TABLE OF CONTENTS

Paving the Way to Profits

The Infrastructure Stock Built for Long-Term Growth

Alexander Green, Chief Investment Strategist, The Oxford Club

Trading has turned choppy in recent weeks, and it’s not hard to see why.

U.S. jobs growth has come in lighter than expected. The price and economic effects of Trump’s tariffs are hard to predict (and only just beginning to be felt). And valuations on some of the most popular stocks have reached nosebleed levels. So it’s no surprise we’ve seen some big down days in the market recently.

However, you can reduce the volatility in your portfolio – and increase its profitability – by focusing on companies where future growth is practically assured.

For instance, this month I’ll highlight a company where revenue is growing at a 50% rate year over year, profits are skyrocketing, and the outlook is so attractive that institutional investors have snapped up almost 100% of the outstanding shares.

It’s a best-in-class operator with unmatched exposure to public infrastructure in high-growth U.S. markets.

With a record project backlog, accelerating sales and earnings, and a powerful industry tailwind, Construction Partners (Nasdaq: ROAD) is the newest addition to our Oxford Trading Portfolio.

Time to Go on the Defensive

On a Clubroom call a few weeks ago – and in my recent Liberty Through Wealth columns – I’ve made the case that the market is looking a bit frothy and Members should make their portfolios more conservative.

How is the market looking frothy?

- The top 10 companies in the S&P 500 trade for 30 times projected earnings for the next 12 months. That’s roughly twice the historical average. And it’s above the

25 times that the top 10 fetched at the peak of the dot-com bubble. - Investors justify this valuation by arguing “this time it’s different,” another sign of a market top. Twenty-five years ago, they insisted that “the internet changes everything.” Today they insist that “AI changes everything.” Both claims are true. But that doesn’t justify throwing caution to the wind or paying excessive prices.

- Insiders have turned cautious. We can see this in the insider sell/buy ratio published by Vickers Insider Weekly. The ratio turns bearish when insiders are selling six shares for each one that they buy. It recently hit nearly double that at 10.5. (Insiders, of course, can’t time the market any more than you or me. But the absence of buying indicates that they believe most stocks are too expensive to purchase.)

- Individual investors are shoveling money into the market – a contrarian signal. They poured a record $155 billion into stocks and exchange-traded funds in the first half of the year. And cyclical stocks are trading at a record premium versus defensive ones, further accentuating bullish sentiment.

- Money managers are holding little cash. A recent Bank of America fund manager survey found that cash as a percentage of assets under management recently fell to an extreme low of 3.9%. This is a historically bearish signal.

- There has been a surge in high-risk trading activity. Too many investors are chasing tiny companies without even sales, much less earnings. And it’s not just mom and pop. Even institutions are trading meme stocks, meme coins, and all sorts of high-risk crypto (a redundancy if there ever was one).

As you can see, sentiment among both professional and individual investors is overwhelmingly bullish.

Some investors might ask, “What’s the problem with that?” But the more investors and cash that come into the market, the less fuel there is to drive share prices higher still. History shows that extreme bullish sentiment is a negative, just as extreme bearish sentiment is a positive, as I pointed out to Members here three years ago.

This does not mean you should move to cash, however. For one thing, the indicators could be wrong and the market might continue to rise – not just for a while but for a long while.

And even if a downturn does materialize, long-term investors should be prepared to ride out corrections and bear markets. They are as normal as night following day. (But a whole lot less predictable.)

But there are a few things that both traders and investors can do to make their portfolios more conservative – and without moving to cash.

You can make your asset allocation more conservative by reducing your equity exposure and increasing your fixed income exposure. You can tighten your trailing stops to protect more of your principal and your profits. And you can focus new investments on companies that are not sensitive to changes in the economy.

With that last factor in mind, let’s take a closer look at Construction Partners.

A Hard Asset Play With Built-In Demand

Based in Dothan, Alabama, Construction Partners is a civil infrastructure company that operates across several Sunbelt states, including Alabama, Florida, Georgia, North and South Carolina, Tennessee, Oklahoma, and Texas.

It specializes in the construction, repair, and maintenance of critical surface infrastructure. I’m talking about roads, highways, bridges, and airport runways. The firm is also involved in site development, including the installation of utility and drainage systems.

In other words, the company’s work is never-ending and almost entirely paid for by the federal, state, and local government, which makes for high-quality accounts receivable. (However, the company does also take on private projects, such as residential developments and commercial sites.)

