TABLE OF CONTENTS

Built to Last…

The Rugged Brand With 150% Upside Potential

Alexander Green, Chief Investment Strategist, The Oxford Club

Peter Lynch is the greatest equity fund manager of all time. He ran the Fidelity Magellan Fund from 1977 to 1990. During that time, the fund earned an annualized return of 29.2%.

He also increased the fund’s assets under management from $20 million to $14 billion during his tenure.

As a young man just starting out in the money management industry, I devoured Lynch’s two investment classics: Beating the Street and One Up on Wall Street.

In those books, Lynch recommended one investment strategy that was devastatingly simple in its common-sense approach.

He contended that if you really love a company’s products or services, other customers probably do too. That bodes well for the business… and the share price.

Today I’ll share a story about a company I patronize regularly – and that we traded successfully a couple years ago.

It’s a leader in its category. But that’s mostly because it invented the category – high-end outdoor gear.

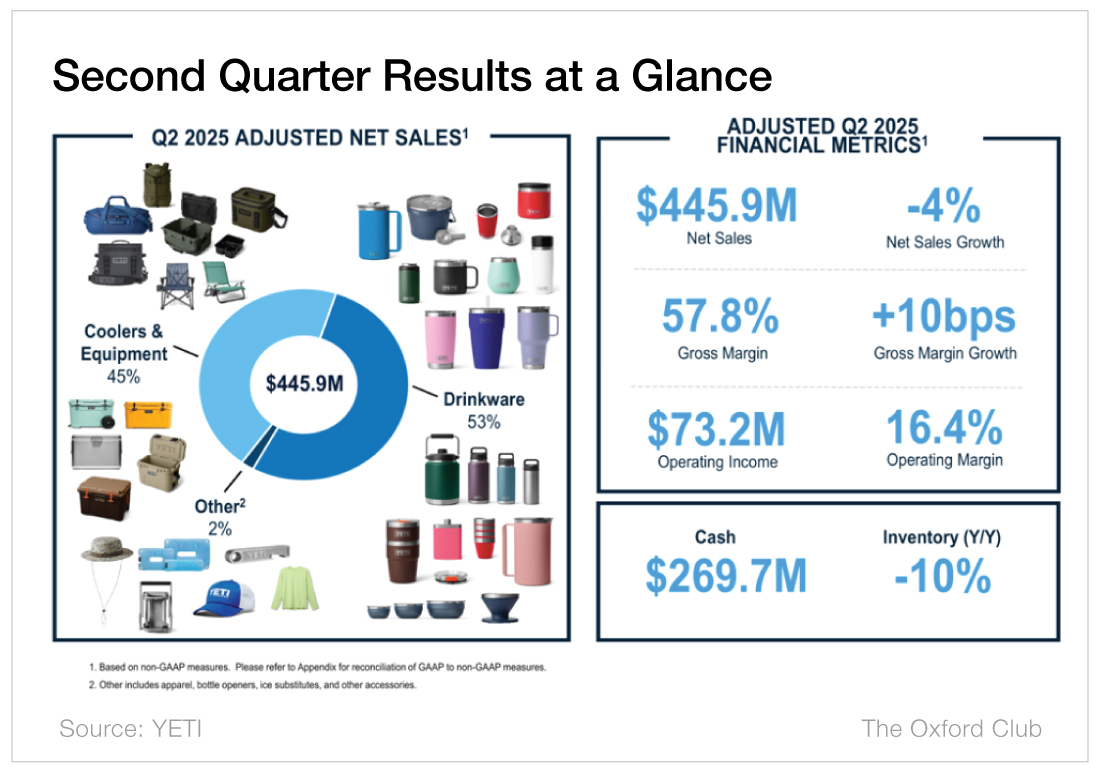

It’s a young company that is still early in its growth. Yet it has more cash ($270 million) than debt ($76 million).

Over the last few years, sales have risen to $1.6 billion. It enjoys a 12% operating margin. Management is earning a healthy 20% return on equity.

