TABLE OF CONTENTS

A Safe 6% Yielder for a Volatile Market

By Marc Lichtenfeld • Chief Income Strategist

There’s real fear of a recession in the U.S. right now. President Trump’s latest tariff announcement, government layoffs, persistent inflation, and falling Treasury yields are all giving investors, economists, and the average American something to worry about.

In a tough economy and a scary market, it’s easy to bury your head in the sand and wait for better times. But the real money is made when markets are going down. Well-diversified investors who don’t panic and who buy the right stocks during market slides can significantly grow their wealth.

I don’t pretend that’s easy to do. It goes against every emotion we have and our desire to protect what’s ours. But more than a century of market data − and three decades of personal experience − has taught me this is the time to find great stocks to generate great returns.

That being said, we’re also going to be smart. While this month’s recommendation may not be recession-proof (because nothing truly is), its long-term contracts should shield it from any major volatility. Whether the economy continues to cool or heats back up again, this company will still be delivering all of the goods and services that individuals, companies, and governments rely on.

A Gigantic Player in a Gigantic Market

It is estimated that the world will spend $100 trillion – that’s “trillion,” with a T – on infrastructure over the next 15 years, or nearly $7 trillion per year.

Brookfield Infrastructure Partners (NYSE: BIP) is one of the world’s largest owners of infrastructure assets, including pipelines, shipping containers, railroads, and data centers. It operates across five continents in many different businesses that are vital to nearly everyone on Earth.

Its assets include...

- 2,900 km of operational transmission lines in Brazil

- 3,900 km of natural gas pipelines in North America, Brazil, and India

- 8.4 million electricity and natural gas connections in the U.S., Canada, Germany, and the U.K.

- 7 million shipping containers worldwide

- Shipping terminals in the U.S., Australia, and the U.K.

- 21,000 km of railroad track in North America and Europe, 9,800 km in Brazil, and 5,500 km in western Australia

- 3,200 km of toll roads in Brazil

- 360,000 residential telecom connections in the U.S. and Australia

- Two semiconductor manufacturing foundries in the U.S.

- More than 140 data centers.