And it manages the full value chain through its own mines for gravel and crushed stones, hot-mix asphalt plants, and liquid asphalt terminals.

This vertical integration improves execution, keeps costs down, and increases margins.

Is this business sexy? No. Is it profitable and growing rapidly? You bet.

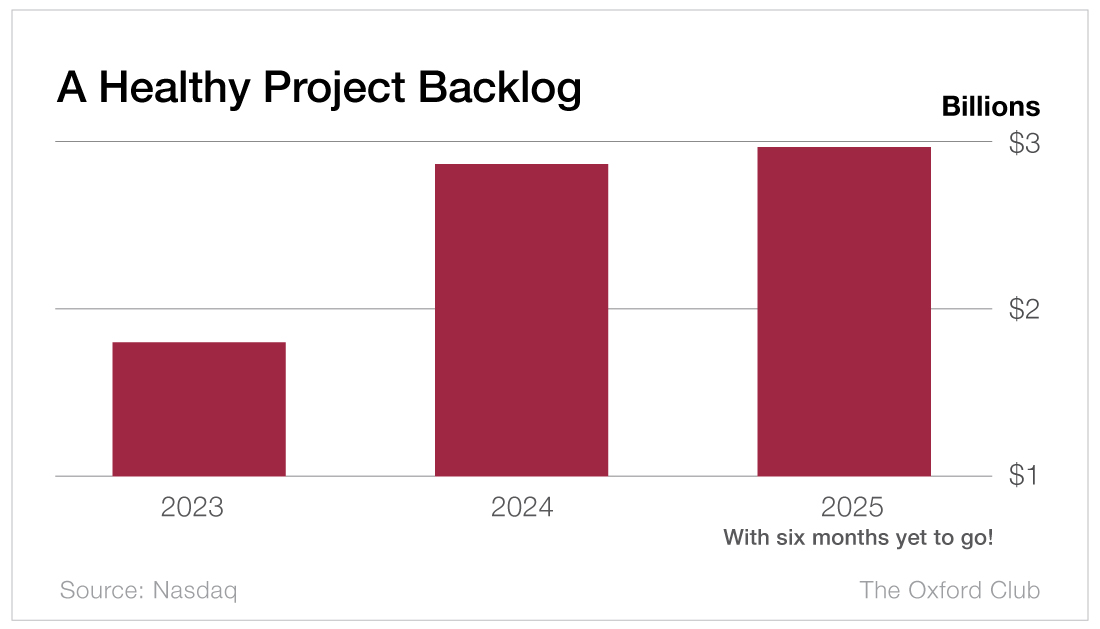

In the most recent quarter, Construction Partners reported that adjusted EBITDA soared 80% on a 51% increase in revenue. Cash flow from operations more than doubled. And its project backlog grew to $2.94 billion.

That’s why the stock has more than tripled the return of the S&P 500 over the past 52 weeks.

And I estimate that earnings per share are likely to jump more than 50% between this year and next, rising from $2.14 in 2025 to $2.35 in 2026.

Why is the outlook so promising?

- The firm has a record project backlog: $2.94 billion, up from $1.79 billion a year ago.

- Increased government investment in infrastructure – especially following the passage of the $1.2 trillion Infrastructure Investment and Jobs Act – is funneling significant capital into transportation and surface projects that are the firm’s core focus.

- The company is expanding through both organic growth and a disciplined acquisition strategy, recently entering new markets and broadening its service offerings.

- Construction Partners’ use of advanced construction technologies and process improvements makes costs more efficient and gives it the ability to take on larger, higher-margin projects.

- The construction industry in the United States is experiencing a period of strong demand driven by economic growth, population expansion in the Sunbelt, and a renewed national focus on infrastructure.

Industry spending exceeded $2 trillion in 2024 with nonresidential activity and public sector projects leading the way.

And trends such as sustainability and a shift toward advanced, eco-friendly materials provide additional structural tailwinds for a well-managed, innovative firm like Construction Partners.

In short, the firm is a market leader in civil infrastructure with a proven track record of growth, an expanding footprint in some of the fastest-growing U.S. regions, and a project pipeline that secures future earnings.

Its vertical integration, strong public-sector demand, and ability to benefit from federal infrastructure initiatives also make the stock an attractive investment. This stock belongs in every Member’s portfolio.

Action to Take: Buy Construction Partners (Nasdaq: ROAD) at market. And use our customary 25% trailing stop to protect your principal and your profits.