And for reasons I’m about to reveal, the share price has 150% upside potential from here.

For all these reasons, Yeti Holdings (NYSE: YETI) is back in our Oxford Trading Portfolio.

The Power of Recognition

Before I get into the specifics of this stock, let me discuss something that is critical to the success of virtually all companies: brand names.

A strong brand name is one of the most valuable assets a company owns. It’s not just a label. It conveys meaning, quality and trust. It shapes consumer perceptions. It differentiates products in crowded markets. And it builds long-term customer loyalty.

Not least of all because consumers use brand names as shortcuts in decision-making, especially when they face many options.

Markets for consumer goods are intensely competitive, with countless products offering similar functions. In this environment, brand names become a critical differentiator.

A well-known brand signals consistency and reliability, which reduces uncertainty and risk for buyers – and the retailers who carry their products.

That’s why people ask for a Coke rather than a cola, a Kleenex rather than a tissue, and a pair of Nikes rather than just new sneakers.

Yeti has also developed strong brand recognition. And it is now leveraging it in several new product categories. That is likely to drive sales and earnings – and, ultimately, the share price – sharply higher.

Quality Over Everything

Based in Austin, Texas, Yeti designs, markets, and sells outdoor and recreational products.

These include hard and soft coolers, bags, and drinkware – including coffee mugs, wine tumblers and water bottles – as well as Yeti-branded gear, such as backpacks, hats, shirts, bottle openers and ice substitutes.

Its products are sold through independent retailers, hardware stores, specialty stores, direct-to-consumer outlets and the company’s website.

You’ll find them everywhere from Bass Pro Shops to Dick’s Sporting Goods to Amazon.

No single retailer exceeds 10% of Yeti’s overall sales. (That diversification protects the company from a problem at any individual retailer.)

The company was founded in 2006 by two brothers: Roy and Ryan Seiders.

They have a passion for the outdoors – especially hunting and fishing – and were disappointed in the quality of most coolers.

The handles would break. The latches would snap off. The lids would cave in. And their drinks wouldn’t stay cold all day.

They solved that problem by building coolers designed for serious outdoor enthusiasts.

Those who own Yeti products already know what I’m talking about.

You can fill a Yeti cooler with ice, have a party on Friday afternoon, and when you open that cooler on Sunday, it’s not full of water. It’s still full of ice!

As the company notes on its website, its coolers represent “The Cold Standard.”

The same is true for the company’s tumblers. Take one full of lemonade to the park or the tennis courts in the noonday sun, and your drink won’t just stay cold – the ice will last for several hours.

It’s like the company has found a way to nullify the laws of thermodynamics.

These days I don’t take a trip – any trip – without throwing a Yeti mug into my suitcase. The world just isn’t civilized without it. (Or, at least, the coffee isn’t nearly as hot.)

As you can see, I’m a big fan of the company’s products. And I’ve learned something else: So are a lot of other people. The company’s reputation for quality is widely recognized.

The firm has done an outstanding job of turning customers into raving fans. Yet most people don’t buy Yeti products. Why?

Because they are admittedly expensive. Most folks will not pay $275 for a cooler or $38 for a stainless-steel tumbler.

Yeti’s products are high-end and made for discriminating, affluent buyers. Like Whole Foods, Mercedes-Benz, and Armani, Yeti offers premium products to an upscale customer base.

Yet as angler – and Yeti Fishing Ambassador – Flip Pallot points out, “Yeti represents the yardstick by which all other outdoor products are measured.”

(The company’s Tundra hard cooler is even certified as grizzly-bear proof by the Interagency Grizzly Bear Committee.)

Yeti has taken a rarefied category – hiking and camping gear – and turned it into a multibillion-dollar opportunity at the intersection of recreation, consumer goods, and lifestyle branding.

I expect total sales to hit $1.85 billion this year and rise to more than $2 billion next year. Earnings per share should rise 33%, from $2.40 in 2025 to $3.20 in 2026.

