities in wealthy ZIP codes with aging populations.

Welltower’s capital allocation is conservative, patient, and opportunistic. The company doesn’t overextend during up markets. It keeps dry powder for downturns. And it’s betting on trends that are slow-moving, mathematically inevitable, and largely impervious to political or economic noise.

The company isn’t a speculative play. It’s a long-term compounder tied directly to the biggest population shift in modern history. As more seniors seek vibrant, supportive communities and healthcare shifts toward outpatient and wellness-focused models, Welltower will capture a disproportionate share of this expanding market.

If you’re looking for steady growth, income potential, and exposure to the longevity economy – without the volatility of high-growth tech or the cyclicality of retail – Welltower belongs in your portfolio.

Seeing Clearly

I also like the prospects for Clear Secure (NYSE: YOU). Based in New York City, Clear operates a biometric identity platform that allows fast, friction-free access to airports, arenas, stadiums, and other public buildings.

It is best known for its CLEAR identity platform, which uses fingerprints and facial recognition to allow travelers to bypass long security lines at airports.

Since going public in 2021, Clear has positioned itself as a leader in this field, with a strong growth trajectory and even more exciting expansion potential.

In today’s dangerous world – which includes not just terrorists and fugitives but also, according to U.S. Immigration and Customs Enforcement, nearly half a million illegal immigrants with known criminal records – there is an increasing demand for secure identity verification.

Clear operates its business as a subscription service. This is the best model for customer retention. It’s a reliable way for companies to build steady, recurring revenue. And with the growing adoption of biometric technology for security purposes, Clear has seen a rapid increase in its subscriber base.

The company already has more than 33 million members. Its biometric technology is being used at 59 airports across the United States. (The firm has major partnerships with airlines and the Transportation Security Administration.)

The COVID-19 pandemic also emphasized the need for contact-free verification, pushing sectors like healthcare, hospitality, and finance to adopt its services.

Clear Secure’s biometric technology is highly accurate, user-friendly, and capable of verifying identities within seconds.

So perhaps it’s no surprise that second quarter sales and earnings easily topped estimates. Operating income grew 19% on an 18% increase in revenue, as the company added several million new subscribers during the period.

In an age where data breaches and identity theft are becoming more common, biometric technology offers the most secure and efficient way to protect identities. Clear’s early leadership in this space gives it a first-mover advantage, as well as an opportunity to capture increasing market share in an emerging industry.

Due to increasing demand for security services in travel, finance, and healthcare alone, I estimate that the identity management industry will grow at a 20% annual rate over the next decade.

As these industries digitalize and enhance their security protocols, Clear’s biometric technology will become an integral part of their systems.

In the third quarter, the company reported that earnings jumped 21% on a 6% increase in revenue. The company also repurchased millions of shares in 2025. (That’s a big plus, because when you divide higher profits by fewer shares outstanding, you get even stronger growth in earnings per share.)

The firm is a major innovator. It has already rolled out a new iteration of its service called CLEAR Plus, which makes verifications up to 30% faster.

This is largely due to its new “face first” technology, which allows facial identification even when individuals are moving. (Ultimately, that will mean no more stopping at a CLEAR kiosk to verify an ID.)

Within four years, 1 million more passengers are expected to crowd America’s terminals every day, putting increased strain on a system that is already over capacity.

Aging infrastructure and technology compound these challenges, especially at screening checkpoints.

But Clear is bringing the latest technology and infrastructure to American airports, making security faster and easier.

With over 33 million subscribers and a growing network of partners around the world, Clear already holds a leading position in the biometric security industry. And there is plenty of room for expansion, with the firm’s short-term goal to increase its subscriber base to more than 50 million members.

The stock remains attractive at current levels.

MEET THE EXPERTS

Alexander Green

Chief Investment Strategist

Alexander Green is Chief Investment Strategist of The Oxford Club and Liberty Through Wealth. For 16 years, Alex worked as an investment advisor, research analyst and portfolio manager on Wall Street. After developing his extensive knowledge and achieving financial independence, he retired at the age of 43. Since then, he has been living “the second half of his life.” He is the Senior Editor of The Oxford Communiqué, which was ranked as one of the top investment newsletters by Hulbert Digest for more than a decade. He also operates three fast-paced trading services: The Momentum Alert, The Insider Alert, and Oxford Microcap Trader. Alex is also the author of four New York Times bestselling books: The Gone Fishin’ Portfolio: Get Wise, Get Wealthy… and Get On With Your Life; The Secret of Shelter Island: Money and What Matters; Beyond Wealth: The Road Map to a Rich Life; and An Embarrassment of Riches: Tapping Into the World’s Greatest Legacy of Wealth. His newest book The American Dream: Why It’s Still Alive… and How to Achieve It, is now available on Amazon.