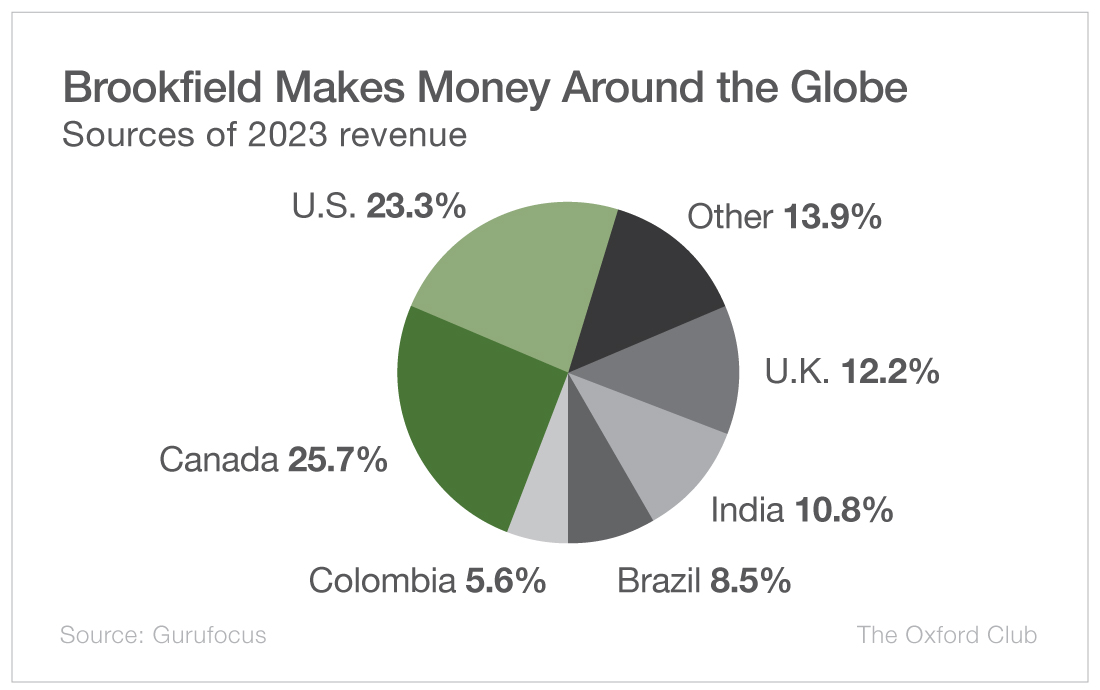

Brookfield is based in Bermuda, but it generates revenue from a number of diverse geographies. As of the end of 2023 (2024 numbers are not yet available), just under half of its revenue came from North America, with almost 26% coming from Canada and 23% coming from the U.S. The U.K. was responsible for 12%, followed by India at 11%.

View larger image

View larger image

Brookfield’s data center business is particularly interesting. You’re no doubt aware of the enormous demand for data centers that’s been sparked by the adoption and continuous improvement of artificial intelligence.

CEO Sam Pollock recently stated that the company’s data segment, which includes data centers, telecom towers, and fiber networks, could become the largest part of the business within five years. In fact, the company is plowing nearly half of its investment dollars into data and digitalization businesses.

While a potential economic slowdown may have some impact on Brookfield’s performance, the company should be relatively resilient, as the services it provides are necessary for both business and everyday life.

Plus, 90% of its funds from operations (FFO) are backed by long-term contracts, many of which are set up to generate more revenue as inflation increases. It also has $8 billion in backlogged orders.

In short, you can feel confident the company will continue to grow its cash flow and its distribution. (Because Brookfield is a partnership, the dividend is called a distribution.)