Why do I see a big jump coming in sales and earnings?

- This is a young and growing company that is benefiting from word-of-mouth advertising.

- The firm is opening more direct-to-consumer outlets. It already has more than 20 stores across the U.S.

- Its direct-to-consumer business – about half of sales – supports higher margins and is growing more than three times as fast as the firm’s other revenue.

- It is expanding rapidly in international markets where revenue growth is particularly robust.

- Yeti has transformed its supply chain. Less than 5% of products will be exposed to U.S. tariffs by year end.

- Over 30 new products are slated for launch this year. The company is already having notable success with bags and packs.

- The firm has also diversified into more product lines, including chairs and camping gear.

- It specializes in customization, new colors, and limited-edition offerings to encourage new and repeat purchases.

- And the brand has pricing power.

Unlike low-end competitors, Yeti competes on quality, not price. Its products routinely command double or triple the price of generic alternatives.

That’s because it’s not just another consumer products company. By leaning into themes of durability, authenticity and rugged simplicity, it has established itself as a premium lifestyle

brand with strong customer loyalty.

That’s why its products are likely to be found not just among hikers, campers, and anglers, but also in the gym, at college tailgates, or strapped on the back of a pickup.

Despite Yeti’s relentless focus on quality and strong customer loyalty, its shares trade at about a third of what they did a few years ago.

While the average company in the S&P 500 sells for 30 times prospective earnings for the next 12 months, Yeti sells at less than 14 times my earnings estimate for the year ahead. That’s a bargain.

I believe that Yeti will hit $90 by the end of 2026. That would be a 150% gain from here.

Yes, there are risks associated with a company that sells premium products to affluent customers. But these consumers are far less economically sensitive than most.

And, as Peter Lynch might point out, the potential rewards make this an attractive investment.

Action to Take: Buy Yeti Holdings (NYSE: YETI) at market. And use our customary 25% trailing stop to protect your principal and your profits.