Building Wealth

Your Do-Nothing Strategy for Navigating a Frothy Market

Kristin Orman, Research Director, The Oxford Club

The market has been reaching record highs, but not everyone is celebrating…

A good number of stocks are overpriced, and many analysts predict they will have to come down. But the biggest red flag I’m seeing right now comes from a single metric…

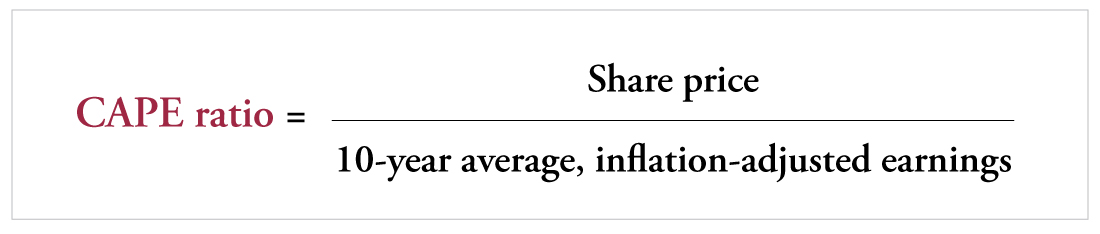

That metric is the cyclically adjusted price-to-earnings ratio (CAPE ratio).

The CAPE ratio measures a stock’s or index’s current price versus the average of its inflation-adjusted earnings over the last 10 years.

This method is used to provide a more stable measure of valuation than the standard price-to-earnings ratio because it smooths out fluctuations in corporate profits.

The CAPE ratio for the S&P 500 right now is 37.8. It’s been this high only two other times – once in 1929 and again in 1999. (Consider – those were right before the Great Depression and the dot-com bust.)

Right now, the market has a lot to be concerned about. Sticky inflation, a weakening job market, and rising tariffs are all significant risks to the economy and stock prices. And with valuations so high, stock prices have a lot of room to fall.

So what should you do differently if you believe the stock market is overvalued? The answer may surprise you…

How to Weather This Market

Investors should do absolutely nothing – at least, nothing new…

The steps you should take to protect your wealth are the same regardless of whether the market is overvalued or undervalued.

Here are the principles that will stand the test

of time…

- Diversify your investments: Spread investments across many different asset classes – stocks, bonds, real estate, etc. By doing this, you’ll reduce the impact of a single asset class on your portfolio. The mix of asset classes will depend on your financial goals, risk tolerance, and time horizon. Adding international stocks to your portfolio is also a great way to diversify your portfolio, as they often outperform U.S. stocks over certain time periods.

- Rebalance regularly: As your portfolio grows, certain asset classes or stocks may outperform and become a larger proportion of your portfolio. Rebalancing involves selling some of the assets that have done well and reinvesting the proceeds in others. Regular rebalancing ensures that you maintain your targeted asset allocation.

- Manage risk: Use stop-loss orders, including trailing stops, to protect profits and limit potential losses on specific investments.

- Maintain a long-term view: Over time, the market goes up. That’s why it’s so important to stick to your investment plan and avoid making impulsive changes in response to market volatility. Keep abreast of market and economic trends and news, but don’t let the short-term noise drown out your long-term goals. Staying the course is the best plan for navigating any market.

And following The Oxford Communiqué’s model portfolios is an easy way to ensure that you stay invested and diversified, all while managing risk in smooth or volatile markets.

Beyond Wealth

The Most Beautiful Place on Earth?

Alexander Green, Chief Investment Strategist, The Oxford Club

Is it possible for a place to be spiritual? Not a church, a shrine, or a tabernacle, but just an area of incredible natural beauty?

I set out to answer that question a few years ago when I drove south on scenic Highway 1 from Monterey, California, with my colleague Steven King. We were on our way to Big Sur, the famous 90-mile stretch of rugged and beautiful coastline between Carmel and San Simeon.

Steven had never been there before. “What are we going to do when we get there?” he asked, a bit apprehensive.

“Just look,” I said.

“You’re kidding, right?”

It was a picture-perfect day: 63 degrees, a gentle breeze blowing in off the coast, not a cloud in sight. Suddenly, to the left us were the imposing Santa Lucia Mountains, and on the right a majestic view of the Pacific.

“Holy –,” Steven said, dumbstruck as we rounded the first bend.

This is arguably the world’s most dramatic meeting of land and sea, an area of unsurpassed natural beauty. For decades, it has attracted painters, sculptors, novelists, and other creative types, including one of my favorite American writers, Henry Miller.