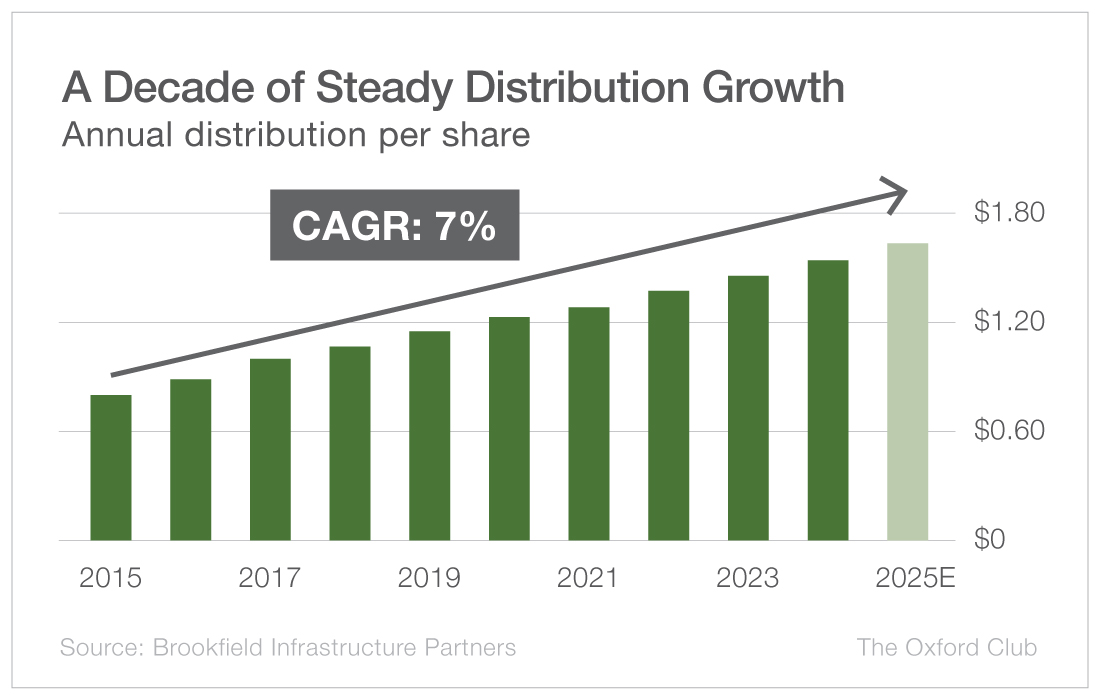

Speaking of the distribution, Brookfield has an impressive track record of rewarding investors. It currently pays a quarterly distribution of $0.43 per share, which equals a 6% yield.

The company has raised its distribution for 16 straight years and is likely to continue doing so for the foreseeable future. Over the past decade, the distribution has climbed at a compound annual growth rate of 7%.

View larger image

View larger image

Brookfield’s FFO, which is the measure of cash flow that we use for master limited partnerships, grew 8% in 2024. This year, it is forecast to rise 9.3%.

In 2024, the company generated $2.5 billion in FFO while paying investors $1.6 billion, for a payout ratio of 67%. Brookfield has a stated payout ratio goal of 60% to 70%, so I’m not worried about it being able to afford its distribution – especially considering that FFO is growing.

View larger image

View larger image

Brookfield Infrastructure Partners is a great way to invest in the projects that keep the world going.

It has predictable cash flow, contracts that should ward off recessionary and inflationary pressures, and an excellent history of raising its distribution every year.

Action to Take: Buy Brookfield Infrastructure Partners (NYSE: BIP) for $31.50 or lower, and add it to the Instant Income and Compound Income portfolios. Place a 25% trailing stop below your entry price in the Instant Income Portfolio only. If the stock is above $31.50, wait for it to come back down.

Though Brookfield Infrastructure Partners is set up as a partnership and you will receive a K-1 statement, only a very small portion of the distribution is a return of capital. As a result, I recommend holding the stock in a tax-deferred account.

FIXED INCOME

Why Municipal Bonds Could Be in Danger

By Marc Lichtenfeld • Chief Income Strategist

The market is buzzing about a possible change for municipal bonds under the Trump administration − and for good reason. The decision could impact fixed income investors in a big way.

The hot topic? The potential loss of municipal bonds’ coveted tax-exempt status. This possibility first surfaced in a recent House Budget Committee document that listed ways the government could raise funds to offset the extension of the 2017 Trump tax cuts. “Eliminate Exclusion of Interest on State and Local Bonds” is right there in black and white.

Now, that doesn’t mean it’s going to happen. But the mere possibility has been enough to rattle the $4.2 trillion muni bond market, and it’s not hard to understand why: The tax advantages are practically the whole appeal of municipal bonds.

The interest on these bonds is typically tax-free at the federal level, and if you live in the state that issued the bond, you often escape state taxes too. Take a 5% municipal bond yield, for example. If you’re in the 32% tax bracket, making 5% tax-free is equivalent to earning 7.35% on a fully taxable bond. That’s a significant advantage, and it has long made munis a go-to investment for income-seeking investors, especially those in higher tax brackets.

The safety of munis remains impressive as well. Between 1970 and 2021, the 10-year cumulative default rate for investment-grade municipal bonds was a tiny 0.1%. That’s a mere 1-in-1,000 chance of default. In fact, muni bonds have an average credit rating of AA – the same as the U.S. federal government.

The House Budget Committee estimates that eliminating the tax exemption could add about $250 billion to federal coffers over 10 years. But the Public Finance Network found that it could also raise borrowing costs for cities and states by $824 billion. Those costs would ultimately get passed on to households, amounting to a projected $6,555 tax increase per household over the next decade.

As for the specific impact on muni investors, there are a few scenarios that could unfold.