Building Wealth

Why “Boring” Value Stocks Could Be Your Smartest Move

Kristin Orman, Research Director, The Oxford Club

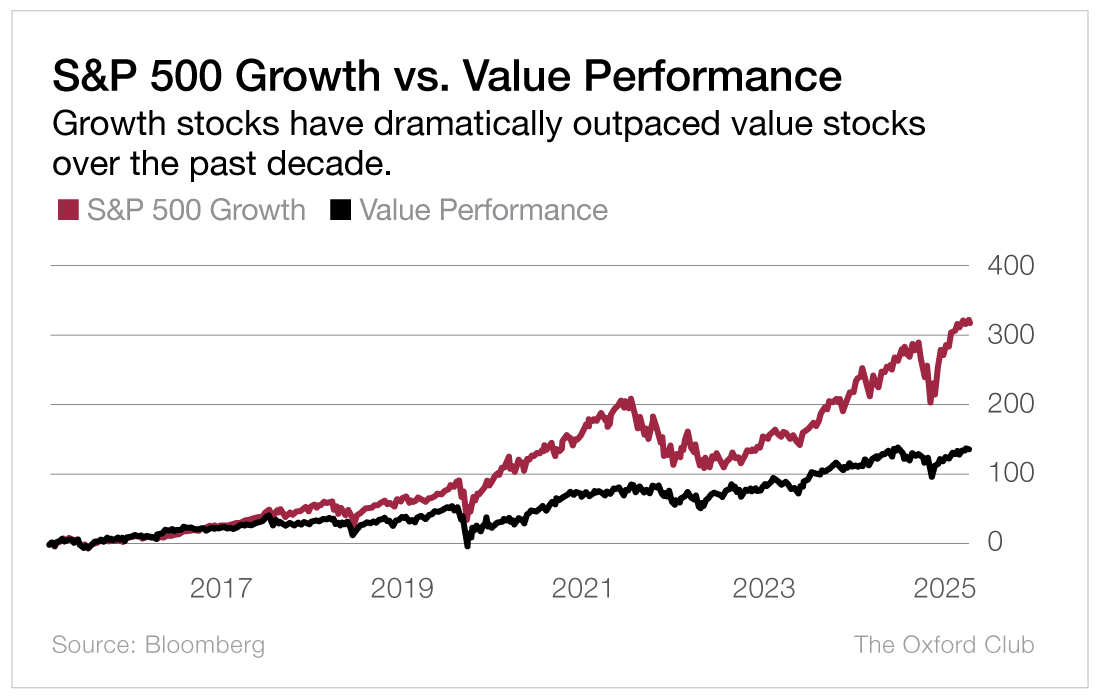

For more than a decade, growth stocks have dominated the market.

Tech giants, cloud innovators, and AI leaders have delivered headline-grabbing returns.

Meanwhile, value stocks – those slow-and-steady companies trading at lower valuations – have lagged far behind. That’s left many investors wondering if value investing is still a viable strategy. The thing is, legendary Vanguard founder John Bogle often reminded investors about one unshakable principle: reversion to the mean.

“A period of above-average performance is inevitably followed by a period of below-average performance. It’s a rule as dependable as gravity.”

Indeed, when an asset class outperforms for too long, it almost always swings back the other way. That’s not just theory – history shows it happens again and again.

What Goes Up…

Over the last decade, the return of the S&P 500 Growth Index has more than doubled that of the S&P 500 Value Index.

Investors have piled into fast-growing companies and largely ignored traditional businesses – even when valuations reached extreme levels.

But here’s the catch… Valuation spreads between growth and value are now at historic highs. The last time we saw a gap this wide was during the dot-com bubble. Back then, investors abandoned value in favor of anything with a “.com” in its name.

The result? A brutal collapse in growth stocks and one of the strongest multi-year runs for value in history.

The Case for Value

Looking back over 50, 70, even 100 years, value has consistently outperformed growth. Why? Because value investing forces discipline.

You’re buying solid companies that are overlooked or out of favor.

You’re paying less for every dollar of earnings.

And you’re positioning yourself for long-term gains when the market eventually “catches on.”

It’s not flashy. It’s not exciting. But it makes money.

So while growth stocks are still having their moment, history – and Bogle’s “Iron Law” – suggests value’s turn is coming.

For long-term investors, now is a great time to…

Review your portfolio for overexposure to expensive growth names.

Consider gradually shifting into undervalued companies.

Stay patient. The payoff for value often takes time, but when the tide turns, it can be dramatic.

That’s easy to say but harder to do – especially when the market keeps rewarding investors who chase what’s already worked. But the most successful long-term investors understand that discipline, not excitement, drives wealth.

Patience may feel boring. But boring is exactly what works.

As John Bogle famously said, “Time is your friend; impulse is your enemy.” In today’s market, that wisdom couldn’t be more valuable.

Beyond Wealth

How to Avoid “The Mañana Syndrome”

Alexander Green, Chief Investment Strategist, The Oxford Club

Eighteen years ago, one of the nation’s largest publishers, John Wiley & Sons, asked if I would write a book about The Oxford Club’s investment philosophy. I agreed, and they paid me a sizable advance to get started.

Unfortunately, I didn’t make the first deadline. Or the second. As the third one loomed, executive editor Debra Englander was on the phone. And she wasn’t happy.

Was I going to write the book or not? I said I was. But when? I was already buried in other research and writing projects.

I tried knocking out my short-term deadlines first, so I could turn my attention to the book later in the week. But things kept piling up and “later” never seemed to happen.

It wasn’t that I didn’t have plenty of material for the book. I did. What’s more, I really wanted to do it. I just felt too exhausted at the end of each day to tackle such a big project.

As I traveled with a group of investors through Italy that year, I finally conceded that trying to write a book on top of all my other commitments was just crazy. Reluctantly, I decided I would return the advance to Wiley and maybe try again when things weren’t so hectic.