The author of Tropic of Cancer and Stand Still Like the Hummingbird called Big Sur home from 1944 to 1962. And he clearly drew inspiration here.

“Often, when following the trail which meanders over the hills,” he wrote, “I pull myself up in an effort to encompass the glory and the grandeur which envelops the whole horizon. Often, when the clouds pile up in the north and the sea is churned with white caps, I say to myself: ‘This is the California that men dreamed of years ago, this is the Pacific that Balboa looked out on from the Peak of Darien, this is the face of the earth as the Creator intended it to look.”

Steven and I soaked up the vistas for a couple hours, then hiked a few mostly empty trails through the redwoods in Julia Pfeiffer Burns State Park. Afterward, we stopped in for a bit of browsing at the local Henry Miller Library. “Check your neuroses and psychoses at the gate” reads a sign out front.

Yet it’s tough having a genuine Miller memorial. For starters, he didn’t approve of them. Memorials, he said, “defeated the purpose of a man’s life. Only by living your own life to the full can you honor the memory of someone.”

His own days were certainly full of gusto. As a young man, he lived an impecunious life, roaming the streets of Paris. His entire life, in fact, was nonmaterialistic.

“If there is to be any peace,” he once wrote, “it will come through being, not having.”

Miller was married five times. (Another good reason he was broke.) He was a painter, an essayist, a pianist, and a novelist, and was featured in Warren Beatty’s film Reds. He spent years studying the world’s great religious traditions, and he found something to admire in each of them:

Buddha gave us the eight-fold path. Jesus showed us the perfect life. Lao-Tzu rode off on a water buffalo, having condensed his vast and joyous wisdom into a few imperishable words.

Steven and I knocked about the library for a while – squinting at old photographs, letters, and manuscripts – then headed back out to the cliffs to watch the harbor seals and a school of more than a hundred dolphins, the biggest one I’ve ever seen. (We also searched the sky overhead for the elusive California condor. No luck.)

We topped off the day with a leisurely lunch and a glass of sauvignon blanc at Nepenthe – absolutely recommended – before heading back down the coastline.

So, does a lazy day at an idyllic spot really count as a spiritual experience? I doubt Henry Miller would argue the point. When he died in 1980, he had his ashes scattered off the coast here.

“It was here in Big Sur,” he wrote, “I first learned to say Amen!”

Portfolio Review

Holdings With Serious Momentum

Alexander Green, Chief Investment Strategist, The Oxford Club

Historically, the companies that have delivered the best returns for investors have not been the ones that posted the best earnings results.

They’ve been the ones that posted the best results – and topped what analysts expected by a huge margin.

When that happens, the stock generally moves sharply higher. But there are exceptions.

That’s what we saw recently with Teradyne (Nasdaq: TER), a holding in our Oxford Trading Portfolio.

The firm announced first quarter sales and earnings that were far beyond what Wall Street expected.

Yet the stock got no respect and sold off hard anyway. From its May low, however, our shares

have tacked on more than 30 points – and we’re now up 26% from our initial entry price five months ago.

Let’s take a closer look at what’s going on here and why…

Based in North Reading, Massachusetts, Teradyne is a major supplier for semiconductor equipment manufacturers.

Its products bring cutting-edge innovations – such as smart devices, lifesaving medical equipment, and data storage systems – to the market faster.

By automating two of the most critical elements for manufacturers (repetitive manual tasks and electronic tests), Teradyne allows hundreds of manufacturers to deliver the highest-quality products as quickly and economically as possible.

Virtually every electronic device we use has been enhanced by Teradyne during its assembly or testing.

The company is the largest U.S. maker of chip test equipment. And its systems are widely viewed as the gold standard.

The computers, laptops, smartphones, and other electronics you purchase today have a high level of reliability.

That’s because Teradyne’s advanced test solutions for semiconductors, electronic systems, and wireless devices ensure that products perform as they were designed. However, as profitable as Teradyne’s testing business is, the firm’s most exciting division is its robotics business.

Repetitive, mundane, and physically challenging tasks can be tedious and dangerous for workers.

But Teradyne’s collaborative robots (or “cobots”) automate jobs, deliver faster returns on investment, and free workers to focus on jobs that require human input.

The company’s robotic offerings help manufacturers of all sizes improve safety, increase productivity, and cut costs.

Moving cobots to new processes is fast and easy, giving manufacturers the agility to automate almost any manual task, including those with fast changeovers.