If the tax exemption were revoked for both existing and new muni bonds, the yields on existing tax-free munis could jump to match those of taxable munis. With about a 1.25-percentage-point spread between them, that could theoretically cause a 12.5% decline in the value of the tax-free bonds. It’s an unlikely outcome, but a potentially devastating one for investors who are not planning on holding until maturity.

A more likely possibility is that existing munis keep their tax-exempt status, while new issues would be taxable. This would create scarcity value for existing tax-free bonds, pushing their prices higher and their yields lower. However, remember that muni bonds are attractive only if their taxable-equivalent yields are equal to or higher than those of taxable bonds. In other words, if a 10-year Treasury yields 4.3%, the taxable equivalent of a 10-year muni bond would have to be 4.3% or higher. If it’s lower, there’d be little reason for an investor to own the muni bond.

(To calculate the taxable-equivalent yield, divide the muni bond yield by 1 minus the tax rate. So if you are in the 32% tax bracket and are earning 3% on a muni bond, you would divide 3 by 0.68, for a taxable-equivalent yield of 4.4%. In that case, the muni bond is a better investment than the Treasury.)

In this scenario, while existing tax-exempt bonds might see more demand, they would be unlikely to rise so high that their taxable-equivalent yields would drop meaningfully below taxable bond yields.

It’s also possible that only some sectors, like hospitals and higher education, could be targeted. If so, existing bonds in these sectors could become more valuable if they’re grandfathered in and retain their tax-exempt status.

Even so, the general consensus among fund managers seems to be that Congress is well aware of the value of tax exemption for funding local projects, making a full repeal unlikely.

Why would legislators want to raise borrowing costs for projects in their own districts?

All in all, there seems to be little reason for panic as of yet. A complete elimination of the muni tax exemption remains unlikely.

Remember, municipal bonds have weathered many tax policy discussions over the decades, and they’ve maintained their tax-exempt status through it all. Stephen Moore, an informal advisor to Trump, has suggested that even if changes come, they might include a “cap” on the exclusion for newly issued bonds rather than a broad repeal.

As I’ve always said, patience is key in bond investing. The higher yields we can lock in today might not be available for much longer, especially if this tax talk blows over. And if you’re holding bonds to maturity anyway, short-term market fluctuations aren’t your primary concern.

For now, if you own high-quality municipal bonds, stick with them. The benefits of munis – including their safety, liquidity, and tax advantages – still make them attractive for fixed income investors in higher tax brackets. If anything, this uncertainty could cause other investors to overreact, creating additional buying opportunities for those who stay the course.

RETIREMENT ROUNDUP

Should You Hire a Financial Advisor?

By Marc Lichtenfeld • Chief Income Strategist

You may be surprised to hear this, but early in my career, I used a financial advisor. I was working long hours, my kids were little, and I just didn’t have a lot of time to spend on my investments.

It was money well spent... until it wasn’t. That’s not because the advisor did anything wrong. It’s simply because, after a few years, I once again had the time to handle our investments myself, so it no longer made sense to pay the thousands per year in fees.

Many retirees and soon-to-be retirees struggle with the question of whether to hire a financial advisor.

Sixty-two percent of Americans age 50 and older manage their own money, which isn’t surprising. Financial advisors are not cheap. A fee-only advisor typically charges around 1% of managed assets annually. For a $500,000 portfolio, that’s $5,000. For a $2 million portfolio, it’s $20,000. That’s a lot of money out the door each year.

(Of course, the larger your portfolio, the more your advisor stands to make and the more incentivized they are to make you money.)

Some advisors charge a little more than 1%, some a little less. But don’t pay more than 1.25%. If an advisor is charging anything over that level, they’d better be providing some pretty specialized services.

Very few advisors are going to make you a ton of money, and if their pitch is that they will, don’t just walk away – run. A good advisor will understand your needs and design a portfolio accordingly.

If you believe that someone else will do a better job than you of reducing your risk while achieving reasonable returns, then it may be worth paying an advisor. But know that no one cares more about your money than you.