With me on the trip, however, was an aspiring writer from Tennessee, Richard Nelson, who had recently published a book of maxims. As we boarded the coach for the airport the next day, he handed me a copy.

On the first page, my eye fell on the following quote: There is no shortage of time, only a confusion of priorities.

I felt like I had been struck on the head with a ball-peen hammer. If I really wanted to do that book, I had to stop wishing I had the time and start making it.

In short, I went to war. I cut out all nonessential activities. I delegated some responsibilities to my colleagues. And no matter what was on my schedule each day, it had to wait until I had spent at least a couple hours working on the book.

With all the excuses out of the way and a genuine commitment underway, I finished it in just over five months. The book The Gone Fishin’ Portfolio: Get Wise, Get Wealthy… and Get on With Your Life became an immediate New York Times bestseller.

And I wrote a revised edition a few years ago, with a new foreword by longtime Chairman’s Circle Member Bill O’Reilly.

But I couldn’t have written that first volume if I hadn’t stopped deluding myself that I would get around to it “eventually.”

At some point, we all have to recognize that we’ll never change our lives for the better – or accomplish the things we really want – until we change something we do daily. This applies to virtually every aspect of life.

Want to rise in your business? Start working harder and learning more about your organization today. Need to put together an estate plan for your family? Call your attorney right now. Want to lose 10 pounds? Start eating better and exercising today. Not tomorrow. Not when you get “one thing” out of the way. Today.

As Gary Buffone writes in The Myth of Tomorrow…

The very fact that our time is finite makes living precious. When we exclude the recognition of our end, when we lose sight of the real stakes involved, life becomes impoverished. It becomes easier to develop “mañana syndrome” and constantly postpone authentic living. People who presume that there is always tomorrow waste away in unproductive and meaningless jobs, joyless relationships, pointless worries, and vague plans for some distant future.

Don’t be one of them. If you need encouragement, John Maxwell, author of Today Matters, offers a helpful prayer:

Dear Lord, so far today, I am doing alright. I have not gossiped, lost my temper, been greedy, grumpy, nasty, selfish, or self-indulgent. I have not whined, cursed, or eaten any chocolate. However, I am going to get out of bed in a few minutes, and I will need a lot more help after that. Amen.

According to Maxwell, “People create success in their lives by focusing on today. It may sound trite, but today is the only time you have. It’s too late for yesterday. And you can’t depend on tomorrow. That’s why today matters.”

Most of us are planners, of course, and forward-looking by nature. But it’s what you do today that determines what you are tomorrow. As the great industrialist Henry Ford once said, “You can’t build a reputation on what you’re going to do.”

So give yourself a friendly push and start pursuing what matters most. Commit to it daily. After all, “there is no shortage of time, only a confusion of priorities.”

Portfolio Review

Two Great Buys in an Elevated Market

Alexander Green, Chief Investment Strategist, The Oxford Club

There are two ways to look at the current market.

On the one hand, second quarter GDP growth was recently revised upward. Corporate earnings have been better than expected.

And the Federal Reserve is likely to keep cutting interest rates between now and the end of the year. That’s bullish.

On the other hand, the job market is softening, tariff uncertainty is growing, and stock valuations – whether you’re looking at price-to-sales or price-to-earnings – are looking a bit frothy. That’s less bullish.

As I mentioned in last month’s issue, Members might want to make their asset allocation more conservative and run their stops a little tighter to protect more

of their principal and their profits.

But there are plenty of attractive opportunities out there still. Today we’ll focus on a conservative one – Labcorp (NYSE: LH) – and a more speculative one, Glaukos (NYSE: GKOS).

A Pulse Check on Labcorp

Based in Burlington, North Carolina, Labcorp offers laboratory services that provide vital information to help doctors, hospitals, drug companies, researchers, and patients make important – and often lifesaving – decisions regarding their health.

The company is a leader in the diagnostics and drug development industry, with a broad portfolio that covers routine testing, advanced genomic testing, and clinical trial management.