Aside from safety and flexibility, using robots to automate quality inspection lets manufacturers maintain consistently high product quality levels.

And cobots help businesses overcome labor and skills shortages and create a better environment for workers.

In sum, Teradyne’s Universal Robots division allows employees to work with robots, not like robots. The company serves a diverse range of industries – from autos to telecommunications to aerospace – mitigating the risk of serving a single industry.

Its heavy investments in research and development allow it to stay at the forefront of technological advancements – and stave off competition.

The firm has consistent revenue growth, healthy profit margins, and solid cash flow generation.

Teradyne ensures that the chips in our computers, smartphones, and other electronics are effective, inexpensive, and reliable. That’s a vital business.

It also makes, sells, and services robots that help American businesses deal with a widespread labor and skills shortage while freeing workers to do less tedious or less dangerous jobs.

For all these reasons, I expect Teradyne to be one of the market’s top performers in the months ahead.

This Glazier Shines

I also like the prospects for Corning Inc. (NYSE: GLW), which I added to our Oxford Trading Portfolio in the May issue of the Communiqué.

Our shares are already up 55% – more than doubling the return of the S&P 500 over the period – and recently hit a 52-week high.

Based in New York, Corning is a global leader in materials science with unparalleled expertise in ceramics and optical physics.

The firm’s innovations include the first glass bulbs for Thomas Edison’s electric light, the first low-loss optical fiber, the first cellular substrates that enabled catalytic converters, and the first damage-resistant cover glass for mobile devices.

Corning is accelerating and transforming entire industries, including consumer electronics, optical communications, and the automotive industry.

And it’s about to revolutionize the construction and remodeling industries as well.

The company is famous for making glass that is thin, insulated, and damage-resistant. It pioneered the invention of low-loss optical fiber in 1970. And it has since become a cornerstone of the telecommunications industry.

The company makes optical fiber and cables, connectivity solutions for hyperscale data centers, 5G networks, and broadband infrastructure.

It manufactures glass substrates for LCDs used in computers, monitors, and TV sets. It makes windshields, display sensors, and connectors for automobile manufacturers. It has also become

a leader in AI infrastructure.

(The firm recently launched GlassWorks AI, which positions Corning as a critical enabler of generative AI technologies, offering high-density optical infrastructure for data centers.)

Corning is also revolutionizing windows. The Energy Department estimates that U.S. households waste $200 to $400 a year on energy bills due to leaks, drafts, and inefficiencies. That totals at least $25 billion a year.

However, Corning has created new three- and four-pane windows that can insulate even better than walls – yet they cost only about 20% more than standard energy-efficient windows.

Installing them will bring huge energy savings to those who retrofit. It will also enable the construction of new homes that are so well-insulated that even when the power goes out in a winter storm, they will stay warm for days.

These windows can meet the most stringent hurricane-related building codes in the country while being significantly lighter than conventional stormproof windows.

How is this possible? Corning makes thin, tough Gorilla Glass that is a key component in today’s mobile devices.

To win over Steve Jobs as a client when he came up with the iPhone, Corning offered Apple a new kind of LCD display made with chemically strengthened glass.

That makes it resistant to scratches and chipping.

Corning’s factories now use the same process to create far larger sheets of similarly tough glass for windows.

These sheets are thinner than a credit card, yet they can be bigger than a queen-size mattress.

Corning is now ready to mass-manufacture these reinforced windows at two facilities, one in Colorado and the other in Pennsylvania. And it’s moving rapidly to capitalize on this new market.

And recent quarterly results were exceptional. Earnings soared 351% on a 19% increase in revenue.

Much of the revenue surge is coming from data centers building out infrastructure for generative AI applications.

How about Trump’s tariffs? Not a problem here.

Almost all the products Corning sells in the U.S. originate in its 34 advanced manufacturing facilities in the U.S.

And nearly 90% of its domestic revenue comes from products of U.S. origin.

In short, Corning’s strategy is right for the times.

It’s capitalizing on two of the most investable secular trends – AI and renewable energy – while expanding margins and securing multiyear revenue streams.

If you’re looking for solid earnings momentum, growing end-market demand, and clear strategic leadership, Corning belongs in your portfolio.

