The Gone Fishin’ Portfolio Annual Review

Editor’s Note: Each January, the Club likes to pause and reflect on the lessons we learned during the previous year.

Naturally, we examine the performance of all our portfolios. (As you heard on Sunday, David Fessler’s Advanced Energy Strategist had the best-performing stock portfolio.)

But we also dig into our investment philosophy.

As you know, the Club’s first Pillar of Wealth recommends a diversification of investing strategies – not just of asset classes.

That said, a Core Portfolio – one that contains a traditional asset allocation of funds – should be your foundation.

Alex Green’s Gone Fishin’ Portfolio is the perfect example.

So when our Research Team realized that the Gone Fishin’ Portfolio had underperformed the S&P 500 in 2017, we asked Alex to revisit the value of an asset allocation model. What he has to say may surprise you…

– Rachel Gearhart, Senior Managing Editor

2017 was yet another good year for our Gone Fishin’ Portfolio.

Those who followed the strategy – investing in all 10 Vanguard mutual funds (or ETFs) according to the recommended asset allocation – earned a 16.3% total return, net of expenses.

In my past few annual reviews, I suggested it was just a matter of time before the red-hot U.S. stock market finally lagged the performance of overseas markets.

Those forecasts proved premature – until last year.

In 2017, the Vanguard European Stock Index Fund (VEURX) returned 26.8%. The Vanguard Pacific Stock Index Fund (VPACX) returned 28.4%. And the Vanguard Emerging Markets Stock Index Fund (VEIEX) returned 31.2%.

Those three funds make up a total of 30% of our asset allocation.

The portfolio got a further boost from its 15% weighting in the Vanguard Small-Cap Index Fund (NAESX). That fund returned 16.1% last year.

However, we also have 10% each in the Vanguard Short-Term Investment-Grade Fund (VFSTX), the Vanguard High-Yield Corporate Fund (VWEHX) and the Vanguard Inflation-Protected Securities Fund (VIPSX). These three funds posted modest single-digit returns last year, as you would expect in the current low interest rate environment.

Meanwhile, the S&P 500 had another banner year. Including dividends, it returned 21.6% in 2017.

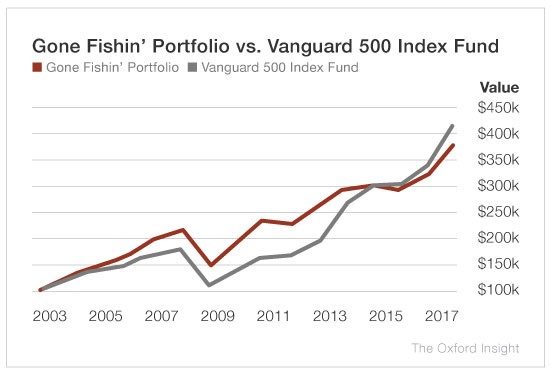

As you can see from the chart below, the S&P 500 has now outperformed the Gone Fishin’ Portfolio since its inception in 2003.

In some ways this is unremarkable.

This is a conservative, long-term asset allocation strategy. With 30% of the portfolio in bonds, holders incur far less risk – and fewer sleepless nights – than those fully invested in equities. Yet net of all costs, an original investment of $100,000 in the Gone Fishin’ Portfolio has nearly quintupled since 2003.

Still, investors are a performance-driven lot, and no doubt some have begun to question the value of asset allocation.

Questioning it is fine. Abandoning it, however, would be a mistake.

Here’s why…

Behavioral psychologists tell us that investors often fall prey to “the recency bias.” This is the tendency to extrapolate recent events into the future indefinitely.

When technology and internet stocks were hot in the late ’90s, for instance, investors talked of a “new era” of limitless growth in the sector, despite the near-complete absence of earnings or – in many cases – even sales. Things ended badly when – over the next 2 1/2 years – the leading index of internet stocks, from peak to trough, declined 96%.

A similar phenomenon arose a decade ago with the housing bubble. After watching residential real estate rise at roughly the rate of inflation for half a century, low interest rates, easy credit and skyrocketing home prices suddenly convinced investors that “they’re not making any more land” and “real estate always goes up.”

That euphoria quickly dissipated in the ensuing financial crisis. And as the stock market collapsed, investors also convinced themselves that a weak economy and stagnant share prices were “the new normal.”

Out of that mistaken conviction arose one of the greatest bull markets in history. From January 2009 through the end of last year, the S&P 500 – with dividends reinvested – returned 268%.

With U.S. stocks the best-performing asset class of the last decade, some now argue against asset allocation, insisting that an investment in the S&P 500 is all the diversification anyone needs.

Check that recency bias at the door.

The S&P 500 may well continue its outperformance in the months and years ahead. Indeed, we are in an unusual period of low inflation, rock-bottom interest rates, cheap energy, synchronized global growth and rising corporate profits.

However, this good news is well factored into stocks, making them pricier than average at 23 times trailing earnings.

If we continue to get great economic news, of course, share prices could head higher still.

Yet some investors have been lulled into a sense of complacency by the extraordinary outperformance of the U.S. market, especially since it’s been accompanied by an entirely ahistorical lack of volatility.

Don’t be one of them. Every bull market is followed by a bear market. When the next one arrives, your bond allocation will soften the blow. And rebalancing will allow you to take advantage of lower stock prices.

This is the real value of fixed income securities in a long-term portfolio. They counterbalance the risk – the occasional neck-snapping volatility – of equities.

With this in mind, let’s review the real-world philosophy that underpins our Gone Fishin’ strategy:

- It is not possible to consistently predict the economy or the stock market. (That is why economic forecasting and market timing are no part of this strategy.)

- Asset allocation is your single most important investment decision, responsible for 90% of your portfolio’s long-term return. (The balance is due to security selection, expenses and taxes.)

- Over periods of a decade or more, more than 95% of all active fund managers fail to match the returns of their benchmarks. That is why we use index funds.

- All asset classes have periods of outperformance and underperformance. The smart investor takes advantage of this by owning a wide variety of asset classes and rebalancing annually.

- All else being equal, the lower your costs, the higher your net returns. You should use the lowest-cost vehicles available: ETFs and Vanguard mutual funds.

- You can further enhance your net returns by tax-managing your portfolio. Hold your tax-inefficient assets – such as interest-paying bonds and dividend-paying real estate investment trusts – in your tax-deferred retirement accounts. Hold your tax-efficient assets – like equity index funds – in your nonretirement accounts. Doing this allows you to legally stiff-arm the IRS.

The Gone Fishin’ strategy requires only that you set up the portfolio using Vanguard mutual funds or ETFs and take 20 minutes once a year to rebalance it.

(The rest of the time you are encouraged to “go fishin’.”)

Paring back your outperformers and adding to your laggards this way doesn’t just reduce risk and boost returns. It literally forces investors to do what they’re supposed to do: sell high and buy low.

The Gone Fishin’ Portfolio is our most conservative strategy, allowing you to manage your serious money in a simple but sophisticated way.

With modest risk, low volatility and a high probability of long-term success, it provides an excellent foundation for your investment program.

Good investing,

Alex

NOTE: If you’re not already an Oxford Communiqué subscriber and are interested in learning more about Alex’s successful, time-tested approach to investing and taking advantage of the stocks in his four Communiqué portfolios, including the Gone Fishin’ Portfolio, click here.