Its tests include blood chemistry analyses, urinalyses, blood cell counts, thyroid tests, PAP tests, prostate-specific antigen tests, tests for STDs, and hepatitis C tests, to name just a few.

Labcorp also provides specialty testing that targets specific diseases – offering services related to oncology, cardiovascular disease, endocrinology, and many other areas.

The healthcare industry – and particularly the diagnostics and drug development sectors – is recession-resistant. (Patients don’t put off medical tests because the economy is soft.)

Labcorp isn’t flashy. But it’s quietly building one of the strongest growth stories in healthcare today.

The company has two things going for it that most of its peers don’t: consistent execution and a powerful tailwind from long-term trends in diagnostics and biotech.

The major trends driving its expansion include…

- The “silver tsunami”: An aging population increases the demand for diagnostic testing and personalized medicine. As people grow older, they require more medical testing and treatments, driving growth in Labcorp’s services.

- Rise of chronic diseases: The prevalence of chronic diseases, such as diabetes, cancer, and cardiovascular diseases, is on the rise. Early detection and ongoing monitoring are critical, fueling the demand for Labcorp’s diagnostic services.

- Technological advancements: Innovations in genomics and molecular diagnostics are transforming healthcare. Labcorp’s investment in cutting-edge technology positions it to capitalize on these developments, offering advanced testing solutions that are increasingly in demand.

- Pharmaceutical industry growth: The pharmaceutical and biotechnology industries are experiencing rapid growth, driven by the development of new therapies and the expansion of clinical trials. Labcorp’s comprehensive drug development services make it a preferred partner for these industries.

Over the past few years, the company has demonstrated consistent revenue growth and strong profitability.

Sales over the last 12 months topped $13.4 billion, reflecting the successful integration of acquisitions and the expansion of its offerings.

Earnings per share should rise from $16.35 this year to more than $18 next year.

In short, Labcorp is a low-risk, high-reward opportunity. Biotech companies, hospitals, doctors, patients, and insurance companies all depend on it.

And the company’s commitment to innovation and operational excellence ensures that it remains at the forefront of the industry.

Labcorp’s robust pipeline of new tests and services, combined with its strategic acquisitions and partnerships, positions it for exceptional profit growth in the months and years ahead. No matter what happens with inflation or the economy.

Wall Street has noticed. Price targets have climbed, with a few analysts tagging Labcorp at $370 per share.

In short, this is a business growing its top line, bottom line, and cash flows – and doing it in one of the most recession-resistant industries on the planet.

The macro story is compelling: Aging demographics, rising rates of chronic illness, more personalized medicine, and an increased focus on early detection all fuel demand for what Labcorp provides.

This is a high-quality business trading at a reasonable valuation in a sector with plenty of room to run.

All Eyes on Glaukos

The Ten-Baggers of Tomorrow Portfolio is the most speculative one in our Oxford Communiqué.

The term “ten-baggers” was originally coined by Peter Lynch to describe a stock that rises tenfold.

(Remember, Lynch is the former world-beating manager of the Fidelity Magellan Fund.)

Of course, no stock goes up tenfold overnight. It takes time. Before a stock can rise that much, it must double… and then triple… and so on.

Glaukos – one recommendation in the portfolio – has nearly tripled. Yet, in my view, the best is still ahead…

Based in San Clemente, California, Glaukos is a medical technology company focused on novel therapies for the treatment of glaucoma, corneal disorders, and retinal diseases.

In other words, it’s addressing three of the largest and fastest-growing segments in ophthalmology.

Glaucoma – which can develop in one or both eyes – is actually a group of diseases that damage the eye’s optic nerve, causing vision loss or blindness.

The diseases create pressure inside the eye. And their creeping, symptomless nature means eyesight is often slowly but irreparably stolen.

Without treatment, people with glaucoma first lose their peripheral vision.

Over time, central (straight-ahead) vision also decreases. In the worst cases, those afflicted lose their eyesight altogether.

There is no cure for glaucoma.