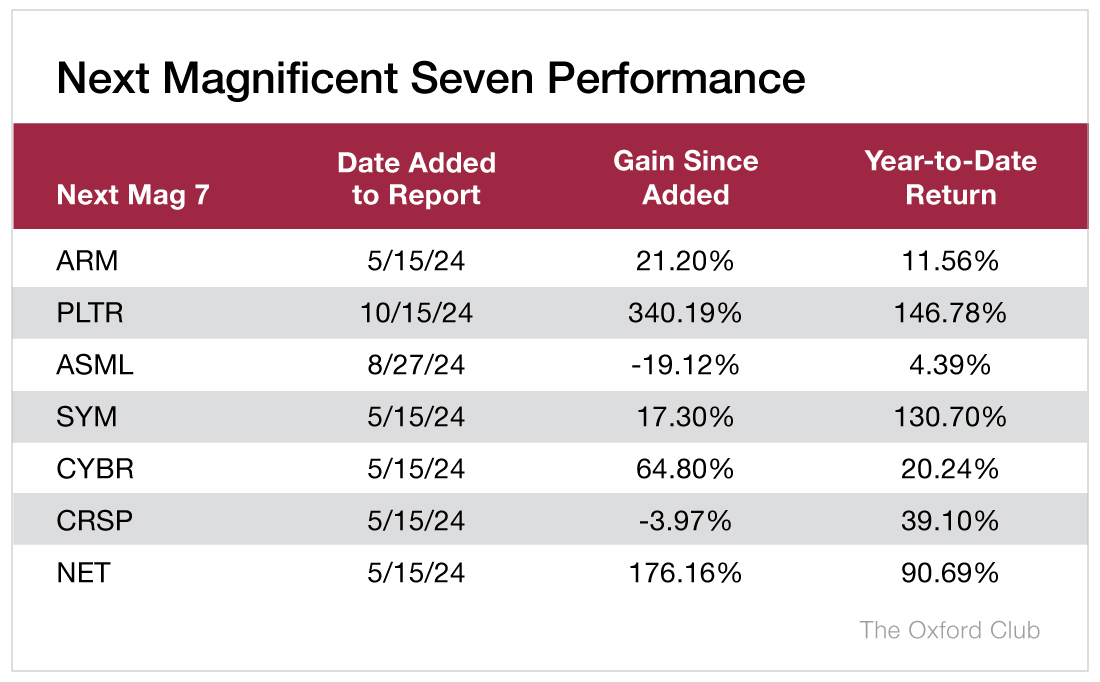

An Update on the Next Mag 7

A big focus this year has been on seven specific stocks I’ve dubbed “The Next Magnificent Seven.”

For those who are unfamiliar, they are…

- Arm Holdings (Nasdaq: ARM)

- Cloudflare (NYSE: NET)

- ASML Holding NV (Nasdaq: ASML)

- Palantir (NYSE: PLTR)

- Symbotic (Nasdaq: SYM)

- CyberArk Software (Nasdaq: CYBR)

- Crispr Therapeutics (Nasdaq: CRSP).

The Next Magnificent Seven have strongly outperformed the markets this year, especially after the April downturn.

Since the publishing of the Next Magnificent Seven report, Cloudflare is up 176%. And Palantir – which replaced Exscientia – is up a staggering 340%.

The year-to-date returns for all the Next Magnificent Seven are positive, with Symbotic up more than 130%. And not to mention, more room to run.

MEET THE EXPERTS

Alexander Green

Chief Investment Strategist

Alexander Green is an analyst, author and speaker whose primary mission is to show investors how to achieve and maintain financial independence. For 16 years, he worked as an investment advisor, research analyst and portfolio manager on Wall Street. He has been the Chief Investment Strategist of The Oxford Club since 2001.

He is the New York Times bestselling author of The Gone Fishin’ Portfolio (now in its second edition), Beyond Wealth, The Secret of Shelter Island and An Embarrassment of Riches.

In addition to directing The Oxford Communiqué, he oversees three fast-paced trading services: The Momentum Alert, The Insider Alert, and Oxford Microcap Trader.

Kristin Orman

Research Director

Kristin has worked as a Research Analyst and contributor to Wealthy Retirement since 2014. She provides deep, fundamental and inferential insight to the Club’s strategists.

Prior to joining The Oxford Club, she spent 10 years as a trader, analyst and portfolio manager. A self-proclaimed “recovering short seller,” Kristin began her career with a highly respected independent research firm, where she learned the value of contrarian investing.

The Club’s secret to success, according to Kristin, is its ability to marry Wall Street financial analysis with Main Street common sense.

She holds a B.A. in political science and psychology from The Ohio State University.