Ultimately, you should hire a financial advisor for one reason only: to help you sleep at night.

If you decide to use an advisor, here are a few things you should do.

1. Only use an advisor who has been recommended to you by someone you know and trust.

There’s no reason to give your money to a stranger. Find a friend or relative who is happy with their advisor. You need to be able to trust the person handling your money, and if they’re getting referrals from existing customers, chances are they’ll want to treat you well too.

2. If a new advisor tries to sell you an annuity or life insurance policy right off the bat, find someone else.

I’m not a fan of these products. They’re expensive and complicated. That doesn’t mean they’re wrong for everyone, but they carry big commissions, and if an advisor is pitching a product that will give them a big payday right after meeting you, they probably don’t have your best interests in mind.

3. Consider certified financial planners.

CFPs are fiduciaries, which means they must act in your best interest. Brokers and other advisors only have to recommend investments that are suitable for you − not necessarily best for you.

For example, let’s say you’re considering two similar mutual funds. Fund A has a 0.85% expense ratio, and Fund B has a 1.25% expense ratio and a 5% load (a type of upfront fee). A CFP would have to recommend Fund A because it’s in your best interest due to the lower fees, but an advisor could recommend Fund B and get a bigger commission. A good advisor would never do that to their clients, but they could do so without getting in trouble with regulators.

4. Look for an advisor who is experienced and well connected.

If you are in or nearing retirement, use an advisor who has been around for a while, has lots of clients in your age group, and understands the needs of retirees.

The 25-year-old kid who is early in his career may be earnest, but he doesn’t have the experience in navigating the various challenges that older clients face.

An advisor who has had a long career will also have a large network of other professionals. My mother’s advisor has set her up with her accountant, lawyers, and other services she needed. They all treat her well because the advisor sends a lot of business their way.

Which Option Is Best for You?

Many of our subscribers here at The Oxford Club don’t have an advisor, because they prefer to use the tools and recommendations we offer to manage their money and their risk. And that’s perfectly fine.

But there are also plenty who do use an advisor. Some of them have an advisor handle a portion of their wealth, while they take care of the rest of it themselves. Others work with an advisor but tell them to buy certain Oxford Club recommendations.

The Oxford Club has several financial advisors on our Pillar One Advisors list. We receive no compensation from them. They are simply advisors who we know and trust and who have received positive feedback from our Members.

What has your experience been like with financial advisors? Tell me some of your best and worst stories. Email me at mailbag@oxfordclub.com.

SNAPSHOT

MLPs Deserve a Place in Your Income Portfolio

By Anthony Summers • Director of Trading

High-quality income investments come in many forms. While it’s tempting to almost exclusively focus on traditional dividend stocks, master limited partnerships − like Marc’s recommendation for this month, Brookfield Infrastructure Partners (NYSE: BIP) − are an excellent alternative that is often overlooked.

MLPs operate with general partners, who manage operations, and limited partners, who provide capital and receive distributions (i.e., dividends).

They combine the tax benefits of a partnership with the liquidity of a publicly traded company, and they issue “units” that trade on exchanges just like stocks.

To qualify as an MLP, a company must generate at least 90% of its income from qualifying sources, such as activities related to natural resources. This is why MLPs are predominantly found in the energy sector, particularly in midstream operations like pipelines and storage.

In today’s ultra-competitive market for yield, MLPs stand out because of their unique tax structure. Unlike regular corporations that face double taxation (first at the corporate level and then again when shareholders pay taxes on dividends), MLPs are “pass-through” entities that avoid corporate-level taxation entirely.

What’s more, when you receive an MLP distribution, it’s not all immediately taxed as income. Instead, portions of these distributions are considered a “return of capital” that reduces your cost basis.

Rather than paying taxes every year on the distributions (as you would with normal stock dividends), you aren’t taxed until you eventually sell your MLP units.

