Trump’s Report Card

Note From Managing Editor Katherine Koman: With the 2020 presidential election officially underway, our Oxford Insight writers will begin looking at the major candidates through the prism of how they might impact investors. We’ll examine their proposals and statements on economic policy, tax and trade matters, budget and fiscal policy, and of course anything to do with financial markets.

But first, Senior Macroeconomic Analyst Matt Benjamin is going to look at President Trump’s record on these issues. It will provide a baseline to evaluate the Democrats looking to unseat him in November.

From the Baltimore Clubhouse – As we begin to examine the presidential candidates and the impact they might have on our portfolios, we need to first look at President Trump’s report card.

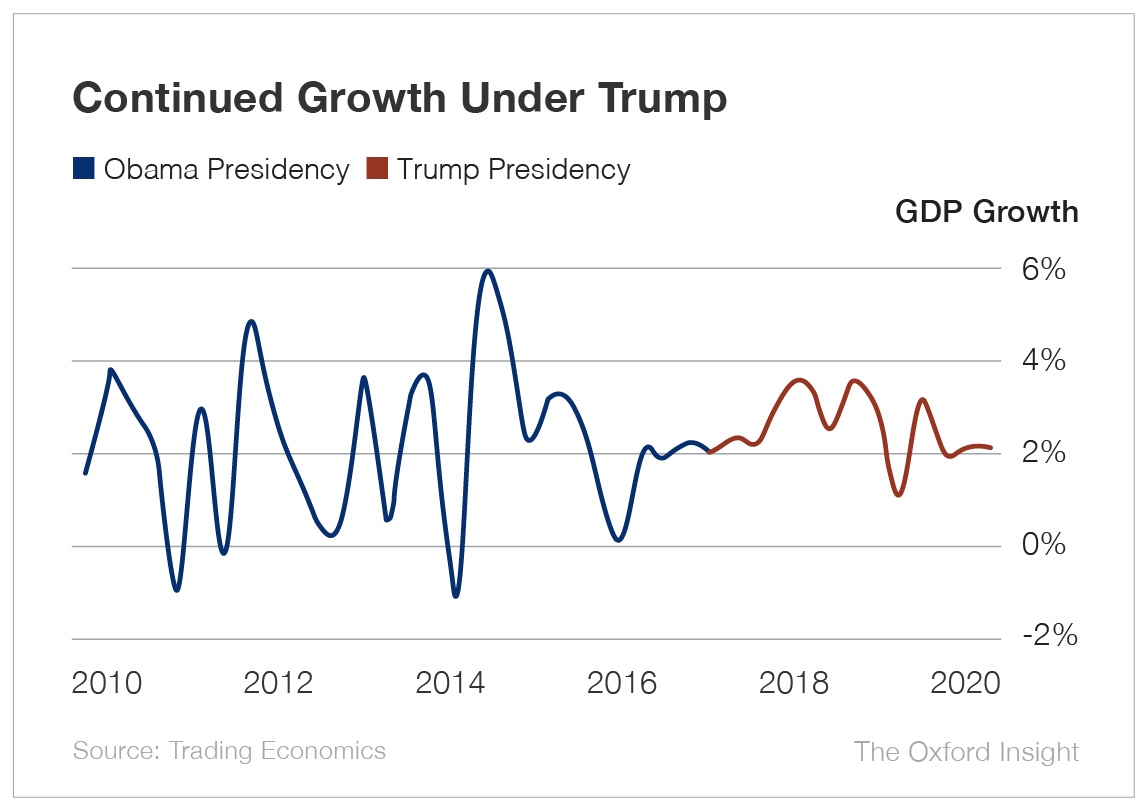

Economic growth and unemployment. Here, Trump’s record is solid.

True, gross domestic product (GDP) growth in recent quarters has settled to just above 2% (it was 2.3% for 2019), but that’s kind of the new speed limit for the U.S. economy, based on available labor and capital and the fact that we’re 10 years into an economic expansion. Over Trump’s three years in office, annual GDP growth has averaged more than 2.5%.

Early in his administration, Trump promised growth of as much as 6%, but no economist thought that was remotely possible. It was just Trump being Trump.