However, the disease can be detected through a visual field test and a dilated eye exam. And, with the proper steps, further vision loss can be avoided.

Patients generally begin treatment with eye drops. But many eventually opt for cataract surgery.

That’s where Glaukos comes in.

The company essentially redefined how doctors treat glaucoma when it pioneered Micro-Invasive Glaucoma Surgery (MIGS) – a safer, less invasive approach that’s now become the new standard.

Its groundbreaking product was the iStent, a tiny L-shaped titanium implant that has helped thousands of people with glaucoma successfully manage intraocular pressure.

The company also expanded into corneal and retinal disorders, including dropless sustained-release therapies that aim to improve outcomes and reduce the burden on patients.

Eye diseases are on the rise. Aging populations, diabetes, and increasing life expectancy are all driving demand.

The ophthalmic devices market is projected to grow from $19.3 billion last year to over $30 billion by 2030 – a 7.7% compounded annual growth rate.

The global glaucoma treatment market stands at $6.6 billion, heading toward $10.5 billion by 2034.

Sales are growing at a 30% annual rate. And I estimate that the company will flip from a loss of $0.85 a share this year to a profit of $0.60 a share in 2026.

This year’s loss isn’t a red flag – it’s an R&D story.

Like many innovation-first companies, Glaukos is reinvesting aggressively in its pipeline. That’s how future breakthroughs are born.

The pipeline is where Glaukos truly separates itself:

- iStent infinite: Already FDA cleared, this next-gen MIGS device is designed for open-angle glaucoma that’s no longer responsive to meds.

- Dropless therapy platforms: These target chronic diseases with long-acting, sustained-release implants. That improves both compliance and patient outcomes.

- Retinal implants: Under development for up to six months of drug delivery, they could change how we manage blinding diseases like age-related macular degeneration (AMD) and diabetic macular edema (DME).

Both AMD and DME are chronic, progressive, and require ongoing treatment, often in the form of injections every four to eight weeks.

Companies like Glaukos are developing sustained-release implants to reduce the frequency of those injections – potentially improving patient adherence and quality of life.

This isn’t a bet on a trend. Glaukos is a focused, high-quality business solving urgent problems in a field that desperately needs better answers.

As more patients seek less invasive, higher-efficacy treatments – and as doctors increasingly shift away from older solutions – Glaukos and its shareholders will be huge beneficiaries.

MEET THE EXPERTS

Alexander Green

Chief Investment Strategist

Alexander Green is Chief Investment Strategist of The Oxford Club and Liberty Through Wealth. For 16 years, Alex worked as an investment advisor, research analyst and portfolio manager on Wall Street. After developing his extensive knowledge and achieving financial independence, he retired at the age of 43. Since then, he has been living “the second half of his life.”

He is the Senior Editor of The Oxford Communiqué, which was ranked as one of the top investment newsletters by Hulbert Digest for more than a decade. He also operates three fast-paced trading services: The Momentum Alert, The Insider Alert, and Oxford Microcap Trader.

Alex is also the author of four New York Times bestselling books: The Gone Fishin’ Portfolio: Get Wise, Get Wealthy… and Get On With Your Life; The Secret of Shelter Island: Money and What Matters; Beyond Wealth: The Road Map to a Rich Life; and An Embarrassment of Riches: Tapping Into the World’s Greatest Legacy of Wealth. His newest book The American Dream: Why It’s Still Alive… and How to Achieve It is now available on Amazon.

Kristin Orman

Research Director

Kristin has worked as a Research Analyst and contributor to Wealthy Retirement since 2014. She provides deep, fundamental and inferential insight to the Club’s strategists.

Prior to joining The Oxford Club, she spent 10 years as a trader, analyst and portfolio manager. A self-proclaimed “recovering short seller,” Kristin began her career with a highly respected independent research firm, where she learned the value of contrarian investing.

The Club’s secret to success, according to Kristin, is its ability to marry Wall Street financial analysis with Main Street common sense.

She holds a B.A. in political science and psychology from The Ohio State University.