Plus, when you finally sell, most of your profit is taxed at the lower long-term capital gains rate, not as ordinary income. This allows your investment to compound more efficiently over time.

This tax-advantaged structure essentially provides a tax-free loan from the government, allowing you to defer taxes for years or even decades.

It also means that holding MLPs in tax-advantaged accounts like IRAs or 401(k)s wastes their inherent tax-deferral benefits, since you’re already getting those benefits from the retirement account itself.

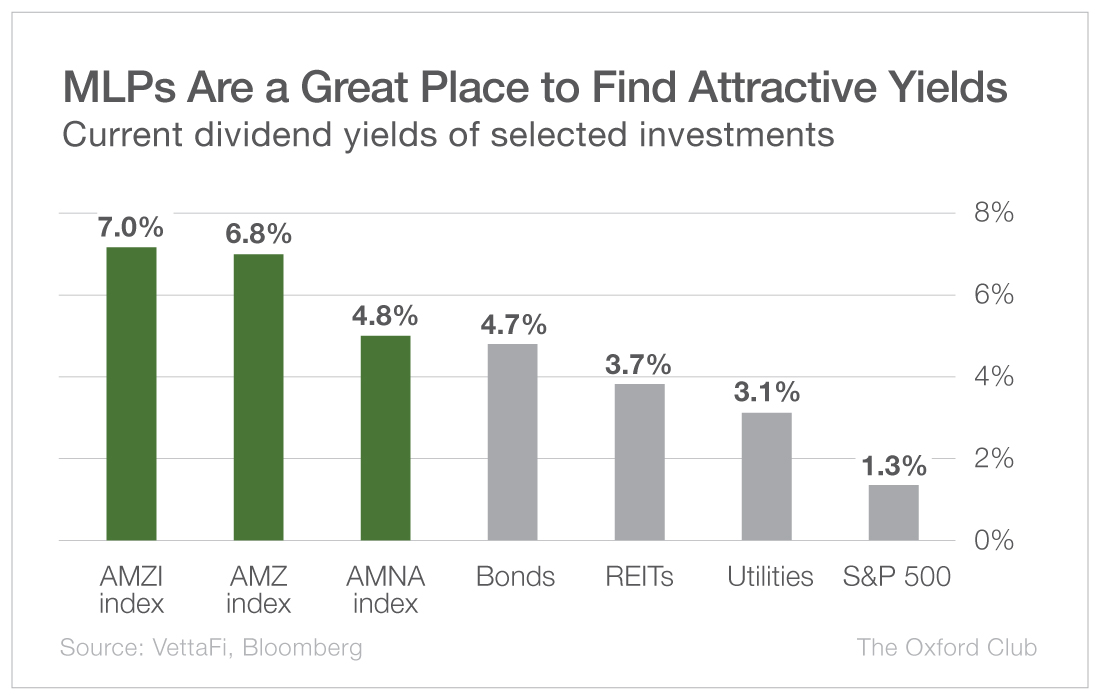

The Yields Are Hard to Ignore

While the tax advantages are compelling, the headline yields of MLPs are what catch most income investors’ attention. Many MLPs currently offer yields in the 6% to 8% range, far exceeding those of most dividend-paying stocks and fixed income alternatives.

The chart below shows three MLP indexes that have significantly higher yields than other yield-focused investments, such as high-yield bonds, real estate investment trusts, and utilities.

View larger image

View larger image

What’s particularly notable is that many MLPs have been growing their distributions, and very few have been cutting them. Over the past year, around 70% of the MLPs in the three indexes listed above increased their payouts, and not a single one reduced its payout. In fact, no MLP in the Alerian Midstream Energy Index (AMNA) has cut its regular distribution since July 2021.

