Are Buybacks the New Dividends?

From the Baltimore Clubhouse – Corporate America broke another record last year.

In 2018, stock buybacks exceeded $1 trillion – setting a new record for buyback announcements. Some analysts expect the record-breaking buyback activity to continue into 2019, possibly even surpassing last year’s record.

But not all are happy about this.

Recently, Sen. Bernie Sanders and Sen. Chuck Schumer published an op-ed piece in The New York Times proposing restrictions on corporate share buyback programs.

Their reasoning?

Too much of the cash saved from slashing the corporate tax rate has gone to buying back shares – delivering increased value to shareholders – and not to workers in the form of raised wages.

Given today’s political landscape, I suspect their proposal might gain some media attention. But here’s why you should be skeptical of such proposals.

Typically when politicians pit shareholders against workers, they assume the two are wholly separate. This is a false premise from the start.

Many shareholders are, in fact, everyday people who’ve invested in the stock market to accumulate long-term retirement savings.

When companies make decisions on behalf of shareholders, that’s you and me.

By attempting to limit how a company chooses to distribute returns to its shareholders – be it through reinvestment in operations, dividend payouts or share buybacks – the government is pretending to know how to best manage a company’s finances.

Of course, we know that’s just silly.

Such decisions require striking a delicate balance. But it’s one best understood by businesses, not government.

Let’s consider why a company buys back its stock at all.

By reducing the number of shares outstanding, the value of individual shares – now more scarce – increases.

Thus, companies buy back shares to increase shareholder value… shareholders who represent not only the rich but also the poor and middle class hoping to retire on the wealth accumulated with those stocks.

That’s where politicians don’t see the full picture.

These attempts to tie the hands of big business might score easy political points with a society increasingly antagonistic toward capitalism and free market principles…

But would such proposals actually help anyone?

That’s yet to be determined.

What has, however, been shown is that buyback activity helps boost shareholder returns and therefore bolsters the savings of those invested in those companies.

Let’s now turn to the numbers…

We’ll take a look at the S&P 500 Buyback Index, which tracks the performance of the top 100 large cap stocks based on buyback activity.

Let’s compare its performance with that of the overall S&P 500.

As you can see above, buyback stocks have delivered superior performance over the past two decades – gaining nearly three times more than S&P 500 stocks.

Investing in buyback stocks could be seen as a marriage between the benefits of both value investing and insider buying.

It relies on the ability of the company’s management to know its own intrinsic value and to invest when market prices fall beneath that value.

Unlike individual insider trading, however, share buybacks are done in order to deliver long-term value for the company’s investors.

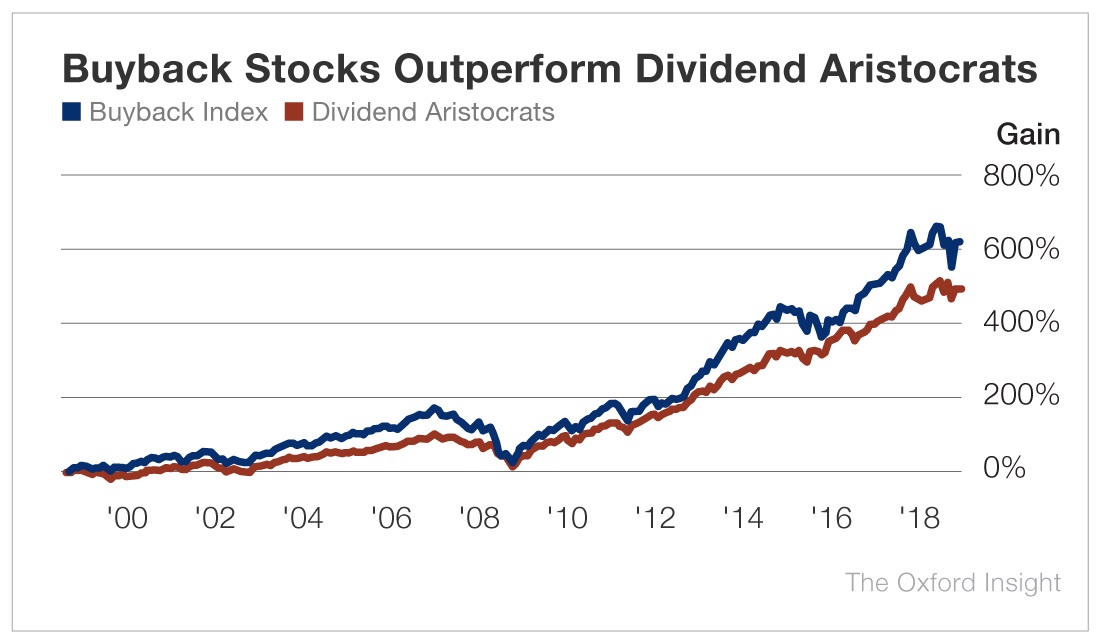

Another way to bolster investor returns in the absence of better uses of capital is to pay a dividend. However, even this powerful long-term strategy pales in comparison to the performance of buyback stocks.

Even stocks with the most consistent dividend growth and payment history – like Dividend Aristocrats – don’t quite deliver the same long-term returns as buyback stocks.

Keep in mind that when a company buys back its own stock, it’s a sign that management believes it’s either undervalued or at least fairly valued.

There has been a strong surge of buyback announcements because of the market sell-off in late 2018. Yet another bullish indicator to buy now-undervalued stocks.

Good investing,

Anthony