Under Trump, unemployment has fallen to 3.5%. The last time it was that low was a few months after Neil Armstrong and Buzz Aldrin stepped onto the moon. And though it’s difficult to know for sure, most economists think 3.5% is about as low as it can go. If you want a job, there is probably one available. That is an enviable position for any economy.

Of course, there’s a caveat here. Trump inherited a strong economy from President Obama. Yet Trump has helped it continue via tax cuts and other measures, and that’s not to be dismissed. Presidents can’t take all the credit for the economy under their watch, but they can certainly screw things up. Trump has not done that.

![]()

Trade. This one is tricky. Traditionally, presidents go about trade negotiations carefully and diplomatically. Not Trump. (He’s from the bare-knuckle world of New York City real estate, after all!)

Trump won the White House in 2016 partly by recognizing that a lot of Americans have not benefited from free trade. He promised to remedy that by renegotiating existing trade relationships. So far, he has replaced NAFTA with the United States-Mexico-Canada Agreement. But that new trade deal is surprisingly like the old one, and many economists expect it to change almost nothing.

With regard to China, Trump talked tough and got some concessions from the autocrats in Beijing, particularly on intellectual property concerns. China has also agreed to increase its purchases of U.S. agricultural goods. It’s a start, and perhaps China now realizes it can no longer take advantage of its biggest trading partner. We’ll see.

Trump now seems to be itching for another trade war, this time with Europe. Punitive tariffs on European goods could potentially tip Europe – already economically weak – into recession. It’s far from clear that Trump’s strategy will turn out well there.

![]()

Taxes. In 2017, Trump pushed through the Tax Cuts and Jobs Act, the biggest tax overhaul since 1986. He should be given credit for thinking big, and the legislation has certainly stimulated the economy. About 8 in 10 households got a tax cut, allowing them to spend more and continue the economic expansion.

A central plank of the tax act was the reduction of the corporate tax rate from 35% to 21%, with the hope that companies would decide to spend more on equipment, factories, technology and workers. They would do so, the reasoning went, because they could keep more of the eventual profits from those investments. And those investments would make American workers and businesses more productive, eventually raising the economy’s “speed limit” and allowing for faster economic growth.

So far, that increase in business investment has been small. But that’s not to say it won’t eventually happen. And the theory behind it seems right.

![]()

Budget. The major drawback to Trump’s tax cut, of course, is its enormous price tag. It is expected to add between $1 trillion and $2 trillion to the national debt over 10 years.

Ideally, when you cut taxes, you should make offsetting spending cuts elsewhere in the budget to avoid increasing deficits. Trump and Congress did not do that. The budget deficit was $984 billion last year. The Congressional Budget Office expects that to hit $1 trillion in fiscal 2020 and average $1.3 trillion from 2021 to 2030.

At some point – no one knows when – these ongoing deficits are going to inflict real damage on the U.S. economy by driving up borrowing costs, cutting needed investments and damaging the power of the dollar. Whatever happened to the tea party?

That said, if the change to corporate tax rates does eventually result in higher productivity, some of these deficits will have been worth it. The jury’s still out.

![]()

Stock market. Trump has undeniably been good for the stock market. Markets love tax cuts, especially on corporations. The massive tax cut they are enjoying should save U.S. companies some $1.35 trillion over 10 years. That allows them to return capital to shareholders and has made their shares more attractive to investors.

As Chief Investment Strategist Alexander Green has written, “Trump’s deregulatory policies and tax reform have boosted the U.S. economy, business investment and consumer confidence.” Those have all contributed to what is now the longest bull market in U.S. history. (Though Alex also points out that the stock market is far too big and complex for even a U.S. president to determine its direction.)

But Trump’s very attitude toward business and markets has been instrumental too. Investors and businesses perceive him to be on their side, and that builds confidence and supports growth.

“The market has performed well under Donald Trump,” Chief Income Strategist Marc Lichtenfeld told me this week. “That’s likely due to corporate tax cuts, a healthy economy and, perhaps most importantly, his jawboning the Fed into keeping interest rates low.”

![]()

All in all, Trump’s grades (as far as investors are concerned) are pretty good. A mixture of A’s, B’s and C’s. They resemble the report cards my sons bring home!

Next up: the Democrats.

Good investing,

Matt

P.S. No matter what happens at the polls later this year, it is sure to affect investors in some way. That’s why the theme of this year’s Investment U Conference is the election and how you can profit. Hope to see you there.