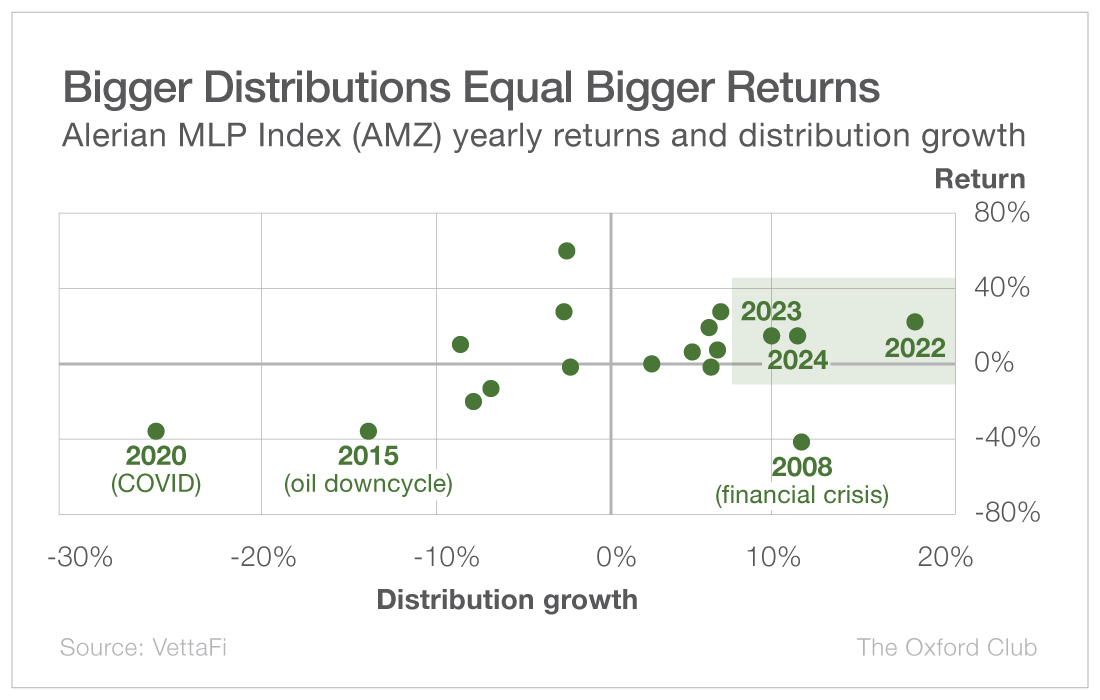

Performance Tends to Follow Distribution Growth

An important trend to note with MLPs is the relationship between their distributions and their returns. History tells us that when MLPs grow their distributions year over year, they often generate sizable returns.

View larger image

View larger image

Considering the strong double-digit distribution growth we’ve witnessed over the past three years, the outlook for MLP performance appears favorable. Many MLPs are generating substantial free cash flow, which supports continued distribution growth. Some, like Enterprise Products Partners (NYSE: EPD) and MPLX (NYSE: MPLX), have never cut their distributions – an impressive track record given the volatility we’ve seen in energy markets.

Now, while I’m enthusiastic about the opportunities in the MLP space, there are some risks involved. The most obvious one is that, since most MLPs are in the energy sector, extreme energy price volatility can impact their businesses.

Another is that, despite their clear tax advantages, MLPs can come with a few tax complications too. For one, MLPs issue K-1 forms rather than the 1099 forms you receive for regular stock dividends, which can complicate your tax preparation.

MLPs can also generate unrelated business taxable income, or UBTI, which sometimes forces owners of tax-exempt retirement accounts to file additional tax forms and potentially pay extra taxes.

Even so, if you’re looking to boost your income and take advantage of tax-deferred growth, high-quality MLPs deserve consideration. Their superior yields, tax advantages, and improved business models make them compelling alternatives to traditional dividend stocks.

Of course, not all MLPs are created equal, and selectivity is crucial in this space. Focus on MLPs with strong balance sheets, consistent distribution growth, and sustainable businesses. Your income portfolio will thank you.